Retail Spending Hits A Record in October but Breadth Narrows

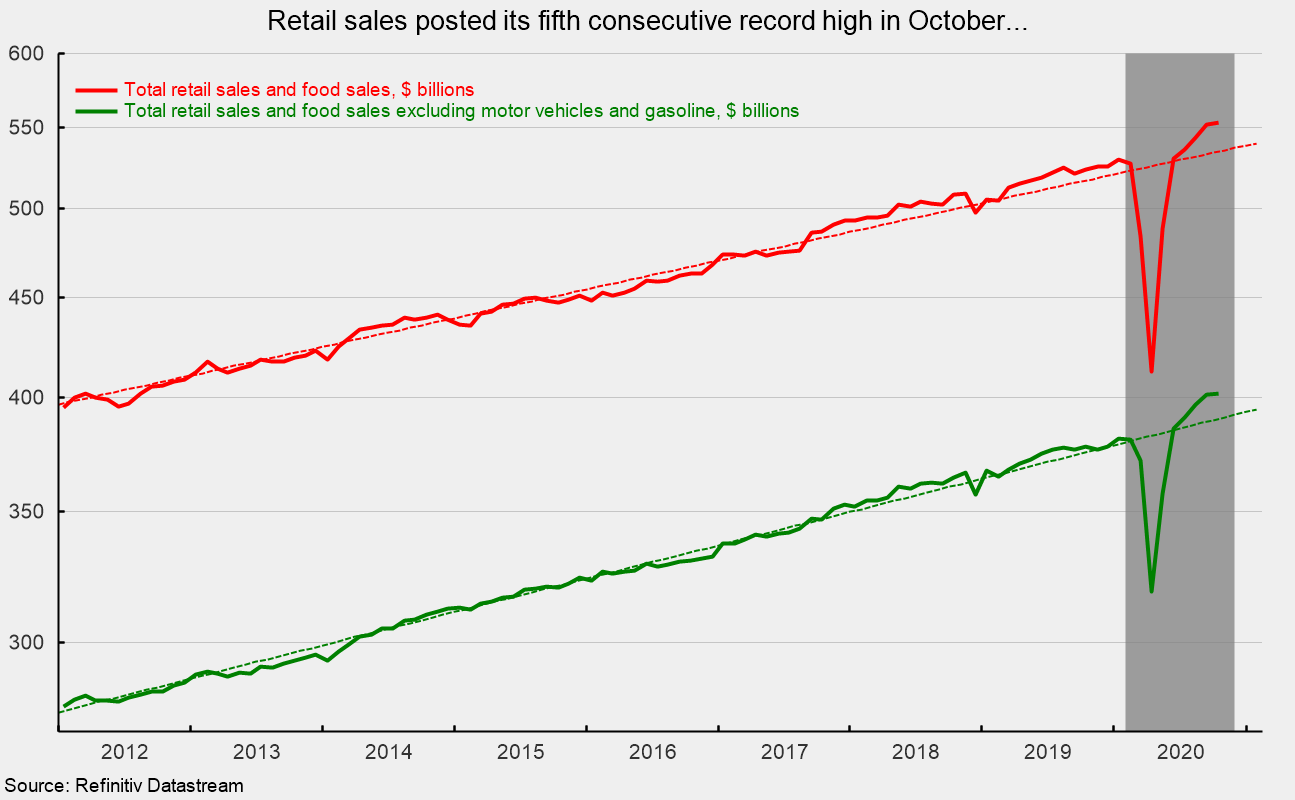

Retail sales and food-services spending posted another gain in October, rising 0.3 percent from the prior month. The October gain was the sixth in a row following two devastating declines in March and April. October is the fifth consecutive record high (see first chart). Core retail sales, which exclude motor vehicles and gasoline retailers, posted a 0.2 percent gain for the month putting them well above trend and at the fifth consecutive record high as well (see first chart).

From a year ago, total retail sales are up 5.7 percent while core retail sales show a 6.5 percent rise. Both are back to the growth rates achieved just before the outbreak of Covid-19 and implementation of government lockdown policies. The current 12-month rates are well above the five-year annualized rates of 3.7 percent and 3.9 percent, respectively, for the five years from 2015 through 2019.

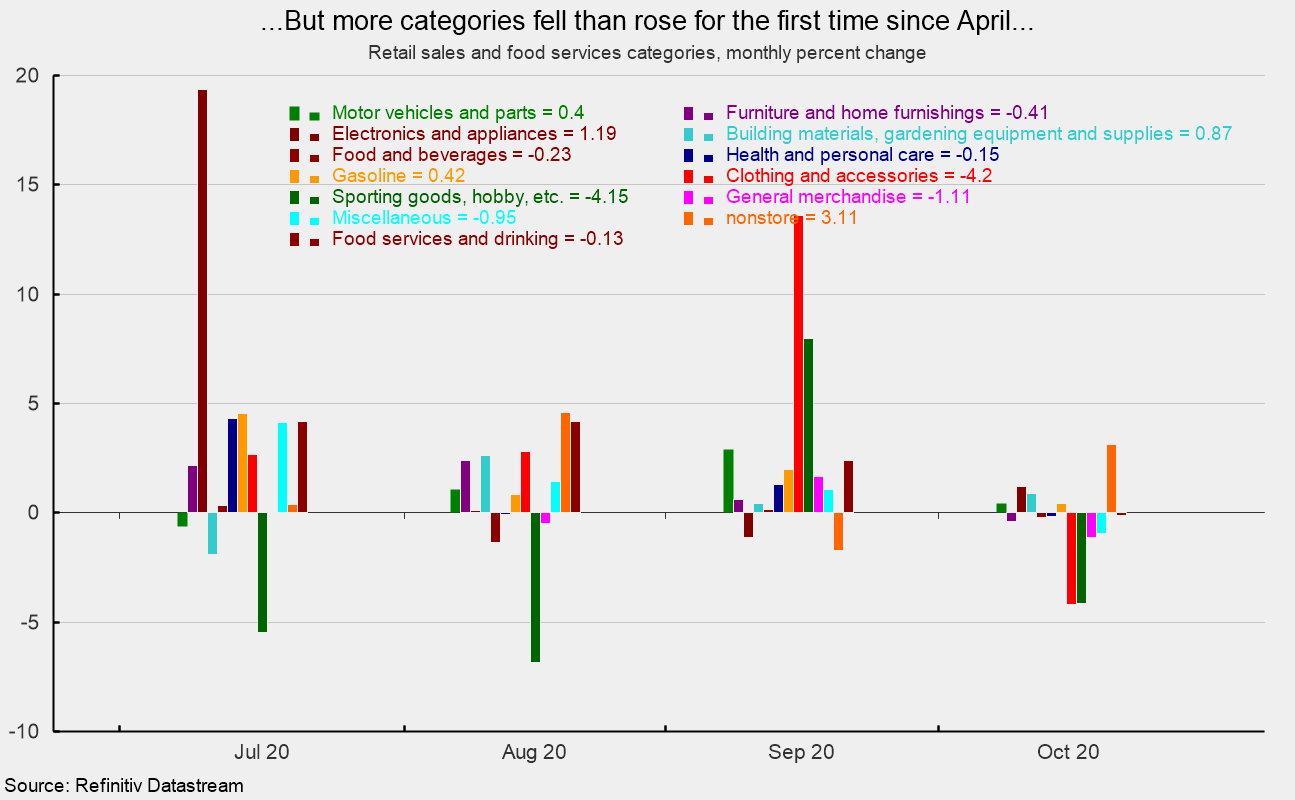

Despite posting another record high, results across the various categories of retailers were mostly weaker in October. Eight of the thirteen major categories reported declines in October sales (see second chart). Decliners were led by clothing and accessories stores and sporting goods, hobby, musical instrument, and book stores, both posting declines of 4.2 percent. Gainers were led by a 3.1 percent gain for nonstore retailers, primarily online shopping (see second chart).

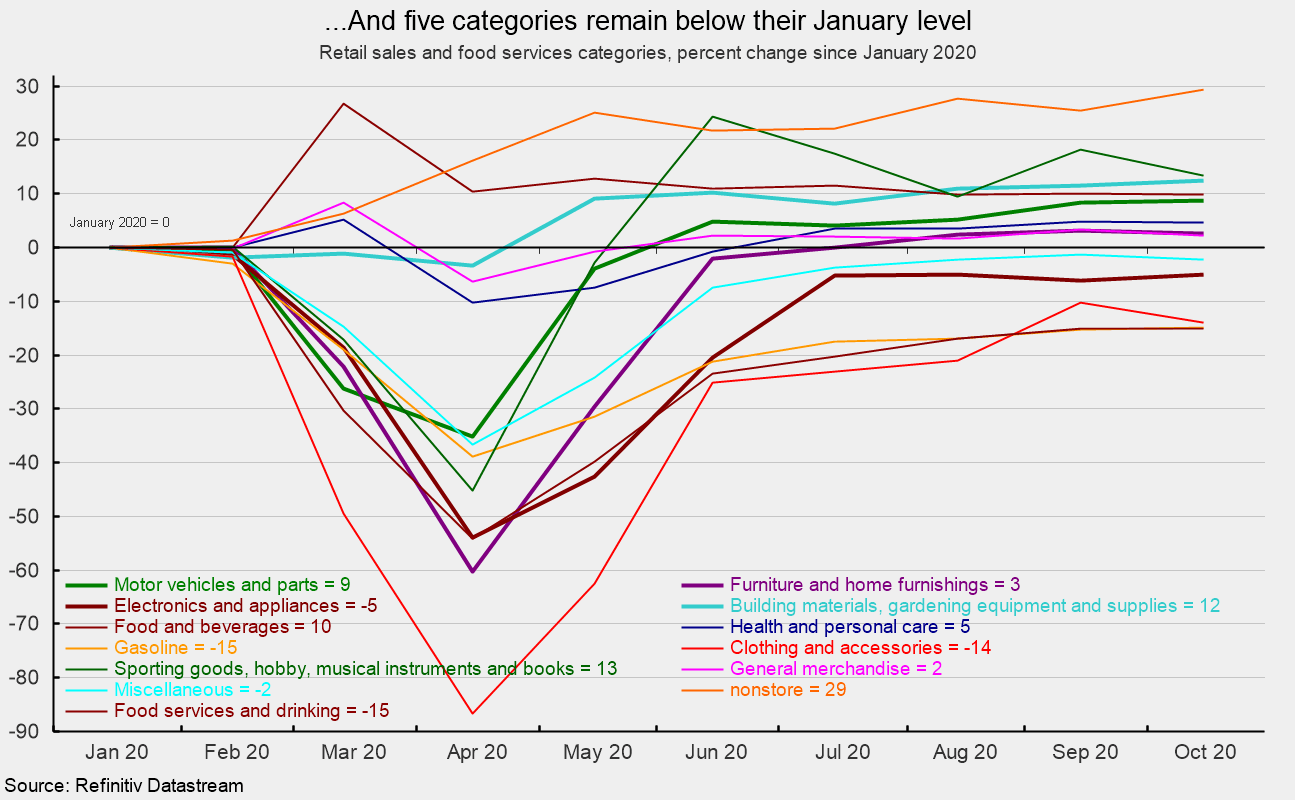

The October results leave five of the 13 categories with sales below their pre-lockdown levels (see third chart). Gasoline stations and restaurants are both 15 percent below January followed by clothing and accessory stores (14 percent below), electronics and appliances (5 percent below), and miscellaneous store retailers (2 percent below).

On the upside, nonstore retail sales are 29 percent above January 2020 levels (see third chart). Nonstore retail sales now account for 15.9 percent of total retail sales, up from 12.9 percent in January 2020 (before the pandemic) and about 8 percent at the beginning of 2012. As a share of core retail sales, nonstore sales account for 21.9 percent, up from 17.9 percent in January and 11.7 percent at the start of 2012.

Retail sales rose to another record high in October as widespread quarantines and lockdowns continue to be eased, and shoppers shift more spending to online retailers. Businesses and consumers continue to emerge from the policy-induced economic coma. However, while aggregate retail spending is at a new high, results still vary greatly by industry.

Uncertainty about the recent progression of the virus and reactionary government policies are sustaining heightened uncertainty and threatening the recovery. A full return to pre-pandemic conditions for the overall economy and the labor market is likely many months, and possibly several quarters away.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.