Powell’s New Monetary Regime

During the financial crisis of 2008–9, the Federal Reserve bailed out the firms that were invested in mortgage-backed securities and instruments tied to these securities. The Federal Reserve made massive purchases of mortgage-backed securities and other debt. These greatly expanded the monetary base. To prevent inflation, the Federal Reserve simultaneously began to pay interest on excess reserves. This incentivized banks to place the extra base money on account at the Federal Reserve.

Last year I asked whether the Fed could manage the excess reserves. Others have explored this question. These authors have mourned the disappearance of the corridor system, where the Federal Reserve paid a rate of interest on excess reserves that was below the interest rate — the effective federal funds rate — charged by banks in the overnight lending market. The ceiling of this “corridor” was the discount rate charged to banks that, with stigma, borrow from the Federal Reserve. Instead, in the current system, the rate paid on excess reserves serves as a ceiling on the effective federal funds rate. With this regime, banks, if they are able, are better off leaving their money with the Federal Reserve.

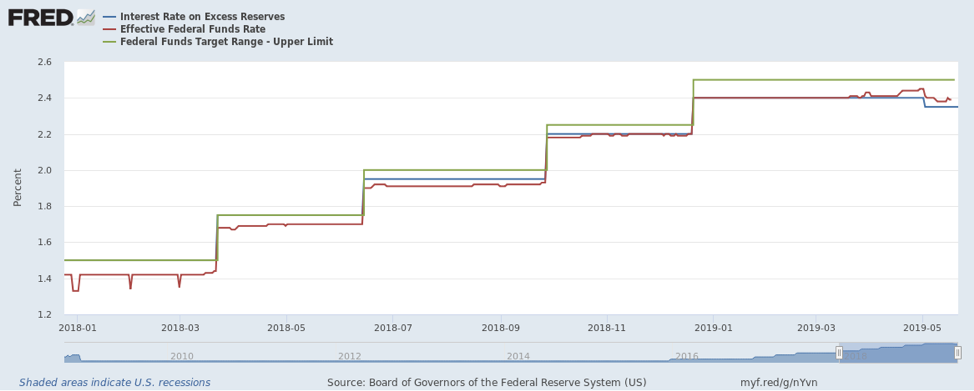

So far, the Federal Reserve has answered our question with a resounding “Yes!” Shortly before my article in September, Federal Reserve policy set the stage for a return to the corridor system. If you do not carefully follow the data, you may have missed this. While Fed Chair Jerome Powell suggested that Federal Reserve policy might not tighten as much as anticipated, he simultaneously changed the regime that dominated the last decade of monetary policy by lowering the rate of interest paid on excess reserves below the federal funds rate target. I will discuss this change in more detail after reviewing the Fed’s policy instruments.

Policy Instruments

To understand the change, one must be aware of two policy instruments available to the Federal Reserve: open market operations and payment of interest on excess reserves. Imagine that the Federal Reserve has a money-printing machine (the truth is not so different). When it wants to ease market conditions, it prints new money and spends it. The different policy instruments concern how the Federal Reserve spends this money.

First, the Federal Reserve can use its money-printing machine to purchases bonds. This practice is part of open market operations. (Conversely, the Federal Reserve can sell bonds to reduce the amount of money in circulation.) It can purchase bonds that are scheduled to be repaid relatively soon with the intent of lowering short-term rates. In particular, officials seek to impact the federal funds rate. At this rate, banks lend to one another overnight to meet temporary shortfalls that place their reserve ratios under the legal minimum.

Second, the Federal Reserve can use its money-printing machine to pay interest on excess reserves. These excess reserves are money held on account at the Federal Reserve above minimum reserve requirements. The Federal Reserve pays banks a risk-free rate of return for their excess reserves. This removes base money from circulation, preventing it from causing inflation.

Policy after the Crisis

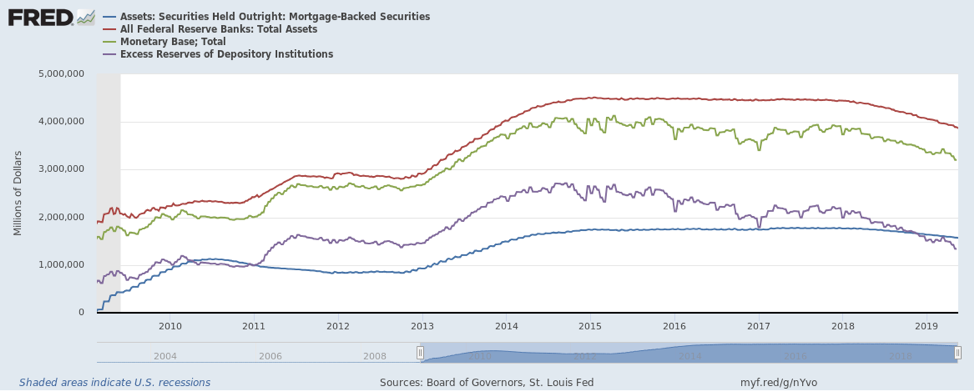

In 2008, operations conducted by the Federal Reserve were referred to as quantitative easing (QE). QE refers to a special case of the Federal Reserve using its money-printing machine, often to buy mortgage-backed securities. So much money was printed as part of the QE program that the quantity of base money made available by the Federal Reserve increased fivefold from about $850 billion to over $4 trillion in just over five years.

If the Federal Reserve had let this new money circulate in the economy, the annualized rate of inflation would have been at least in the double digits and might even have reached the triple digits. Aware of the potential effects of its money printing, the Federal Reserve paid interest on excess reserves For years this interest rate stood at 0.25 percent, before rising modestly under Janet Yellen. In the most extreme case, money held as excess reserves amounted to over 60 percent of the stock of base money. With Powell at the helm, this value has consistently fallen, reaching just under 42 percent by the end of April 2019.

Powell continues to shrink the Federal Reserve’s balance sheet and plans to continue doing so into September. One might expect that this reduction would necessarily be accompanied by a negative aggregate demand shock. That is, the reduction of base money might be expected to lead to a fall in the total value of expenditures in the United States (nominal GDP).

Much as Ben Bernanke and Yellen successfully avoided tremendous inflation, Powell is avoiding deflation. Although he has been increasing the federal funds target, he has also changed the policy that governed payment of interest on excess reserves. Starting in June 2018, Powell has reduced the rate paid on excess reserves compared to the upper end of the range of the federal funds target. Before this point, they had been equal. The difference between these rates increased again at the end of 2018 and again as April turned to May. About one month before the last rate reduction, the effective federal funds rate rose above the rate of interest paid on excess reserves. The interest paid on excess reserves has ceased to be a ceiling for the federal funds rate.

Powell is incentivizing banks to invest the funds that were previously sterilized by the relatively high rate of interest paid on excess reserves. By this means, Powell can coordinate a reduction in the Federal Reserve’s balance sheet while maintaining growth in aggregate expenditures (i.e., nominal GDP).

Powell’s strategy represents a turning point in monetary policy at the Federal Reserve. The payment of interest on reserves is being adjusted to promote increases in the effective stock of base money without requiring the Fed to expand its balance sheet. The indirect approach has proven useful. However, the responsiveness of the volume of excess reserves to the rate paid on those reserves may grow as the spread between the effective federal funds rate and the rate paid on excess reserves grows. In particular, if the difference between these rates approaches or exceeds the portion of the federal funds rate representing the risk premium, we can expect a massive outflow of base money held as excess reserves. So far, the discrepancy between the two rates does not appear to have approached this amount.

It is also possible that even when the Federal Reserve stabilizes the balance sheet, increases in this discrepancy can continue to diminish the level of excess reserves, although Powell has given no indication of such an intention. This regime change will surely have an impact on the growth rate of nominal GDP, the rate of inflation, and the stock of base money. What’s unclear is how the Fed will use the tools they have, and whether or to what extent to which they understand the regime in which they are now operating.

James L. Caton

James L. Caton is an Assistant Professor in the Department of Agribusiness and Applied Economics and a Fellow at the Center for the Study of Public Choice and Private Enterprise at North Dakota State University. His research interests include agent-based simulation and monetary theories of macroeconomic fluctuation. He has published articles in scholarly journals, including The Southern Economic Journal, the Journal of Entrepreneurship and Public Policy, and the Journal of Artificial Societies and Social Simulation. He is also the co-editor of Macroeconomics, a two-volume set of essays and primary sources in classical and modern macroeconomic thought. Caton earned his Ph.D. in Economics from George Mason University, his M.A. in Economics from San Jose State University, and his B.A. in History from Humboldt State University.