Stagflation: Can It Happen Again?

All Keynesian roads lead to stagflation. This happened in the 1970s. Will it also be the case in the 2020s? Stagflation signifies the combined appearance of stagnation and inflation. In the 1970s, the main industrialized countries suffered from the combination of low economic growth, high rates of price inflation, persistent underemployment, and widening budget deficits. In the United States, the price inflation rate and the unemployment rate reached double digits from the 1970s until the early 1980s. Fiscal and monetary expansion prepared the way for the outbreak of the stagflation.

Over the past 10 years, as a reaction to the crisis of 2008, governments and the monetary authorities applied similar policies. Will the result this time too be a global stagflation?

Time Lag

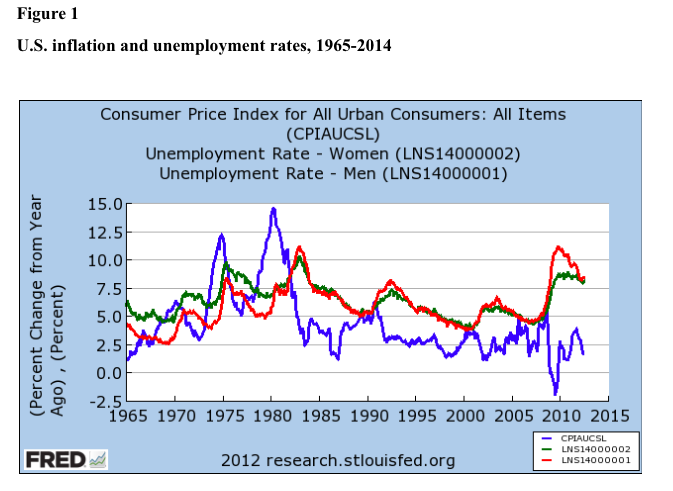

More than a decade of monetary and fiscal abuse preceded the onslaught of price inflation in the 1970s. Despite rising deficit spending and the expansion of the money supply, the price level had remained relatively stable throughout the 1960s. It wasn’t until 1973 that hell broke loose. In a short period of time, the inflation rate shot up together with the unemployment rate (figure 1).

Confronted with stagflation, policy makers were at a loss. Keynesianism had become the leading paradigm. This school proclaimed that recessions were a thing of the past. With the appropriate fiscal and monetary policies, the economy could be kept forever on the path of inflation-free steady growth and high employment. Yet when the policy makers applied the recipe, each round of expansionary policies brought down unemployment only for a short time, and when the effect of the stimulus petered out, the level of unemployment was higher than before.

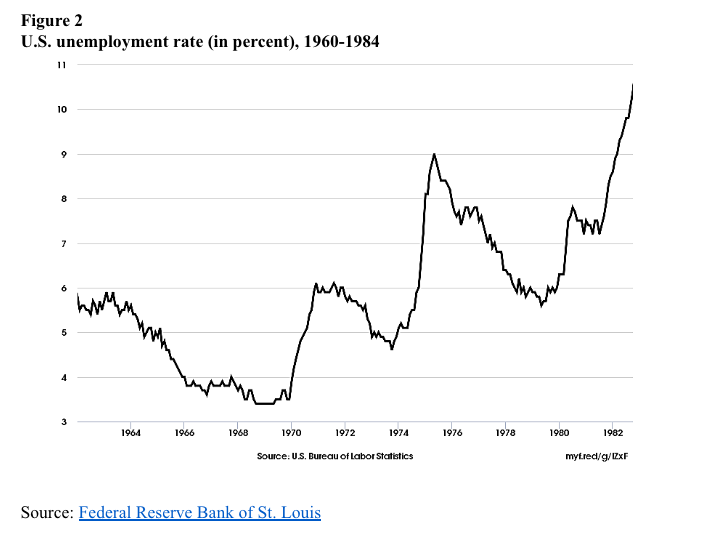

As one can see in detail in the graph below (figure 2), the unemployment rate rose in waves. Each phase of expansionary measures had at first some effect of lowering the unemployment rate, but the effect was not lasting. After every new application of stimulus policy, the level of unemployment became higher than before.

Economic Policy

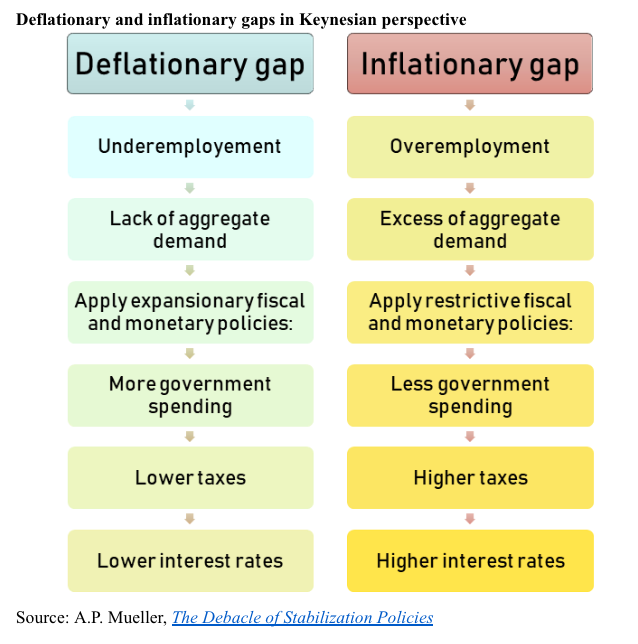

According to the Keynesian doctrine, the economy can be either in a deflationary or an inflationary gap but not in both states at the same time. The doctrine postulates that inflation could not show up together with recession. Likewise, a deflationary gap must come along with a falling price level and rising unemployment. As the Keynesian theory diagnoses recession as the result of a lack of demand, the government must apply expansive monetary and fiscal policies. In contrast, an inflationary gap results from an excess of demand, which leads to inflation and over-employment. Here, the Keynesian theory says, the right policy is a fiscal and monetary contraction (table 1).

According to the economic model of the Keynesians, aggregate demand determines economic activity. Therefore, the policy recommendation says that if there is insufficient private demand, the public sector must jump in. With this theory, Keynesianism stands in contrast to classical economics, according to which the growth of an economy depends on production. For the classical economists, the supply of goods generates the means for the demand for goods, as stated by Say’s law. According to the classical theory, economic imbalances show that technical innovations or changes in consumer preferences or other disturbances require the restructuring of the economy’s capital structure — a task that falls within the competence of the entrepreneurs.

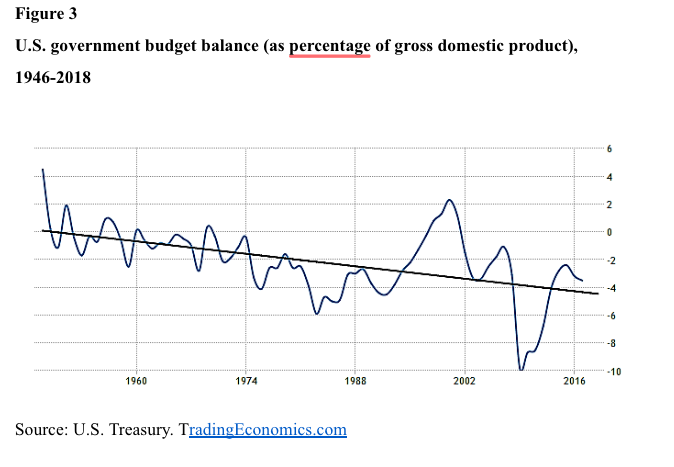

For the Keynesians, in contrast, economic stabilization is the job of macroeconomic policy makers. Now, however, confronted with stagflation, the policy makers knew no answer. While doing away with unemployment would require expansive policies, the fight against inflation would need contractionary measures. Faced with stagflation, fiscal policy became inoperative because high unemployment and stagnant growth meant widening budget deficits and consequently a mounting public debt (figure 3).

What Happened?

In the 1960s, Keynesianism became the dominant doctrine of central banking. Interest rates had to be low, so the mantra said, to stimulate investment and economic growth. Consequently, the U.S. government ignored its obligation under the Bretton Woods Treaty to limit the dollar emission to the size of its gold stock, and the central bank put no brakes on a further growth of the money supply. This policy led right into a decade of inflation first and stagflation later.

The oversupply of dollars destroyed this system. The central banks in Europe and Japan became the buyers of last resort for the weakening greenback. The world experienced a massive increase in liquidity originating from the oversupply of dollars, which spilled over to the other major currencies. When the central banks in Europe and Japan bought dollars with their own currencies to stabilize the exchange rate, they expanded their domestic monetary base. After a short liquidity-driven boost, the world economy slipped into the stagflation of the 1970s.

At the same time, when Keynesianism was gaining its foothold in politics, monetarism received growing recognition in academia. According to the leading monetarist, Milton Friedman, it was not the market economy that was to blame for the Great Depression, as the Keynesians claimed, but the American central bank’s monetary policy. What the Keynesian diagnosed as insufficient aggregate demand was in fact a monetary contraction.

The experience of stagflation led to a turnaround of monetary policy in the late 1970s when the U.S. central bank embarked upon the monetarist experiment. Now, it was the money supply that became the magic word and the most important guideline for central banking. In the 1980s, the rate of price inflation declined. However, this happened more by accident than by design, because with the onset of the monetarist experiment, the velocity of money circulation, which had been trend-stable for decades, contracted.

What Next?

The stagflation of the ’70s was the result of the mismanagement of the central banks and fiscal policy during the 1960s. In response to the crisis of 2008, the monetary and fiscal authorities have applied a host of expansionary measures. The result has not yet been a broad rise of consumer prices. Yet by implementing interest rates that are below any reasonable level, central bankers have fueled a global speculative frenzy of gigantic proportions. The combined effort of the central banks of the United States, Japan, and Europe to “stimulate” their economies has initiated an asset price bubble.

Which way the present experiment will end — whether the asset price inflation will become a consumer price inflation or whether the collapse of the asset prices will provoke a deflationary depression — remains to be seen. In any case, the lesson to learn is the urgency to reform the current monetary system. The existing monetary regime is a political instrument for the exercise of power, which allows the unrestrained expansion of the welfare state and war-making and the accumulation of public debt. Abolishing the state monopoly on money and recognizing private money as a means of payment would be the first step on the way to reforming the monetary system.

Antony Mueller

Antony P. Mueller is a professor of economics at the Federal University UFS in Brazil where he is also a researcher at the Center of Applied Economics, and Senior Fellow of the American Institute for Economic Research. Antony Mueller earned his doctorate in economics summa cum laude from the University of Erlangen-Nuremberg, Germany. He was a Fulbright Scholar in the United States and a visiting professor at the Universidad Francisco Marroquin (UFM) in Guatemala as well as a member of the German academic exchange program DAAD. Antony Mueller has recently published the book “Beyond the State and Politics. Capitalism for the New Millennium”.