New Orders for Durable Goods Rose Again in July, but Details Are Mixed

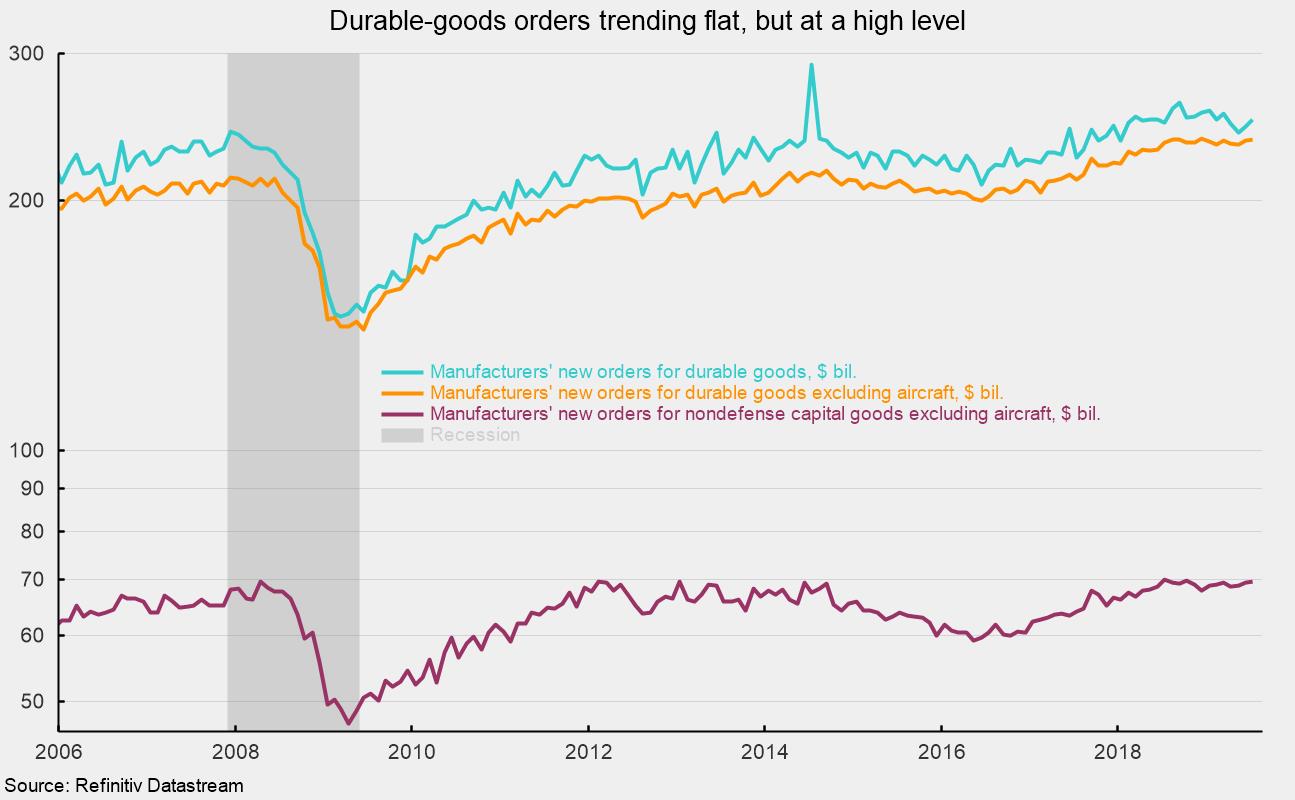

New orders for durable goods jumped 2.1 percent in July following a gain of 1.8 percent in June. The gain in July was supported by large increases in both defense and nondefense aircraft orders. Nondefense aircraft orders gained 47.8 percent in the month while defense aircraft orders jumped 34.4 percent. Because of the large per-unit price and the tendency for buyers to place orders for multiple aircraft at once, both of these series tend to be extremely volatile. If aircraft are excluded, new orders for durable goods rose 0.3 percent for the month of July following a gain of 1.0 percent in June and a decline of 0.3 percent in May. From a year ago, orders for durable goods excluding aircraft are up 0.8 percent. Total durable-goods orders and durable-goods orders excluding aircraft have been essentially flat (near record-high levels) since April 2018 (see chart).

Results for the various categories of orders were mixed in July. Among the industries showing increases, orders for computers and related equipment gained 0.2 percent, electrical equipment and appliances rose 1.1 percent, and motor vehicles gained 0.5 percent. Among the decliners, primary metals were down 1.0 percent, orders for fabricated metal products fell 0.9 percent, machinery orders were off 0.6 percent, and the catchall “other durables” category lost 0.2 percent.

Within the report for new orders for durable goods are data on new orders for capital equipment, or business investment. This subcategory is particularly important for two reasons. First, business investment can have a major impact on future productivity trends, and productivity is critical for helping offset cost increases as well as raising living standards over the long term. Capital-goods orders are also important as they tend to be early indicators of turns in the business cycle. Real new orders for core capital goods — that is, real nondefense capital goods excluding aircraft — is one of the indicators in AIER’s Leading Indicators index.

On a nominal basis, new orders for core capital goods rose 0.4 percent in July following gains of 0.9 percent in June and 0.2 percent in May. Similar to the broader durables-goods category, the trend of new orders for core capital goods has been essentially flat since mid-2018, but near the record high (see chart again).

Overall, the report suggests the manufacturing sector of the economy is expanding at a very slow pace. The strong labor market remains the cornerstone of the economy, supporting consumer spending (about 70 percent of gross domestic product). However, increased uncertainty and anxiety among consumers and businesses, largely a result of erratic, politically motivated policy, has the potential to destroy confidence and precipitate an economic downturn.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.