Economy

Conditions are improving for business investment.

Business investment as measured in gross domestic product has three major components: equipment, structures, and intellectual property products, or IPP. Among the three, equipment accounts for the largest share, totaling about 47 percent of business investment in the third quarter of 2016. IPP accounted for about 33 percent, while structures’ share was 20 percent.

The plunge in crude-oil prices that began in mid-2014 hurt investment in both structures and equipment, while IPP was largely unaffected (Chart 2). For the structures component, energy investment spending fell from a high of $127 billion in the fourth quarter of 2014 to just $41 billion in the third quarter of 2016, about a 67 percent drop. While investment in structures excluding energy-related spending increased at an average pace of about 7.8 percent, that growth dropped to less than 1 percent when energy structures were included.

Mining and oil-field equipment spending fell to just $9.8 billion in the third quarter of 2016 from $30 billion in the second quarter of 2014, also about a 67 percent drop. However, unlike the structures component, equipment spending minus energy-related equipment still suffered a significant slowdown in recent quarters, dropping an average of 0.4 percent since the third quarter of 2014 (compared with an average gain of 10.6 percent from the fourth quarter of 2013 through the third quarter of 2014). All equipment, on the other hand, has declined at a 1.3 percent average rate since third quarter 2014, compared with an average 10.4 percent rise in the year before.

Among the other major components, tech spending fell over the first two quarters of 2016, transportation equipment dropped over each of the past four quarters, and the catchall “other” category excluding energy is down from its peak in mid-2014, led by drops in agricultural and construction equipment.

The combination of higher crude-oil prices boosting energy-related investment and a somewhat stronger economy overall is likely to provide a foundation for continued improvements in business investment in the coming quarters.

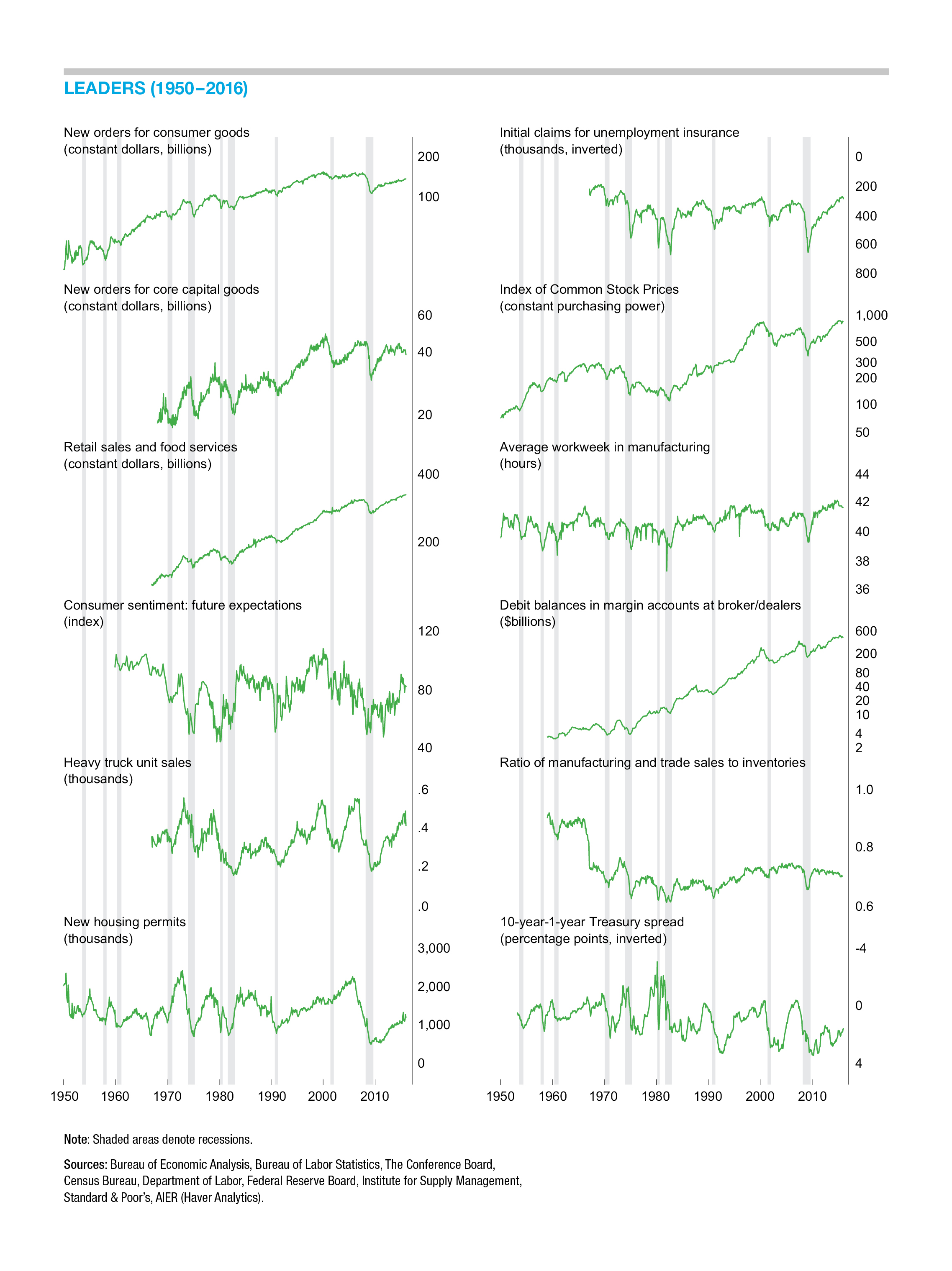

Economic Outlook

Our Business-Cycle Conditions Leaders index improved again in the latest month, rising to 67 in November from 58 in October (Chart 3). November marks the highest level since September 2015 and the third month in a row above the neutral 50 level. As we have been saying, we do not believe there is enough evidence to suggest that the economy is on anything but a slow growth path. However, a reading of 67, the highest since September, provides solid evidence that the risk of recession in the months ahead has diminished.

The improvement for November resulted from two indicators turning up, from negative to neutral. The consumer sentiment indicator in our Leaders, the University of Michigan Index of Consumer Expectations, rose to neutral after several months of a negative trend. As the university’s survey says, “The upsurge in favorable economic prospects is not surprising given (President-elect Donald) Trump’s populist policy views, and it was perhaps exaggerated by what most considered a surprising victory as well as by a widespread sense of relief that the election had finally ended.”

Real new orders for core capital goods was the other Leader that turned up to neutral from negative. The combination of higher energy prices and better overall economic activity may lead to further improvements in this indicator.

Among our other indexes, the Coinciders were unchanged at 92 in November, while the Laggers rebounded to 75 from 67 in October.

Click for interactive Indicators at a Glance (on mobile device turn to landscape)

Next/Previous Section:

1. Overview

2. Economy

3. Policy

4. Investing