Nigeria’s Cash Tax Is a Bad Idea

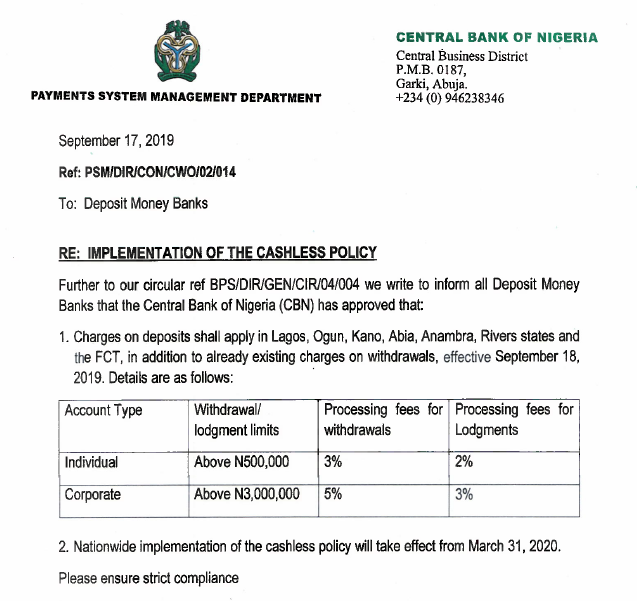

Last month, the Nigerian monetary authorities announced that they will be rolling out a national tax on cash. When Nigerian individuals or businesses deposit large amounts of cash at a bank, they will have to pay up to 3 percent in fees. And when they withdraw cash they will have to pay as much as 5 percent in fees.

Nigeria joins a number of other emerging nations that have adopted policies that try to restrict domestic cash usage. India’s 2016 demonetization of the 1,000- and 500-rupee notes is the most well-known effort. Kenya’s less aggressive 2019 demonetization of the 1,000-shilling note is another.The usefulness of these policies is questionable.

Most Nigerians continue to rely heavily on cash. According to a recent report from EFInA, a Nigerian think tank, just 39.7 percent of Nigerians are banked. Out of this, a quarter of all accounts are inactive. Around 82 percent of Nigerians continue to receive their main income in the form of cash.

The new law (set to be enacted in 2020) will set a fee of 2 percent on deposits by individuals above 500,000 naira (₦) per day (US$1,400) and 3 percent on withdrawals. Businesses that deposit more than ₦3,000,000 per day (US$8,000) will be taxed 3 percent on the excess and 5 percent on withdrawals.

Source: CBN website

In a country where the average salary is around ₦72,000 per month (US$200), a ceiling of US$1,400 is unlikely to be too onerous for most Nigerians. But large businesses that deal in naira banknotes will certainly be inconvenienced by the US$8,000 ceiling. Rather than banking all their cash receipts by the end of the day, some businesses may try to avoid the tax by storing cash until the next day. But storing cash on site is dangerous and expensive.

Alternatively, businesses may try to offload deposit and withdrawal fees onto their cash-paying customers by setting a higher price for goods when cash is used, in which case the incidence of the tax falls on the consumer. Rather than withdrawing small bills and coins to make change for their customers, businesses may prefer to avoid withdrawal taxes and use gum or candy as change, a common practice across low-income countries that inconveniences customers.

The cash tax is one component of the Central Bank of Nigeria’s “Cash-less Nigeria” vision. The CBN notes in its FAQ that unlike “progressive countries of the world,” Nigeria uses too much cash. By penalizing cash usage, it hopes to “enlighten” the public and get them to use electronic-payments options. By doing so, the CBN’s goal is that Nigeria will vault into one of the “top 20 economies by the year 2020.”

The problem with this line of thought is that it confuses correlation with causation. There are many reasons why nations get rich, including strong institutions like the rule of law, clearly defined and well-enforced property rights, and access to sound money. And while it is true that developed nations like Sweden, the U.S., and the U.K. tend to have low cash reliance, they didn’t attain high levels of development because their citizens switched from cash to digital payments. It is more likely that the opposite happened: the adoption of non-cash payments was a byproduct of growing wealth, not its cause. Forcing Nigerians to drop cash in the hope that this will somehow make Nigeria a more prosperous place mixes up the proper order.

In fact, the evidence from Mexico suggests attacking cash may hurt Nigerians.Two recent events involving the ride-hailing company Uber provide an ideal natural experiment for measuring the role that cash plays. In 2016, Uber Mexico began to allow its customers to pay with cash. Prior to then, they had been limited to card payments. Mexico City had to wait until late 2018 for cash to be introduced.

The second event is linked to the 2017 murder of a young Mexican woman — allegedly by a driver at a competing ride-hailing app, Cabify. This led the local government to ban all ride-hailing cash payments in the city of Puebla.

In a recent paper, economists Fernando Alvarez (University of Chicago) and David Argente (Pennsylvania State University) use Uber data to explore how the introduction and banning of cash affected the local cab economies. The introduction of cash to the areas surrounding Mexico City in 2016, but not Mexico City itself, provides the authors with an opportunity to compare Mexico City’s no cash policy to that of the yes cash suburbs. They found that the introduction of cash resulted in twice as many Uber rides purchased relative to a scenario in which cash was prohibited.

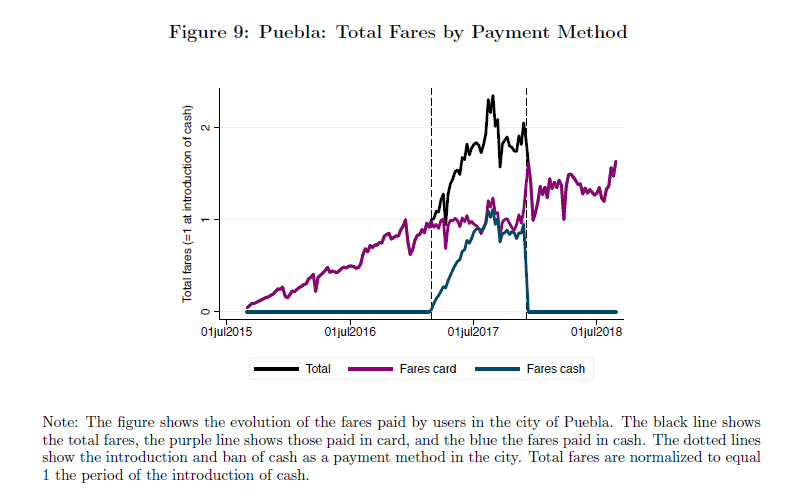

Puebla originally introduced cash in early 2017. Total fares almost doubled. But when it banned cash payments on Uber and other ride apps, Alvarez and Argente found, the number of fares plunged by 60 percent. As the following figure shows, the total number of trips remained 40 percent below pre-cash levels even after cash users migrated to card payments following the ban.

Source: Argente and Alvarez (2019)

Alvarez and Argente make an effort to quantify the value of consumption that Mexicans lose when cash is banned (or gain when cash is added as a payment option). They estimate that around half of the economic value enjoyed by riders who had previously paid in cash prior to a ban ends up being destroyed when cash is prohibited. That’s a sizable loss.

Part of this is due to the fact that cash and credit are not exact substitutes. Once cash is banned, Mexicans who were entirely dependent on cash may have had problems getting cards. And so they drop out of the Uber economy altogether. Interestingly, rather than switching to cards, many Mexicans who already had cards but often paid for rides with cash used Uber less after the ban as well. The lesson here is that good ol’-fashioned cash is important to people in emerging markets like Mexico. It allows them to make payments they wouldn’t otherwise make.

The ability to pay with cash may be more important to some people than others. By matching Uber’s ride data with demographic information from Mexico’s census, the authors show that lower-income households are more dependent on cash fares. This means that bans have a bigger effect on the poor than other demographic groups.

Alvarez and Argente’s careful approach to measuring the social usefulness of cash should give would-be cash banners in developing nations pause. Sure, Nigeria isn’t quite banning cash. It is increasing the costs of using it. But the basic principles drawn from Alvarez and Argente’s Uber study still apply.

Nigerians, Mexicans, Kenyans, Indians, and others in low-income countries who depend on cash may not be able to smoothly switch into non-cash alternatives. Rather than nudging them to use cards, well-meaning cash bans may lead citizens to reduce their consumption and thus their overall welfare. As for people who already have cards, they may still prefer to use cash in certain situations. A policy that restricts cash usage may lead them to avoid making some transactions rather than swiping, tapping, or inserting their cards to pay.

Nigeria is one of Africa’s most influential nations. But other African countries should think twice before emulating its costly cash policy. As for the Central Bank of Nigeria, it won’t roll out its cash tax until March 2020. It still has a few months to reconsider.

J.P. Koning

J.P. Koning is a financial writer and blogger with interests in monetary economics, economic history, finance, and fintech. He has worked as an equity researcher at a Canadian brokerage firm and a financial writer and publisher at a large Canadian bank. More recently, he has written several papers for R3, a distributed ledger company, on the topics of central bank cryptocurrency and cross border payments. He founded the popular blog Moneyness in 2012. He designs economics and financial wallcharts at Financial Graph & Art.

Koning earned his B.A. in Economics from McGill University.