Nonmanufacturing Index Rises in August; Initial Claims Lowest Since 1969

Following Tuesday’s report from the Institute for Supply Management suggesting that the manufacturing sector expanded at a faster pace in August, today’s report from the ISM suggests a similar pickup for the nonmanufacturing sector.

The ISM’s nonmanufacturing index rose to a reading of 58.5 from 55.7 in July. For this index, 50 is neutral, with readings above 50 suggesting expansion and readings below 50 suggesting contraction. Typically, the NMI ranges between 50 and 60, with dips below 50 during recessions. Historically, readings above 49.0 have suggested expansion of the overall economy. The August result is the 103rd consecutive reading above 50.

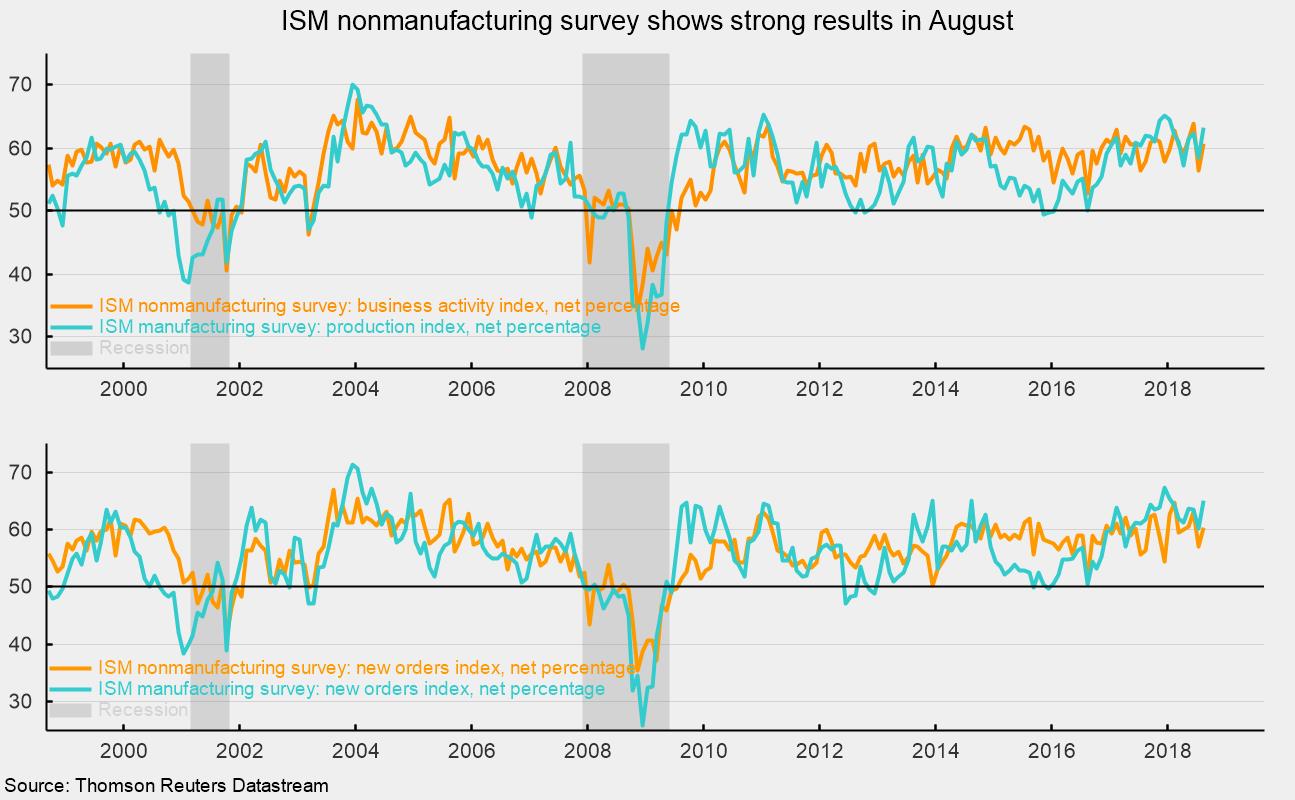

Among the key components of the NMI, the business-activity index (equivalent to the production index in the ISM manufacturing report) was 60.7 in August, up from 56.5 in July. Tuesday’s manufacturing report showed the production index came in at 63.3. For the month of August, 14 industries in the nonmanufacturing survey reported growth while 2 reported contraction.

The nonmanufacturing new-orders index came in at 60.4, up from 57.0 in July. August was the 91st month of readings above 50. The new-export-orders index, a separate index that measures only orders for export, was 60.5 in August and has been above 50 for 19 consecutive months. The manufacturing new-orders index released on Tuesday came in at 65.1 last month. With all four indexes (activity and new orders for nonmanufacturing released today, and production and new orders for manufacturing released Tuesday) above 60, the overall message is ongoing economic strength (see chart).

The nonmanufacturing employment index increased to 56.7 in August, versus 56.1 in July. The favorable readings from this and the manufacturing survey suggest employment likely increased in August. The Bureau of Labor Statistics will be releasing its own employment report for August tomorrow (Friday, September 7).

Supplier deliveries, a measure of delivery times for suppliers to non-manufacturers, came in at 56.0, up from 53.0 in July. It suggests suppliers are falling farther behind in delivering supplies to non-manufacturers, and the slippage has accelerated a bit from the prior month.

The one component that raised concern in the nonmanufacturing report was the prices index. It fell slightly to a reading of 62.8 in August. However, August was the 30th month in a row that the prices index has been above 50. This result suggests nonmanufacturers are experiencing materials-costs increases. The price index in the ISM manufacturing report also fell in August, but to a still-elevated 72.1, versus 73.2 in July.

Today’s report from the Institute of Supply Management suggests the nonmanufacturing sector continued to grow in August. That performance is in line with the report for the manufacturing sector and other recent data that point to ongoing expansion for the overall economy.

The latest weekly initial claims for unemployment insurance fell 10,000 to 203,000 for the week ending September 1. That is the lowest level since 1969. The four-week average, calculated to help reduce volatility, fell 2,750 to 209,500. The strong labor market continues to be the cornerstone of the economic expansion and is complementing strong consumer spending and upbeat consumer attitudes regarding the current economy.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.