Why Uber’s Business Model May Not Be Viable

The rise of ride-hailing firms Uber and Lyft, flagships of the so-called sharing economy, has been nothing short of astounding. In less than five years, Uber has comfortably overtaken traditional taxis in market share for most major urban markets, with Lyft not far behind. At the end of March came Lyft’s long-awaited IPO valuing the company at $26.5 billion. Uber is hoping to go public next month with a valuation above $100 billion.

But neither company has made a profit. Lyft lost over $900 million in 2018, the deepest in the red any startup has ever been for the 12 months before its IPO. Uber will likely break that record next month: it lost over $3 billion in the past year.

Nobody doubts the sharing-economy model’s capacity for disruption. But is it a viable long-term business model for a large corporation? Investors obviously think so, but a close look reveals that the companies have precious little room to maneuver as they try to find their way to profitability.

Estimated Profit

To become profitable, the companies must either raise revenues, lower costs, or enter a whole new line of business.

We can think more carefully about potential lines of sight to profitability by looking at a highly stylized profit function. The following doesn’t capture every dollar that goes in or out the door of Uber or Lyft, but seeks to nail down the basics:

(Quantity of rides)*(Price – Driver’s share) – Fixed costs

A ride-hailing firm has the following options to increase its profits:

- Increase the number of rides without increasing costs

- Increase the price of each ride without losing market share

- Decrease the amount drivers get paid

- Reduce costs while maintaining market share

- Enter a new line of business

Continued Growth

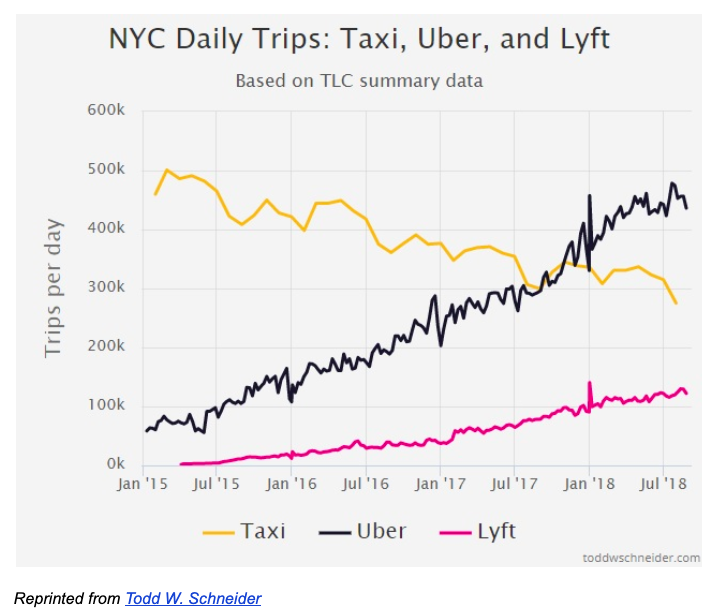

How much room do the ride-hailing leaders have to grow? The answer is less than you might think. The chart below shows the companies’ astonishing ascent to market dominance in New York City, but leaves one wondering how long the companies can maintain such growth.

Uber and Lyft combined for a total of about 600,000 rides in July 2018, with taxis at 300,000. Interestingly, taxis are down from their peak in the period of about 500,000 in January 2015, before either firm had appreciable market share. This means Uber and Lyft have achieved less than half of their growth in New York City by taking rides from taxis. The majority came from consumers who otherwise would have driven themselves, walked, rented a car, taken public transit, or not taken the trip at all.

The trouble with both taxis and other transportation options is that they are limited sources of growth. If the companies drove traditional taxis out of business in New York and took the rides in about the 75/25 ratio of their current sizes relative to each other, they would both grow by about 50 percent. This would replicate growth Uber and Lyft achieved in the 18 months starting in January 2017 — not exactly a limitless well.

Other transit options also supply fundamentally limited growth. Many walking (short distance) or driving (long distance) trips would not be economical for Uber or Lyft to provide. And if the companies stole more than a little market share from NYC public transit, excessive congestion would lead to nobody on the city’s roads finding any trip economical.

Rather than an outlier, New York looks similar to other major markets worldwide including London. Smaller markets are also limited in the growth they provide, and below a certain density just aren’t profitable (they haven’t even bothered with AIER’s hometown, Great Barrington, Mass.). And Uber’s current play after giving up ground to international firms in developing markets is the even lower-margin Uber Lite.

Finally, Uber or Lyft could gain market share from each other. We’ll talk about the prospects for monopolization below.

Unnatural Monopoly

Uber or Lyft can become profitable by increasing their profit margins, either by increasing prices charged to consumers or reducing the unit cost of a ride by paying drivers less. We typically think of firms as maximizing profits given the competitive landscape, meaning the path to higher margins is through greater market power.

Both companies have indicated their intention to become a “natural monopoly” in the industry, but the idea seems more like investor hype than an actual business plan. As Lyft has already shown, the rapid rise of a second player in the industry would be an extremely credible source of downward pressure on prices. And at least on a smaller scale, this is not a difficult industry to enter: one needs an app and a set of rules.

Uber and Lyft could also attain higher margins by paying drivers less — letting them keep less of each fare. But given the relentless charge against especially Uber that drivers are already not making enough, this would likely be the recipe for a public relations disaster.

End the War of Attrition

Uber and Lyft spend billions of dollars each year on essentials such as marketing and computing infrastructure. Lyft spent $1.3 billion in 2018 on “marketing and incentives for drivers and riders” alone. Will a successful ride-hailing firm have to make such outlays in the long term? Here the companies can find some room for optimism.

Lavish marketing expenditures and subsidies might be necessary right now for the companies to build trust in their brands and the ride-hailing model overall. But if the companies finish their conquest of traditional taxis and make a further dent in other transit options, they may establish enough trust and loyalty to cut this part of their budget.

The companies’ current war of marketing attrition might also be tied to their need for investor funding. Prior to going public, Uber and Lyft needed to show venture capital investors the highest possible revenue stream, meaning expensive marketing campaigns, discounts for consumers, and incentives for drivers. Once public, the companies will not need to return to the venture capital well, and can therefore settle in for longer-term growth. It’s a promising idea, though venture capital investors are on average more sophisticated than public ones and would likely see through such a strategy.

The Big Pivot?

Many have theorized that the real money in Uber and Lyft will come in the future with autonomous vehicles. But this is an extremely risky and long-term proposition. A fleet of driverless cars in every city will require not just the maturation of technology, but changes in society. And given the current trimming of profit margins to establish trust and market share, real profitability would likely take a great deal of time.

One can make a compelling case for the long-term profitability of the model as it’s currently deployed, but that case is far from certain. The companies can continue to take rides away from taxis and other transit options, but their already-explosive growth means there is a limit on this source of added profitability. Monopolizing the market to charge higher prices is less plausible, as is paying drivers less. Perhaps most promising is reducing other costs, though whether this alone is enough to reach profitability is far from certain.

The sharing economy, fueled by the internet’s capacity to match small buyers and sellers, looks like a revolutionary business model. But for this model to be sustained, there must be a reliable source of long-term profits. Ride-hailing is perhaps the application of the sharing economy that is currently most developed, so its success or failure will teach us a great deal about the model’s viability in the global business landscape.

Max Gulker

Max Gulker is a former Senior Research Fellow at the American Institute for Economic Research. He is currently a Senior Fellow with the Reason Foundation. At AIER his research focused on two main areas: policy and technology. On the policy side, Gulker looked at how issues like poverty and access to education can be addressed with voluntary, decentralized approaches that don’t interfere with free markets. On technology, Gulker was interested in emerging fields like blockchain and cryptocurrencies, competitive issues raised by tech giants such as Facebook and Google, and the sharing economy.

Gulker frequently appears at conferences, on podcasts, and on television. Gulker holds a PhD in economics from Stanford University and a BA in economics from the University of Michigan. Prior to AIER, Max spent time in the private sector, consulting with large technology and financial firms on antitrust and other litigation. Follow @maxg_econ.