New- and Existing-Home Sales Are Showing Divergent Paths

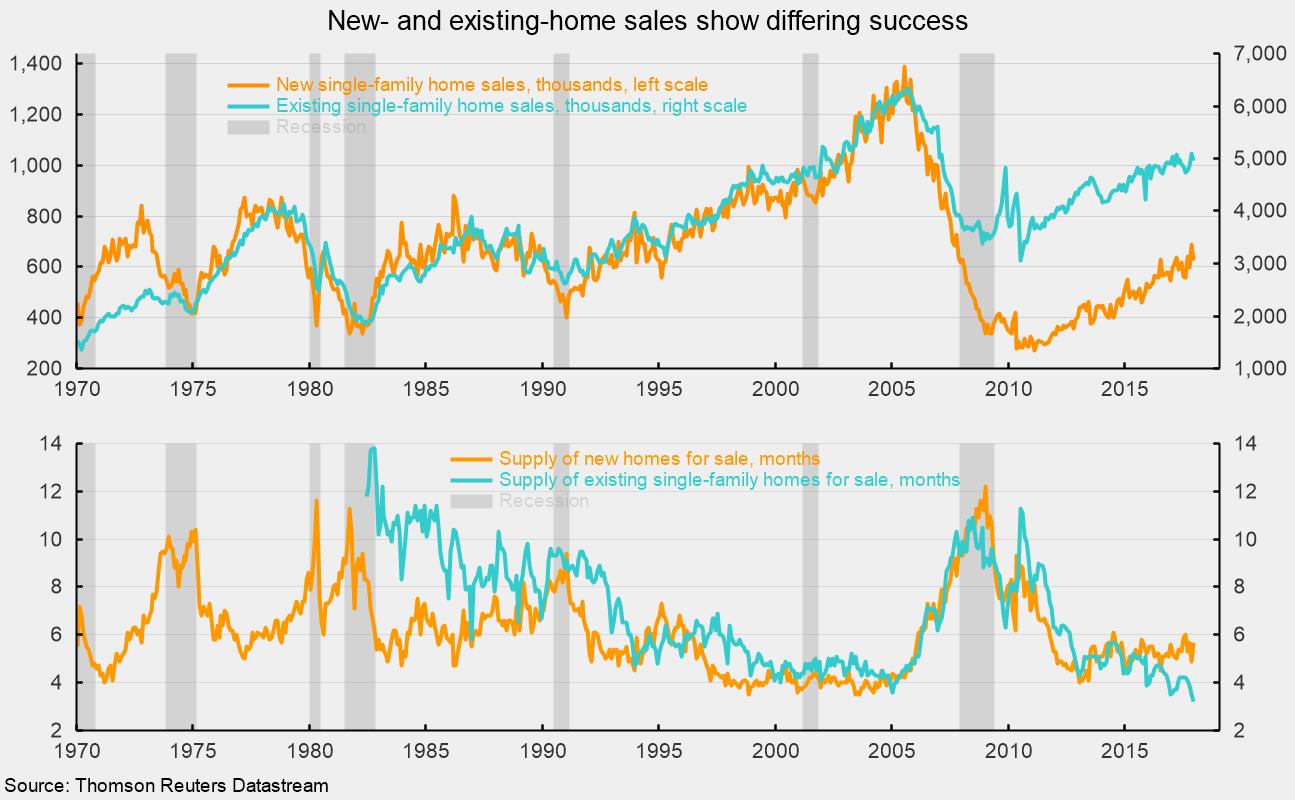

Sales of new and existing single-family homes fell in December, dropping 9.3 percent and 2.6 percent, respectively. While both categories have achieved significant rebounds from their postrecession lows, the degree of success varies substantially between the two.

For new-home sales, the rebound from the February 2011 annualized low of 270,000 units to the December 2017 pace of 625,000 is about 130 percent and places the latest month close to the average of 632,000 average for the period 1970 through 1996, before the housing market started to surge. The current upward trend looks set to continue. The decline from the peak in the mid-2000s to the 2011 low was slightly more than an 80 percent plunge.

For the existing-home market, the decline from the peak in 2005 to the low in 2010 was not as large: about 50 percent. Since the low, existing-home sales have risen about 62 percent, which puts the current pace of 4.96 million well above the 1970–96 average of 2.97 million. However, recently, existing-home sales have been trending flat. The bottom line is that new-home sales fell more sharply and have rebounded only back to the pre-bubble average while existing-home sales fell less and are back at historically strong rates (see top chart).

Furthermore, the stronger recovery in existing-home sales has pushed the current months supply to an all-time low of just 3.2 months while the months supply for single-family homes has held relatively steady in the 5–6 months range (see bottom chart). Tight supplies are likely to support higher prices over time. Higher prices combined with somewhat higher interest rates may weaken future demand and help balance supply and demand.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.