Rebounding Retail Sales Growth and Low Initial Claims Point to Robust Economy

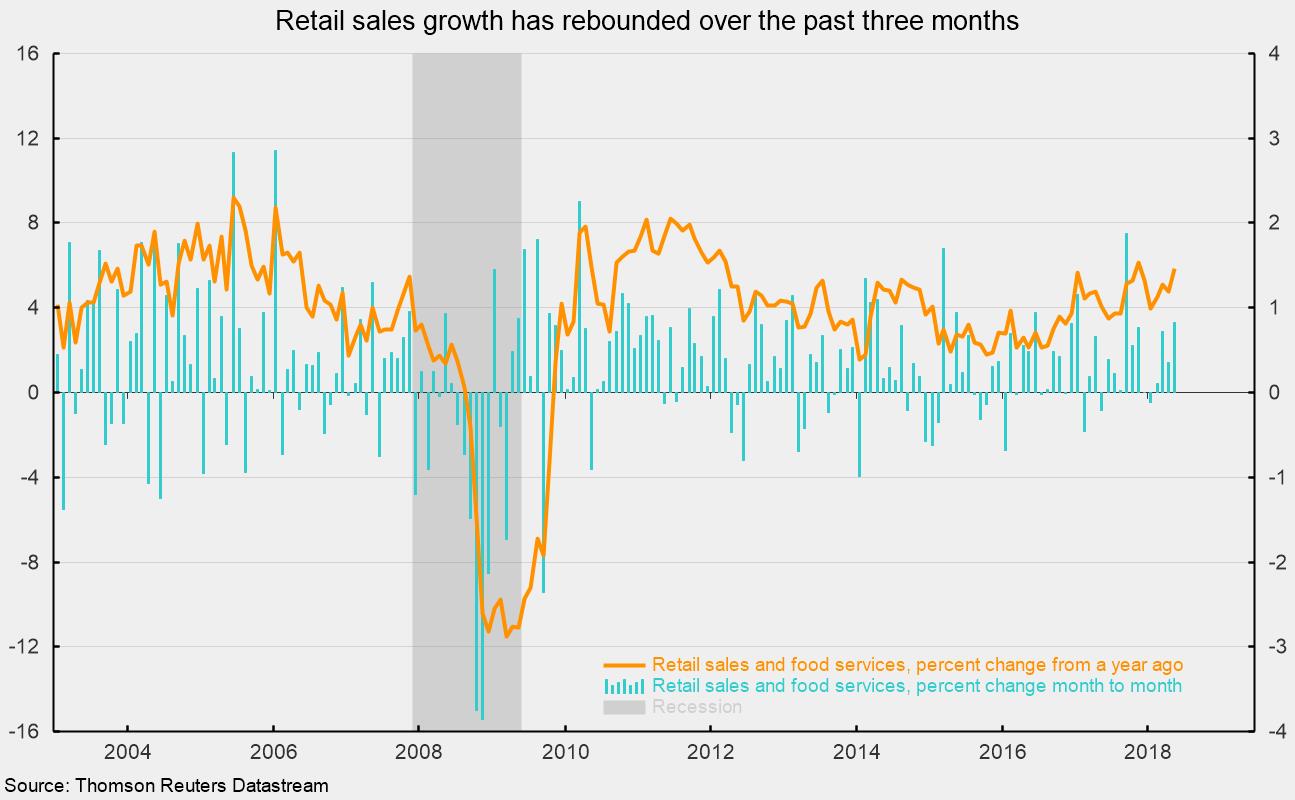

Retail sales jumped 0.8 percent in May, the third strong monthly gain in a row following weak performances in January and February. Over the past year, they are up 5.9 percent, the strongest yearly gain since November 2017 and the second-highest 12-month gain over the last six years (see chart). The robust gains are consistent with the latest results of the AIER Leading Indicators index, which currently stands at a perfect 100 reading.

Gains in retail sales in May were fairly widespread among the components. The only major components to show declines for the month are, first, furniture and home furnishings, down 2.4 percent in May but up 3.5 percent over the past year, and, second, sporting-goods, hobby, music, and book stores, down 1.1 percent for the month and down 0.7 percent for the past year.

Among other categories with strong gains, miscellaneous store retailers had a 2.7 percent gain (7.5 percent from a year ago), building-materials and building-supplies stores gained 2.4 percent (5.2 percent for the year), clothing stores and restaurants both increased by 1.3 percent for the month (5.9 and 5.1 percent for the year, respectively), and general-merchandise stores rose 1.2 percent in May (up 5.0 percent for the last 12 months).

Gasoline-station sales posted a 2.0 percent rise in the latest month, putting the 12-month gain at 17.7 percent, but this category tends to be driven by price changes more than other categories. Average retail prices for gas jumped 5.1 percent for the month.

Online retailers had modest growth in May as sales rose 0.1 percent for the month but are up 9.1 percent from a year ago, second only to gasoline-store sales.

Among retailers of consumer staples, food-store sales were unchanged for the month (but up 3.6 percent from a year ago) while health and personal-care stores gained 0.5 percent (and 2.9 percent for the year).

Retail sales have been regaining momentum over the last few months following a weak start to the year. The outlook for consumer spending is well-supported by a strong labor market, record-high household net worth, and high consumer confidence.

Weekly data on initial claims for unemployment insurance show the labor market remains favorable. Claims fell to 218,000, a drop of 4,000 from the prior week. The four-week average fell to 224,250 from 225,500 in the prior week. The four-week average has been below 300,000 since September 2014, the longest run since the 1970s. As a share of payroll employment, claims continue to hover at record lows.

Overall, today’s data show the economy is robust, supported by the labor market and rebounding consumer spending. Combining these data with strong readings from the AIER Leading Indicators index, the outlook for the economy remains upbeat.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.