Soft Jobs Report Suggests Caution, Not Panic

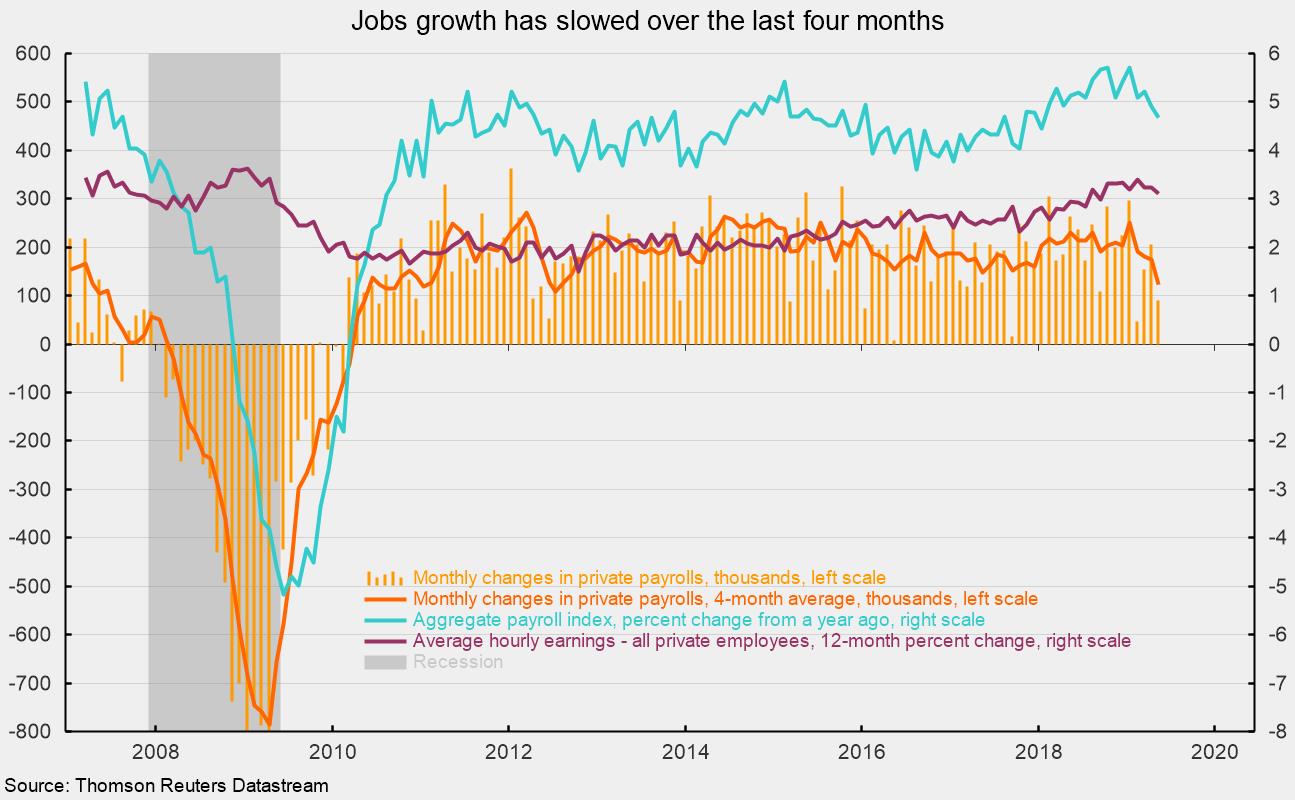

U.S. nonfarm payrolls added 75,000 jobs in May, below the consensus expectation of 185,000. The prior two months were revised downward by a combined 75,000, putting the April gain at 224,000 and the March increase at 153,000. Excluding the government sector, private payrolls added 90,000 in May following downwardly revised gains of 205,000 in April and 153,000 in March (see chart).

Job creation has decelerated over the past four months. Over the four months ending in May, private payrolls added an average of 124,000 per month, the slowest pace since July 2012 and about half the 252,000 average for the four months through January 2019 (see chart). While the slow pace of job creation is worrisome, over the last three economic cycles the four-month average gain fell below 100,000 about a year before the peak of the cycle. Employment is a coincident indicator, and no one knows what will happen over the next year, but the weakness over the last four months suggests caution, not panic.

Within the 75,000 gain in jobs, goods-producing industries added 8,000 employees in May, below the average gain of 36,000 over the past year. Durable-goods manufacturing and construction led with additions of 4,000 jobs each, both below the 12-month averages of 12,000 and 18,000, respectively. For private service-producing industries, which typically account for the lion’s share of job creation, payrolls added 82,000 workers, led by a 33,000 increase in professional and business services (versus a 12-month average of 42,000). Leisure and hospitality added 26,000 while the health care and social-assistance industries together added 27,000 jobs in May. Retail lost 8,000 workers, the fourth consecutive month of decline, while information services lost 5,000. Across the 258 industries in the private sector, 54.8 percent were adding jobs in May, below the five-year average of 61.3 percent but solidly above the 50 percent threshold associated with recession.

The unemployment rate was unchanged in May, holding at 3.6 percent, the lowest since 1969. A total of 176,000 people entered the labor force, leaving the participation rate steady in May at 62.8 percent. The participation rate remains well below the 66.0 percent rate that prevailed from 2004 through mid-2008.

Average hourly earnings rose 0.2 percent in May, resulting in a 12-month gain of 3.1 percent (see chart again). Gains in average hourly earnings have been below gains in previous cycles. The average length of the workweek was unchanged at 34.4 hours in May. Average weekly hours have been bouncing around between 34.3 and 34.6 hours since 2012.

Combining payrolls with hourly earnings and hours worked, the index of aggregate weekly payrolls rose 0.3 percent in May and is up 4.7 percent from a year ago (see chart). Though this aggregate measure has decelerated in recent months, it has posted relatively steady year-over-year gains in the 4 to 5 percent range since 2011.

A number of recent surveys suggest rising tariffs and heightened uncertainty over trade policy appear to be raising concerns among individuals and businesses. Those concerns could translate into slower hiring and investment by businesses and slower spending by consumers. The 10-year Treasury note yield has already fallen to just over 2 percent from a high of over 3.2 percent as recently as the fourth quarter of 2018, reflecting the growing possibility of a significant economic slowdown or recession. Furthermore, Fed officials have acknowledged concern over the fallout from tariffs, adding to speculation that the Fed may cut rates in order to avoid a recession. Since the Fed has no better foresight than anyone else as to how the economy and trade policy will unfold, it is unwise for the Fed to try to preemptively micromanage the economy.

The preponderance of economic data still suggests continued economic expansion over the coming months. However, the fallout from trade wars including increased caution on the part of business and consumers could tilt the scales away from continued expansion. Caution, not panic, remains the appropriate view for the economic outlook.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.