The Effect of Data Lags on Monetary Policy

Advanced, money-using economies occasionally encounter temporary periods of underproduction, where resources are not sufficiently utilized and some workers are rendered unemployed. Since 1980, the United States has experienced five recessions, ranging from 6 to 18 months in duration. The average recession over the period lasted just under a year.

Periods of underproduction are costly in two ways. First, they mean we get fewer goods and services than we would like, given our constraints. Second, since workers gain and maintain skills while working, their temporary unemployment makes them less productive in the future. In other words, we produce less than we are capable of today and we are less capable of producing than we would have been capable of in the future. For these reasons, and perhaps others, we would like to prevent periods of underproduction when possible.

Monetary policy has the potential to reduce the depth and duration of recessions, when they are driven by nominal disturbances. But it takes time to formulate and implement an appropriate monetary policy response. And the monetary authority cannot even begin this task until it realizes there is a problem. Alas, the lags in data collection make it very unlikely that the monetary authority will be able to remedy all but the most long-lasting recessions.

Consider a relatively straightforward question: are we in a recession? I am not asking, “What caused the recession?” or “How severe is the recession?” or “How long will the recession last?” — all of which would be useful to know when formulating an appropriate monetary policy response. No, I am merely asking whether we are currently experiencing a recession. As it turns out, we struggle to answer even this relatively straightforward question in a timely manner.

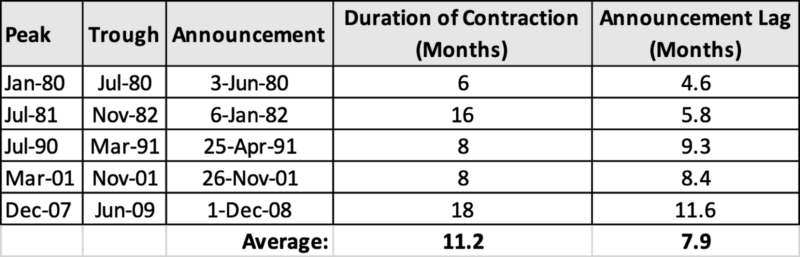

In the United States, the National Bureau of Economic Research’s Business Cycle Dating Committee is widely viewed by economists as the authority for determining when the economy is in a recession. A list of expansions and contractions, beginning in December 1854, is maintained here. The site also includes the announcement dates for peaks (when a recession begins) and troughs (when a recession ends) since 1980. In the following table, I reproduce the data since 1980 and include calculations for the (1) duration of each recession and (2) the number of months between the start of the recession, as identified by the committee, and the announcement of that recession by the committee.

The typical announcement lag — that is, the time between the start of a recession and when the Business Cycle Dating Committee announces the start of a recession — is just under 8 months. That’s a huge lag. The typical recession lasts a mere 3.3 months after the announcement. And, for the recessions beginning in 1990 and 2001, the contraction had ended before the announcement of the contraction’s start had been made!

One cannot expect the monetary authority to formulate and implement an appropriate monetary policy response if it does not know the economy is in recession until that recession is over. But, even when it knows, it often has very little time to do much about it.

There are two caveats in order here. First, the Business Cycle Dating Committee does not intend to announce recessions in a timely manner in order to facilitate the successful conduct of monetary policy. Rather, it intends to provide the most accurate assessment of when a recession begins and ends for historical classification. That almost certainly means it is more conservative in announcing recession dates — waiting until it is absolutely sure — than it would be if it were trying to facilitate monetary policy. The Federal Reserve relies on a host of indicators and constructs elaborate forecasts to make its own assessment of the state of the economy. It does not wait around for the NBER to certify that a recession has begun.

Second, it might be argued that the successful conduct of monetary policy explains why the typical recession has been so short since the 1980s. Perhaps recessions would have been longer and deeper if the Fed were not engaged in countercyclical policy.

Despite these two caveats, however, the point remains: it takes time to collect and analyze data. While it might not take as long to collect sufficient evidence for policy as it does to provide an authoritative statement for the historical record, the known time for the latter gives us a good reason to be concerned about the unknown time for the former. After all, any policy conducted on the evidence available prior to when the Business Cycle Dating Committee feels confident enough to state that a recession has begun is necessarily conducted on a less certain assessment of the state of the economy.

Likewise, the recognition that monetary policy may have reduced the duration of recessions in no way invalidates the claim that there remains a considerable amount of underproduction that the monetary authority is unable to do much about. If monetary policy is conducted based on historical data, occasional periods of underproduction, while perhaps short in duration, are inevitable.

It is difficult to conduct monetary policy effectively. It takes time to formulate and implement an appropriate monetary policy response. That task is made all the more difficult by the lags of data collection. Recognizing the existence of these lags does not imply that the Fed is incapable of reducing the depth and duration of recessions. However, it should instill a sense of humility in those of us considering what the Fed might accomplish in practice.

William J. Luther

William J. Luther is the Director of AIER’s Sound Money Project and an Associate Professor of Economics at Florida Atlantic University. His research focuses primarily on questions of currency acceptance. He has published articles in leading scholarly journals, including Journal of Economic Behavior & Organization, Economic Inquiry, Journal of Institutional Economics, Public Choice, and Quarterly Review of Economics and Finance. His popular writings have appeared in The Economist, Forbes, and U.S. News & World Report. His work has been featured by major media outlets, including NPR, Wall Street Journal, The Guardian, TIME Magazine, National Review, Fox Nation, and VICE News. Luther earned his M.A. and Ph.D. in Economics at George Mason University and his B.A. in Economics at Capital University. He was an AIER Summer Fellowship Program participant in 2010 and 2011.