The Economic Future of a Negative Interest Rate World

Following on from my previous article — “The Pension Fund Apocalypse” — these are just a few of last month’s stories.

-

Danske Bank of Denmark introduces the first negative 10-year fixed-rate mortgage.

-

The German Finance Ministry voices disappointment at the lack of demand for 30-year zero-coupon bonds.

-

The U.S. and Sweden contemplate issuing 50-year and 100-year bonds.

These are all cause for concern.

Excessively low interest rates support assets, favor the rich over the poor, favor the rentier over the business investor, encourage leverage and stock buybacks over capital expenditure and equity-capital formation. Income inequality grows, and social instability follows. Corporations that, under a more normal interest rate regime, would have been placed into receivership are able to continue to operate. New, more innovative enterprises, which should thrive as inefficient incumbent corporations exit the gene pool, are stifled at birth by a dearth of investment and lack of opportunity. Trend economic growth suffers. In an excessively low–interest rate environment, financial sleight of hand trumps improvement in total factor productivity every time.

Are We Nearly There Yet?

Since the great financial crisis of 2008–9, global economic growth has been sluggish when compared with past recoveries. The slashing of interest rates spawned a new credit cycle, protecting the overextended corporations and individuals who, during the previous boom, borrowed too heavily.

The problem in 2008 was too much debt, and the predictable knee-jerk regulatory response was to tighten bank capital requirements. Had that been the sole response, an even-deeper recession would have ensued. Many companies would have defaulted, investors would have been wiped out, and asset markets would eventually have cleared. Painful, but necessary, capital destruction is the nuclear solution to an overblown credit binge, but in a caring modern democracy the collateral damage to the electorate is too great for any elected administration to contemplate.

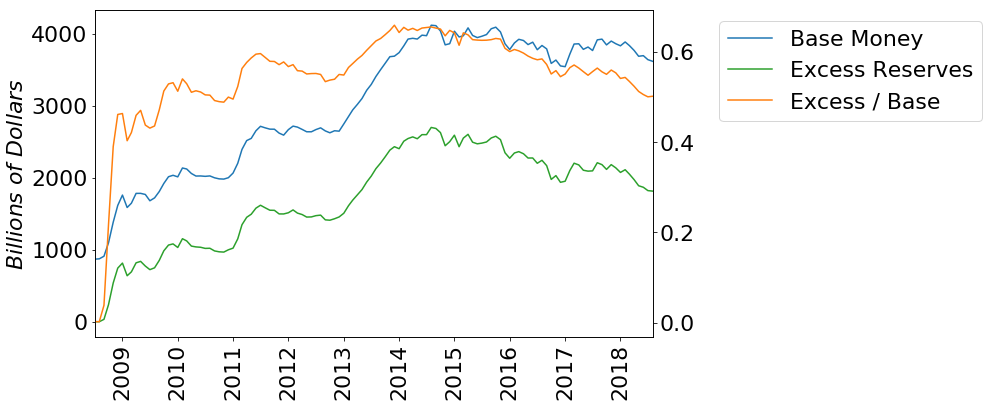

The actual policy response took different forms from country to country. Forsaking the advice of Walter Bagehot, who stated that the function of a central bank during a panic was to lend freely at a penalty rate against good collateral, the Federal Reserve cut interest rates, lending freely, at a far-from-penalty rate, against poor collateral. Even this monetary largesse failed to suffice, prompting the U.S. Treasury to introduce the Troubled Asset Relief Program, enabling bloated U.S. financial institutions to walk away from large swathes of their nonperforming loans. The Fed, not wishing to be upstaged by the Treasury, then embarked on a policy of quantitative easing (QE), whereby it purchased U.S. Treasury bonds in the secondary market in order to reduce interest rates across the maturity spectrum. This reduced capital costs for dollar borrowers large and small.

In Europe, where 28 national treasuries were unable to agree on an approach to nonperforming loans, the European Central Bank (ECB) was forced to cut interest rates even more aggressively than its U.S. counterparts. It also implemented its own version of QE.

Denmark was the first country to adopt negative interest rates (July 2012), but it was Japan, which had been wrestling with the fallout from the twin forces of an aging population and a credit bubble since 1989, that became the petri dish in which financial alchemy was tested. Quantitative and Qualitative Easing (QQE) followed, allowing the Bank of Japan (BoJ) to buy corporate bonds and even equities. Negative–interest rate policy followed in January 2016.

QQE remains a predominantly Japanese affair, but once ECB President Mario Draghi realized that saying “Whatever it takes” would entice the financial markets to test the stiffness of his resolve, the ECB also began acquiring corporate bonds. It has yet to buy stocks, but it is known to be contemplating the provision of “permanent capital” come the next crisis.

The latest BoJ ruse, “yield-curve control,” is aimed at holding 10-year government bond yields at zero. This still allows pension funds the freedom to embrace the longest-maturity debt, in order to glean a few basis points of income. In Switzerland, and the less profligate countries of the Eurozone, it may be too late to follow the Japanese. As the table below shows, rates are too negative and expectations, to judge by the slope of the one-year/two-year yield curve, are that rates will either become more negative or remain at current levels. If an inverted yield curve is the harbinger of recession, there may be trouble ahead.

For finance ministries, zero interest rates on government bonds are a blessing and a curse. For the first time in history, they can raise capital for nothing or even receive an interest payment for their trouble. However, a large proportion of that gain is due to purchases by their own central banks, which, in purchasing these bonds at negative yields and holding them to maturity, incur actual losses that will have to be met by their governments. There are, of course, other bond buyers, such as pension funds and insurance companies, that are obligated to purchase their government’s debt obligations. Central banks do not operate in isolation.

Apart from a reduction in central bank profitability, all may remain, ominously, well until inflation creeps back to life and interest rates start to rise. An aging demographic, which saps a nation’s propensity to consume, will subdue price increases for decades to come, but a chronic lack of corporate investment will eventually lead to shortages. Between 1915 and 2014, U.S. bonds returned 4.3 percent. Imagine the impact on government finances if bond yields return to the mean.

The Leveraged-Asset Bubble

The effect that an artificially low interest rate has on an economy is pernicious. Asset markets are supported, and it raises the point at which they clear, but it also reduces the need for companies to improve internal efficiency. For corporates, borrowing becomes preferable to issuing equity. Firms become more leveraged. The managers of these businesses have an incentive to improve profitability per share by issuing debt and retiring equity capital. They are deterred from raising new capital for other purposes; stock buybacks are safer than speculative projects, especially when you cannot divine what discount rate to use in order to assess the potential of a project.

For households, lower interest rates encourage borrowing to buy assets. The most efficient form of collateralized borrowing available to individuals is that which is secured against property. With falling interest rates comes more affordable mortgage financing, boosting property prices. As mortgage-servicing costs fall, those who are able to borrow get ahead of those who are excluded by virtue of low income or lack of regular employment. A rentier class has always existed, but artificially low interest rates swell their ranks substantially. In August 2019, Danske Bank, a Danish bank, began offering negative–interest rate mortgages, much to the consternation of its customers; other countries are bound to follow.

And what of the poor, the unemployed, those unable to clamber onto even the first rung of the property ladder? Populist politicians will seize the opportunity to pander to the dispossessed voter. They will promise boldly, knowing that, once elected, they can lean on their notionally independent central banks and be paid to borrow at no apparent cost. The self-financing social safety net will scoop up vagrants, waifs, and strays, averting a rebellion and buying loyalty. Until the cycle of leverage needs to be unwound, the gravy train will rumble inexorably onward.

Gravy Train Spill Creates Chaos

The next step in the central bank experiment may be to embrace really negative rates, not just a handful of basis points but several percentage points. Banks will have to charge individual customers higher fees for current account services. A bank solvency crisis may ensue as customers withdraw cash to stuff mattresses. The velocity of circulation of money will trend even lower.

In a recent publication from the Federal Reserve Bank of San Francisco — “Negative Interest Rates and Inflation Expectations in Japan” — the authors observe that cutting rates at or near the zero bound in Japan has led to lower anchored inflation expectations. They advocate that central banks take preemptive action to avoid the uncertain impact on economic activity and inflation of reducing rates toward or below the zero bound.

In the long run, the deleterious effect of negative interest rates turns economic theory on its head. The concept of time preference dictates that, all other things equal, there has to be an incentive for homo economicus to defer consumption. Positive interest rates are that incentive, and in an unhampered market they will always be positive. If, however, interest rates are driven negative by the actions of the state or its central bank, time preference is inverted and traditional economic incentives are corrupted. Individuals and corporations are paid to borrow and consume goods or assets.

The unalloyed power of this corruptive process was evident during the asset boom of the last decade, long before interest rates turned negative. What is not seen amid the credit-and-asset bubble is that, for the economy to grow sustainably, productive investment is required. Before there can be capital available for investment, there has to be saving. In the thrall of negative interest rates there is a clear incentive to borrow and a disincentive to save. This is Ponzi finance; it has turned time preference on its head, driving us to borrow from tomorrow to consume today.

In order to enhance its earnings per share, a profitable company may defer capital investment. This works in the short term, but if it defers investment indefinitely it will eventually cease to be a going concern. If a country chooses the same course of action, it will front-load economic growth in the short run but impoverish its people in the longer term, diminishing the trend rate of economic growth until it reaches the point where its economy physically shrinks.

Negative interest rates may be driving us toward the Gotterdammerung of the market-based economy. Government spending, much of which is nonproductive, is fast becoming the only driver of economic growth. With the currency and interest rates manipulated by the state, little remains free.

Colin Lloyd

Colin is a macroeconomic commentator, writer and presenter, based in London, England. He has worked for asset managers in commodities, money markets, capital markets, equities and foreign exchange since the early 1980’s and writes In the Long Run. He is a contributor to several free-market publications including The Cobden Centre and was a 2017 runner-up for the 2017 Richard Koch Breakthrough Prize awarded by The Institute of Economic Affairs.