Retail Spending Suggests Caution

Retail sales and food services spending rose 0.3 percent in October following a 0.3 percent decline in September. Over the past year, total retail sales and food services were up 3.1 percent through October, the slowest pace since February.

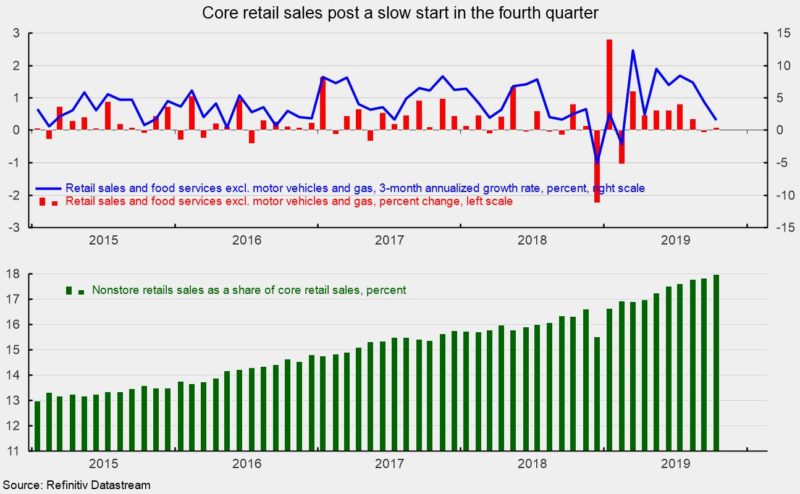

Excluding the volatile auto and energy categories, core retail sales and food services were up 0.1 percent in October after a fall of 0.1 percent in September. Core retail sales had posted six straight monthly gains through August before declining in September. Over the last three months, core retail sales are up at just a 1.5 percent annualized rate, the slowest since February (see top chart).

Details of the October retail sales report suggest even more caution as the strongest areas of spending are ones typically regarded as staples while the categories typically considered more discretionary fell. Overall, there were declines in seven retail-spending categories, while five categories posted gains and one was essentially unchanged. Declines were led by a 1.0 percent drop in clothing and accessories stores, a 0.9 percent drop for furniture stores, and a 0.8 percent fall for sporting goods, hobby, musical instrument, and book stores. Discretionary spending fell 0.1 percent for the month while discretionary spending excluding autos fell 0.5 percent.

Gains were led by a 1.1 percent rise for gasoline station sales. The gain in gas station sales reflects a 1.7 percent jump in average retail prices of gasoline. Also posting gains were motor vehicles and parts stores, up 0.5 percent for the month despite a drop in unit sales to a 16.55 million-unit annual rate from a 17.14 million-unit rate in the previous month, and a 0.9 percent increase for nonstore retailers, predominantly online shopping. This category has been growing very robustly for years, posting a gain of 14.3 percent over the last 12 months. Nonstore retailers now account for 18 percent of core retail sales (see bottom chart).

Retail spending data for October adds to the uncertainty about future economic growth. Turmoil in policy, including trade policy and monetary policy, may be starting to impact business and consumer confidence. If the softening in confidence translates into significant restraint in consumer spending, hiring, and business investment, the probability of recession increases dramatically. For now, economic expansion is the most likely path, but caution is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.