Massive Job Losses Continue but The Pace Slows

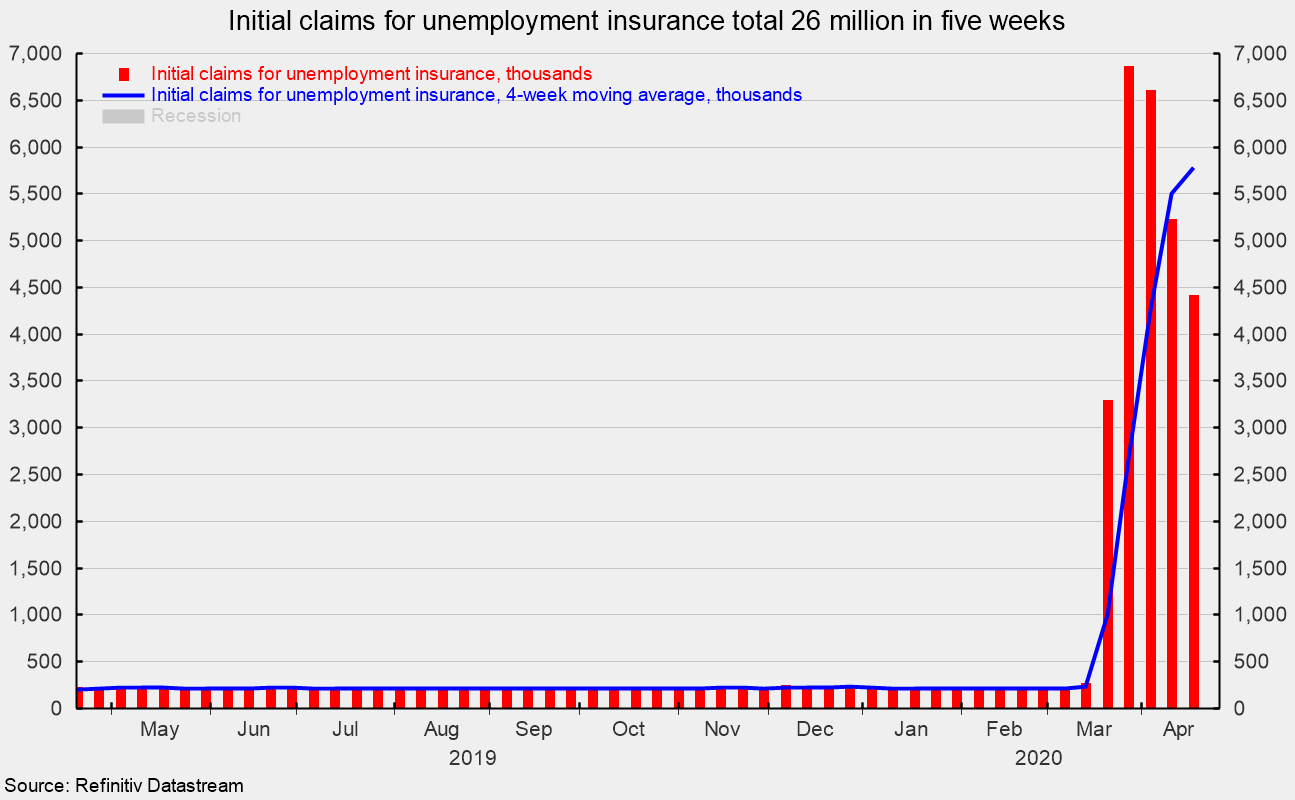

Initial claims for unemployment insurance totaled 4.43 million for the week ending April 18, marking the fifth consecutive week of massive, record-shattering layoffs, and dwarfing the previous high of 695,000 in October 1982. However, on a positive note, the latest tally is the third week of declines in the number of initial claims since the 6.87 million claims during the week of March 27 (see chart).

During the Great Recession in 2008-09, total job losses were 8.8 million over 25 months versus the current 5-week total of 26.5 million initial claims. The unprecedented flood in claims is the leading edge of a tsunami of negative economic statistics that reflect the impact of the COVID-19 outbreak and the drastic policy reactions implemented to contain the spread.

Sales of new single-family homes tumbled 15.4 percent in March to a 627,000 seasonally adjusted annual rate. Sales are now down 9.5 percent from a year ago. Sales fell in all four regions tallied: sales plunged 41.5 percent in the Northeast, putting sales 4.0 percent below year-ago levels while sales plummeted 38.5 percent in the West and were 30.8 percent below the year-ago level. The Midwest region saw an 8.1 percent decline as the South, the largest region by volume, posted a 0.8 percent pullback. From a year ago, sales are down 9.2 percent in the Midwest but up 1.3 percent in the South.

Total inventory of new single-family homes for sale increased 2.8 percent to 333,000 in March, pushing the months’ supply (inventory times 12 divided by the annual selling rate) up to 6.4, up 23.1 percent from February and 10.3 percent above the year-ago level.

Since home buying is often a long process, the sales recorded for March were likely initiated before the worst of the outbreak. It is probable that home sales over coming months may see further sharp declines.

The outbreak of COVID-19 and government policy responses have resulted in massive distortions to economic activity including a sharp rise in layoffs, plunging consumer confidence and retail spending, and declining housing market activity. Expect extraordinarily weak economic reports over the next several months.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.