Why Debt-Driven Booms Are Unsustainable

Modern central banking claims to make the money supply more elastic to stabilize the economy. The rationale says that left to itself, the market economy is unstable. Yet the evidence suggests the opposite: that modern central banking is the main culprit for boom and bust.

Boom

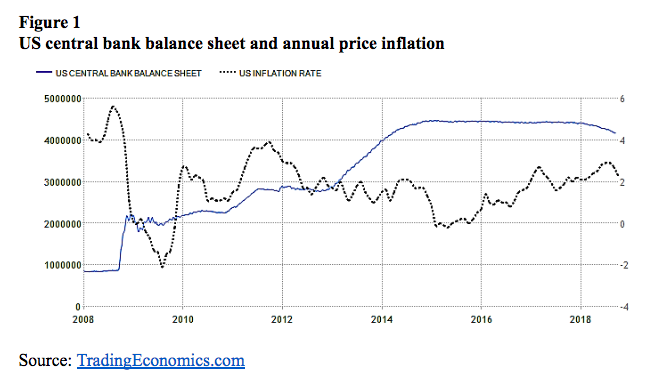

In 1914, the United States installed a central bank. The European countries abandoned the gold standard shortly thereafter. Since then, the world economy has experienced phases of hyperinflation, depression, and stagflation. There have also been times, as in the 1920s and the 1960s, when the price inflation was relatively mild even while the economy was booming. These periods, however, typically have ended in a bust. Over the past 10 years, the major economies have likewise experienced a phase of low, stable inflation. Price inflation has not materialized despite a massive monetary expansion. While the balance sheet of the American central bank increased from under $1 trillion to over $4 trillion, the price inflation rate remained relatively constant at around 2 percent (figure 1).

Whether a monetary expansion leads to inflation depends on the relationship between nominal demand and the economy’s productive capacity. When demand expands faster than production, the monetary expansion leads to price inflation. Without sufficient technological progress and when there are no other factors that lead to higher production possibilities, a monetary expansion becomes inflationary. This was the case with the run-up to the stagflation of the 1970s. In periods of clustered technological progress, as in the 1920s, for example, price inflation need not rise despite the monetary expansion. The debt-driven boom of the 1920s, as the prelude to America’s Great Depression, did not come with higher consumer prices.

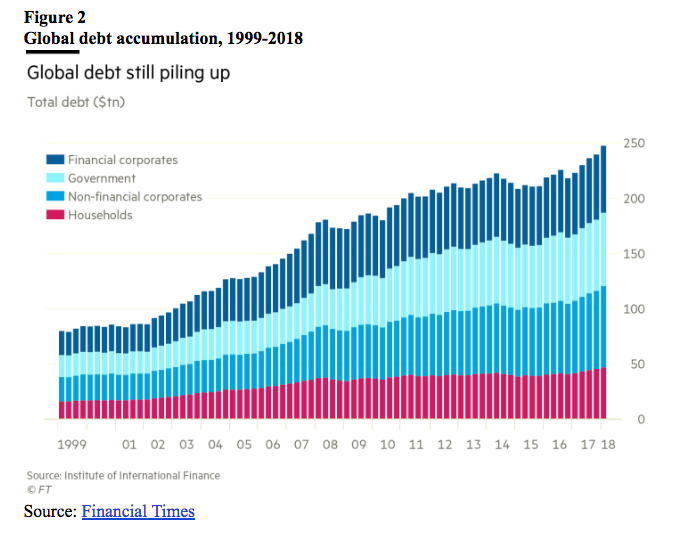

In the 1920s, the monetary authorities misinterpreted price-level stability as an indication that their monetary policy was not excessively expansionary. This also seems to be currently the case. When the central bank targets a certain rate of inflation, it inadvertently creates too much money when the economy’s productive capacity increases and thus would require a falling price level. Thus the central bankers fabricate monetary overexpansion and interest rates that are below the free market equilibrium. This policy moves the economy to ever-higher levels of debt (figure 2).

A stable-inflation boom is hard to recognize in the theoretical and statistical framework used by modern central banks. Steeped in the framework of Keynesian economic theory and its derivatives, monetary authorities do not wake up until the cycle has gone beyond the boom phase and the economy has already moved into the bust. Central banks, the government, and the public in general experience a period of deception as high economic growth, low unemployment, and stable, moderate inflation appear at the surface. This goes on as long as the productivity advances continue at a fast enough pace to offset the monetary expansion and no adverse supply-side shocks occur. By not letting deflation occur as the natural consequence of productivity gains and other cost reductions, central banks transform an economic expansion that began on the supply side into a debt-driven boom on the demand side. Each time the central bank authorities fear deflation, they augment the money supply, thereby pushing the economy to higher debt levels.

Over the past decades, the integration of many new suppliers into the world economy has led to a strong expansion of the productive capacity on a global scale. While the inflation rate has fallen from close to 14 percent in 1980 to below 2 percent since 2016, the rate has not yet turned negative. Deflation should have happened as the consequence of more production. That this did not happen indicates that the money supply and the debt expansion it implies have turned the natural economic expansion into an artificial boom.

Bust

Debt expansion implies the build-up of an overhang of liquidity. In the boom phase, most of the excessive liquidity tends to be absorbed by the asset markets. It is no surprise that the end of the boom phase typically coincides with overvalued asset prices as the prelude to a stock market crash.

When the contraction arrives, the expansionary monetary instruments of central banking become blunt. Central banks may go on and expand the money supply. Yet this excess liquidity will build up as higher reserves in the banking sector and thus paralyze active monetary policy. In the face of a bleaker economic outlook, economic actors will try to reduce their debt exposure. Unlike what happens in the boom phase, when it was easy for the central bankers to push the economy to expand, the stimulus policy no longer works in the bust. Additional liquidity does not turn into new debt.

It takes a while until the statisticians can register that the contraction of liquidity affects the real side of the economy. As now the economy’s productive capacity shrinks, the price level tends to stabilize. This phenomenon adds a further treacherous factor to the monetary policy makers’ analysis. Things get even worse when fiscal policy is called to substitute for the failed monetary policy. As rising public expenditures meet a shrinking supply, the structure of production distorts further.

The economy veers between a deflationary depression and stagflation. At the end of the debt-driven boom of the 1920s, a deflationary depression followed in the 1930s, while in the 1970s, stagflation occurred. The difference came because of government spending. In the 1970s, fiscal policy was highly expansive. Yet this policy did not cure the slump. Unemployment remained high, and real economic growth did not pick up. What grew was the public debt.

When the bust sets in, the velocity of money circulation contracts. It was this phenomenon of a collapsing money supply that attracted the attention of the monetarists. The basic error of monetary policy, however, is not the inactivity of central banks in the slump, as the monetarists claim, but the active stance at the inception of the boom when central banks decrease interest rates and feel vindicated by an apparently stable price level.

Conclusion

Productivity gains and the expansion of the supply side make it possible that debt expansion comes without price inflation as measured by the Consumer Price Index. The state of the economy appears as sound when in fact the groundwork is laid for the bust. When individual companies achieve cost reductions and nominal demand remains constant, the price level tends to decline. Yet when central banks expand the money supply and aggregate demand rises, the price level need not fall. Even if productivity rates do not rise in a specific country, the entry of many emerging markets into the world economy should come with falling prices. Over the past decades, the productive capacity of the world economy has experienced a gigantic expansion. There has been disinflation but no deflation.

Modern central banks operate on the false claim to stabilize the economy when in fact they are flying blind. Because there are no constant quantitative relations among the variables, central bankers are unable to calibrate their policies. No amount of empirical research can solve this issue because the present economy will always be different from the past economy, and in times of crisis the present economy and its future path will be radically different from its course in the past.

Antony Mueller

Antony P. Mueller is a professor of economics at the Federal University UFS in Brazil where he is also a researcher at the Center of Applied Economics, and Senior Fellow of the American Institute for Economic Research. Antony Mueller earned his doctorate in economics summa cum laude from the University of Erlangen-Nuremberg, Germany. He was a Fulbright Scholar in the United States and a visiting professor at the Universidad Francisco Marroquin (UFM) in Guatemala as well as a member of the German academic exchange program DAAD. Antony Mueller has recently published the book “Beyond the State and Politics. Capitalism for the New Millennium”.