Why the Argentine Peso Is Plummeting

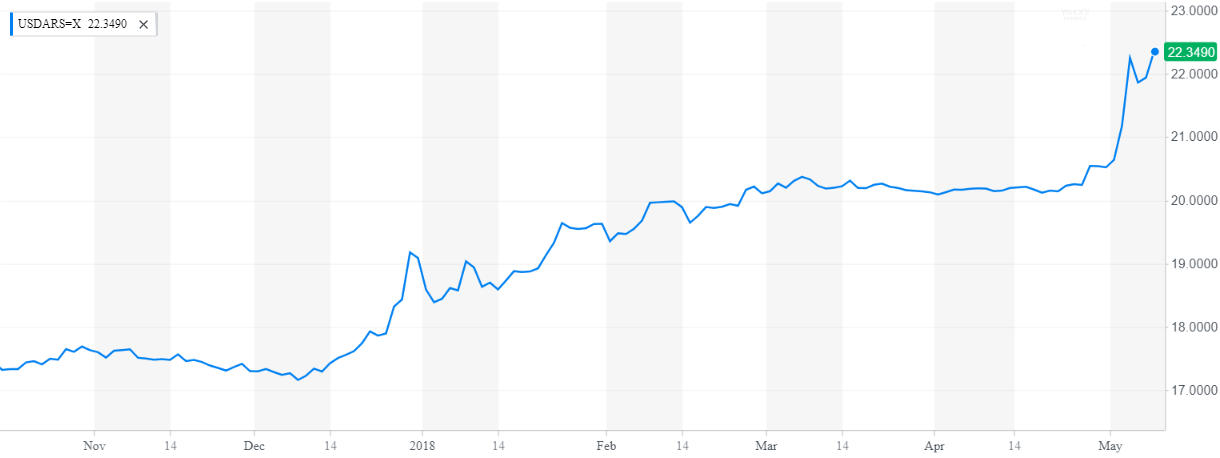

Days ago, Argentine President Mauricio Macri asked the International Monetary Fund for help. His call came after the Argentine peso tumbled. The peso fell by 10 percent in a matter of weeks and more than 25 percent over the past 12 months. (The peso-to-dollar rate went from 16 to approximately 23).

What caused Argentina’s currency crisis?

The Central Bank of the Argentine Republic (BCRA) did precisely what the textbooks on monetary economics explicitly tell you to do. The BCRA resorted to two main measures:

- raise interest rates;

- sell foreign-exchange reserves to “defend” the exchange rate.

In the process, the BCRA raised the benchmark interest rate from 30.25 percent all the way up to 40 percent in a matter of days. Moreover, it lost more than 10 percent of its foreign-exchange reserves in less than a week. The central bank intervened, but in vain: the free fall of the peso continued.

Why did the BCRA’s intervention fail?

To understand the perilous situation of the peso, we must go back to the previous Kirchner administration. Former President Cristina Kirchner basically used the central bank as an ATM. Her administration robbed the central bank of its foreign-exchange reserves. They exchanged reserves for worthless, non-transferable letters of credit (letras intransferibles) and, in effect, told the central bank: “Give us your dollars and in return we will give you these worthless and non-sellable IOUs.”

These worthless government IOUs already amount to more than 30 percent of the BCRA’s total balance sheet.

There is another asset that deserves scrutiny: transitory advances (adelantos transitorios). This account—already over 15 percent of the total BCRA balance sheet—was used by the Kirchner administration to finance public spending. Instead of issuing formal government debt, they issued 12-month IOUs. In practice, far from being mere advances, these were simply worthless government IOUs and toxic assets for the BCRA. Every 12 months, previous advances rolled over, and the total amount of “advances” just kept rising.

In sum, we have approximately 45 percent of toxic assets on the BCRA balance sheet, which are worth exactly the same as Kirchner’s election promises: zero.

Argentina’s current president, Mauricio Macri, has done little to solve this issue. First, Argentina still runs a large public deficit. Second, the Macri administration continues to finance this deficit partly with the same mechanisms as Kirchner did. The chickens, however, have come home to roost, and this predatory policy is coming to an end.

Why Are Central-Bank Assets Important?

Let’s do a brief thought experiment. What would happen if we were to completely liquidate a central bank? We would sell off its assets and pay all outstanding liabilities. Now, in the case of Argentina, the problem is that we have a bunch of assets that cannot be sold: neither the transitory advances nor the untransferable letters of credit can be sold in the open market. It is no secret that they are effectively worth zero.

The result is disastrous:

- We cannot pay off all our liabilities; we do not have enough assets (of value) to face a currency crisis. In fact, when we start selling foreign-exchange reserves, the market knows very well that we will never be able to defend our currency, since we do not have enough assets (reserves) to do so.

- We cannot raise interest rates without incurring losses. After all, the BCRA can only raise interest rates on its liabilities. Given the fact that a large part of its assets are toxic (and earn zero interest), raising interest rates leads to greater losses. And how are these losses paid for? By increasing either the transitory advances or the non-transferable letters. The central bank gets stuck in a negative downward spiral; it cannot raise rates without weakening its balance sheet. This shows that central banks are effectively interest-rate takers, instead of interest-rate makers: they depend much more on the market than they usually admit.

This is why the BCRA’s intervention was in vain. Central banks are sometimes capable of defending exchange rates and sometimes not. The “sometimes not” cases are due to the quality of the central bank’s assets. The BCRA lacks a strong balance sheet and a portfolio of healthy assets. The BCRA’s toxic assets ended up eating away the peso-denominated savings of the Argentine population.

Macri Can Solve This Currency Crisis

If President Macri wants to put an end to the currency crisis, he must fill the gaping hole on the Argentine central bank’s balance sheet and eliminate the public deficit. One way would be to simply replace the transitory advances and non-transferable letters with short-term sovereign bonds or US Treasuries. If the IMF’s assistance is needed to do so, so be it.

Unfortunately, Argentine savers will likely have to sit out the depreciation of the peso. Surely, after a significant devaluation of the peso, we can start over. But that is after a large part of the Argentine population have been robbed of their savings.

It could very well be that Argentina is the first domino to fall in an over-indebted world and an excess of toxic assets on the books of many central banks. The recent Argentine tragedy is a warning for other central banks, including the Federal Reserve.

Lessons for the Fed

First, we have to consider that the Fed does not own non-transferable, shady government IOUs that pay 0 percent interest, but highly demanded US Treasuries. This is the good news.

The bad news is the Fed’s mortgage-backed securities portfolio, which makes up roughly half of its balance sheet. For the moment, the US housing market appears strong and even bubbly. But in a worst-case scenario, the prices of these securities would suffer dearly during a downturn.

Moreover, the maturities of the Fed’s assets are long—extremely long. This means that if interest rates rise, the Fed’s assets will suffer price drops. (Higher interest rates imply lower bond prices.) A reverse “Operation Twist” (swapping long-dated US Treasuries for short-dated US Treasuries) is therefore not an option, but a necessity.

Otherwise, the Fed might suffer the dire consequences of an impaired balance sheet in the future, and as the case of Argentina proves, currency crises are no fun.

Olav Dirkmaat

Olav Dirkmaat is a Professor of Economics at Universidad Francisco Marroquín and Director of the university’s public choice center: the Center for Analysis of Public Decisions (CADEP). His research focus is on applied public choice, particularly questions of public finance (taxes, public debt, fiscal limits) as well as governance decentralization.