Yang’s Concerns Over Automation Are Overwrought

Every story needs a villain, and the most popular villain recently in economic policy circles is automation.

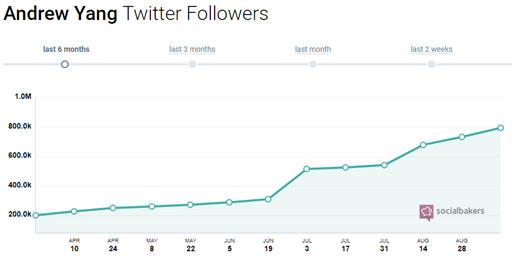

Andrew Yang, by no means a flawless presidential candidate, seems to be the only candidate directly addressing this issue, and his growing presence on Twitter shows how strongly his message is resonating.

He is the only candidate, however, running for president discussing what potentially will be the most important economic topic for the next decade; automation and its economic effects.

He is the only candidate, however, running for president discussing what potentially will be the most important economic topic for the next decade; automation and its economic effects.

The market is obviously craving an objective and level-headed analysis and debate around automation, especially given its potential economic impact.

Survey after survey highlights the percentage of jobs in certain professions set to be automated in the near future, with middle/knowledge class jobs like accounting and law in the crosshairs.

Economic inequality is a technology-driven issue, with some claiming that technology is only benefitting a small subset of the workforce and serves as an effective means to inflame sentiment.

This fear, of economic insecurity and inequality, drives many of the vitriolic debates and feelings dominating the public discourse around immigration, the minimum wage, and the trade wars that continue to dominate policy conversations. Automation, with the uncertainty and anxiety that accompanies this conversation, lies at the core of many seemingly unrelated threads.

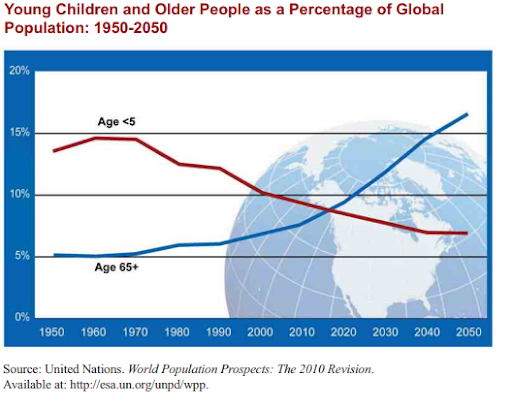

Demographics alone demonstrate the fact that automation needs to be embraced. According to the Census Bureau, the number of adults over 65 will outnumber people under 18 by 2035 in the U.S. Looking across the Atlantic, the E.U already has a fifth of its population over 65, and China is set to have 20% of its population above 65 by 2037.

How will economies continue to grow and prosper if the number of people available to work continues to drop worldwide? Attempting to forestall technological adoption and automation is akin to swimming upstream; exhausting and not productive.

Technology has proven itself a net job creator and an economic positive; according to McKinsey, personal computers along have created over 15 million jobs in the U.S. since 1980.

The answer to future job creation and growth also requires leveraging technology and automation. The WEF projects 133 million new jobs created via automation in the near term, but the evidence already exists in the products used voluntarily by millions of organizations and billions of people.

The list of the most valuable companies, and some of the largest employers in the world, shows how technology and automation creates wealth, empowers entrepreneurship, and creates economic growth. Microsoft, Apple, Amazon, Alphabet, Facebook, Alibaba, and Tencent top the rankings of the most valuable companies in the world, directly and indirectly employ tens of millions, and create trillions in economic value.

These organizations utilize technology and automation to deliver better products, improve the customer experience, and create new job categories.

Throwing money at the problem will not soothe the fears of automation, nor address the inequity created in an economy where access to continuous education, learning, and upskilling is required to succeed and grow.

No single answer, policy position, or individual, including Andrew Yang, has a monopoly on ideas or tactics to assist organizations and individuals contend with the changes that automation will bring to the economy, and believing otherwise only amplifies the already fierce debates on the subject.

Proactive and objective analysis on the subject, and realizing that automation is not the enemy is a much-needed change from the acidic commentary that dominates much of the public commentary on the subject.

Automation is not the enemy, it’s the key to future economic growth. The sooner economic and public policy experts realize that, the sooner productive and growth-oriented solutions can emerge.

Sean Stein Smith

Sean Stein Smith was a Visiting Research Fellow at the American Institute for Economic Research, focusing on blockchain, cryptoassets, and the economic impact of these technologies. He is an Assistant Professor at the City University of New York (Lehman College), serves on the Advisory Board of Wall Street Blockchain Alliance, where he also chairs the Accounting Working Group, and chairs the Emerging Technology Interest Group of the New Jersey Society of CPAs. His research has been quoted in dozens of scholarly and practitioner publications, and he is a regular speaker at accounting and technology conferences. Follow him on Twitter.