Job Openings Decline in November

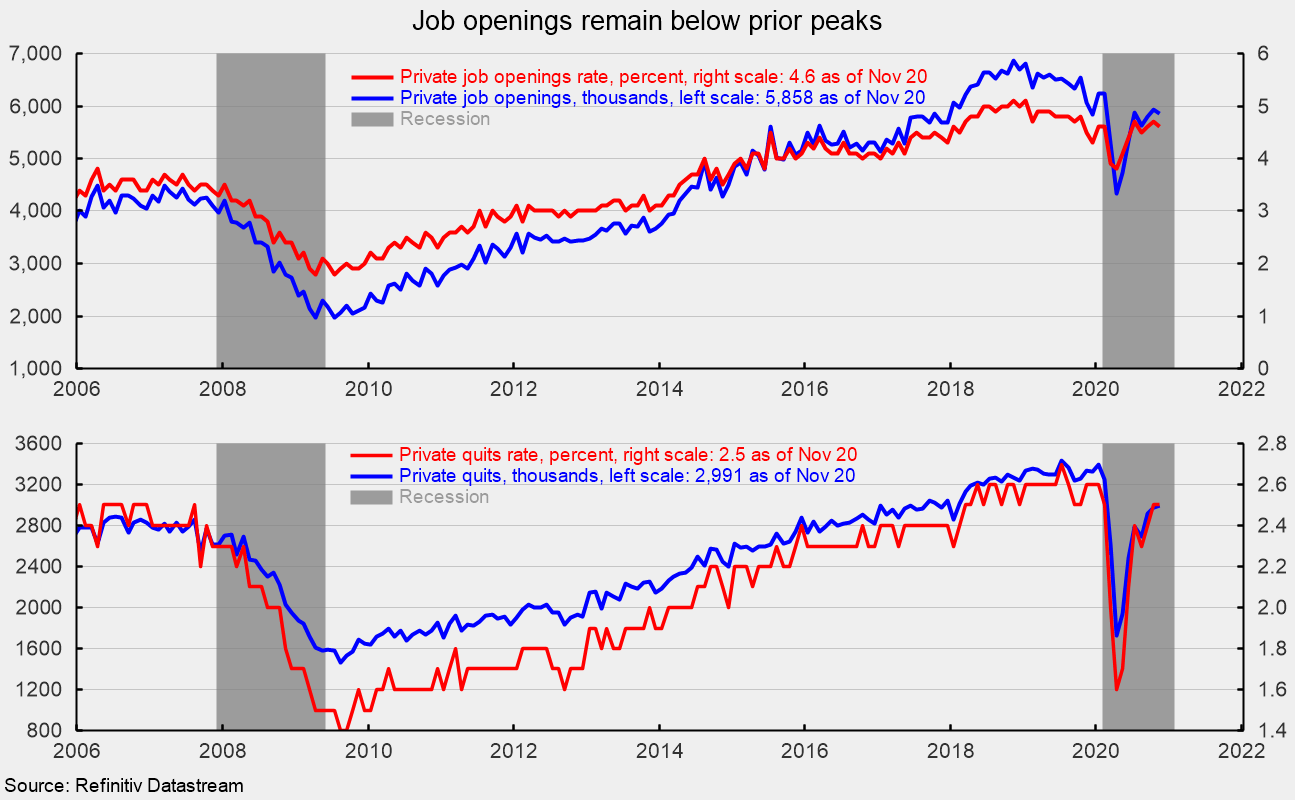

The latest Job Openings and Labor Turnover Survey from the Bureau of Labor Statistics shows the total number of job openings in the economy fell to 6.527 million in November, down from 6.632 million in October. The number of open positions in the private sector dropped to 5.858 million in November (see top of first chart). Private-sector openings are well above the low of 4.332 million in April at the height of government-imposed lockdowns but still below the pre-pandemic peak of 6.858 million in November 2018. The private-sector job-openings rate, openings divided by the sum of jobs and openings, was 4.6 percent, down from 4.7 percent in October but above the low of 3.8 percent in April.

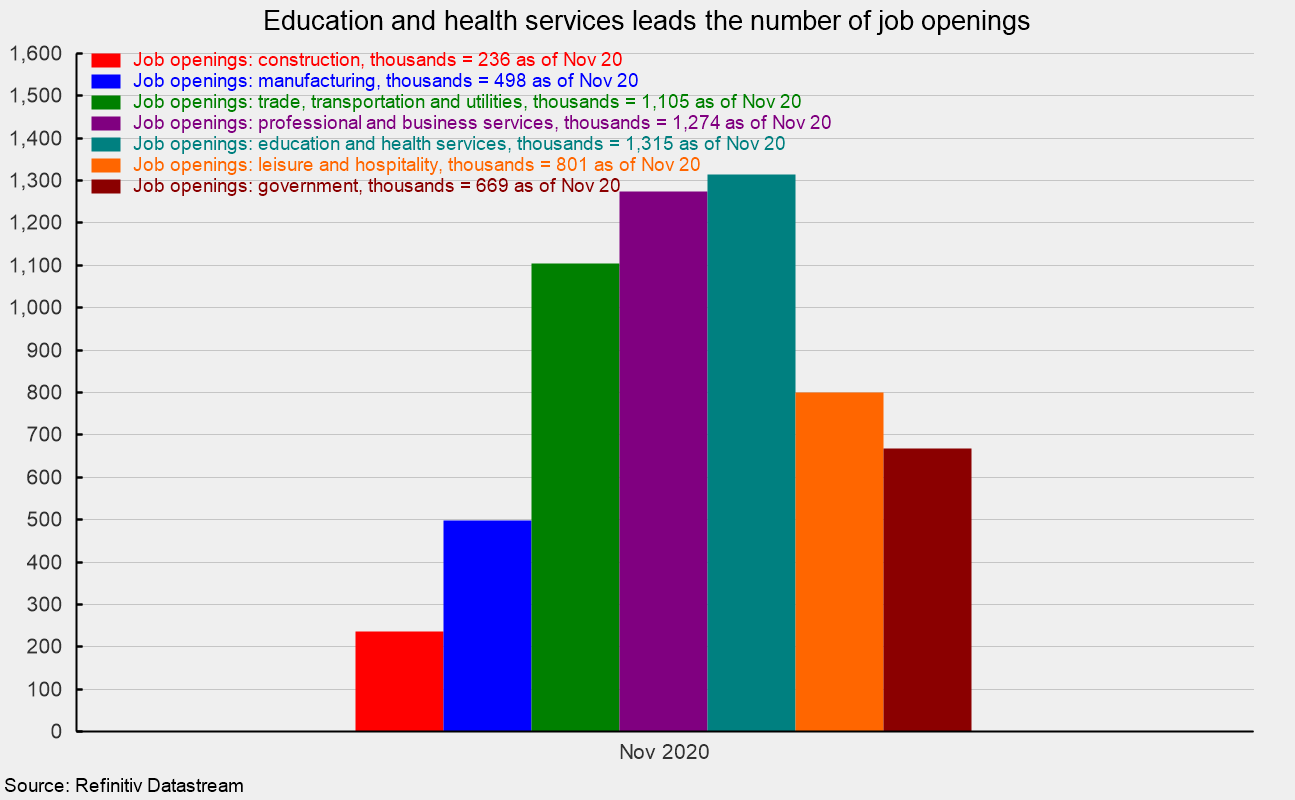

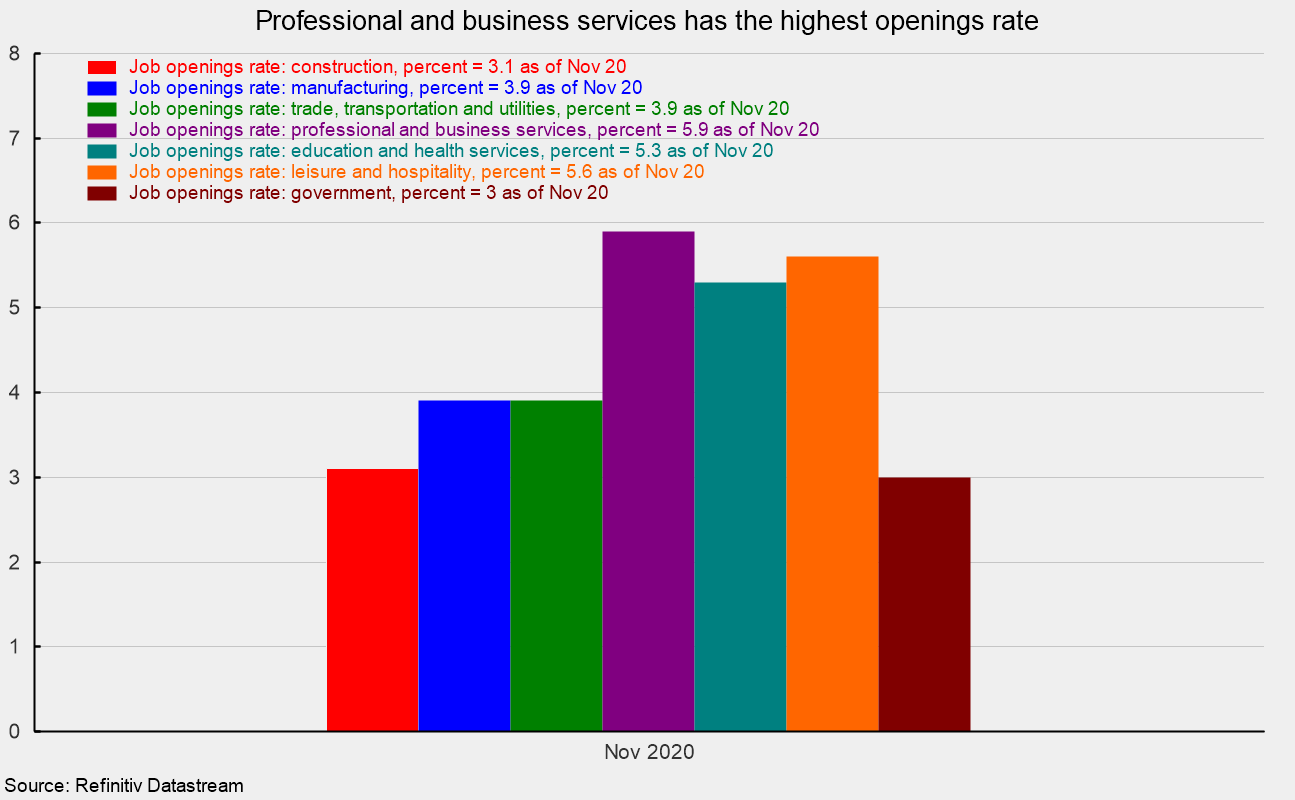

The industries with the largest number of openings were education and health care (1.315 million), professional and business services (1.274 million), and trade, transportation, and utilities (1.105 million; see second chart). The highest openings rates were in professional and business services (5.9 percent), leisure and hospitality (5.6 percent), and education and health care (5.3 percent; see third chart).

The decline in job openings was a function of hires, separations and changing labor requirements. Hires in November rose to 5.979 million from 5.912 million in October. At the same time, the number of separations rose to 5.413 million in November with the number of private sector separations increasing to 5.009 million. Within separations, total quits were 3.156 million (versus 3.150 million in October) and layoffs were 1.971 million, up from 1.676 million in the prior month.

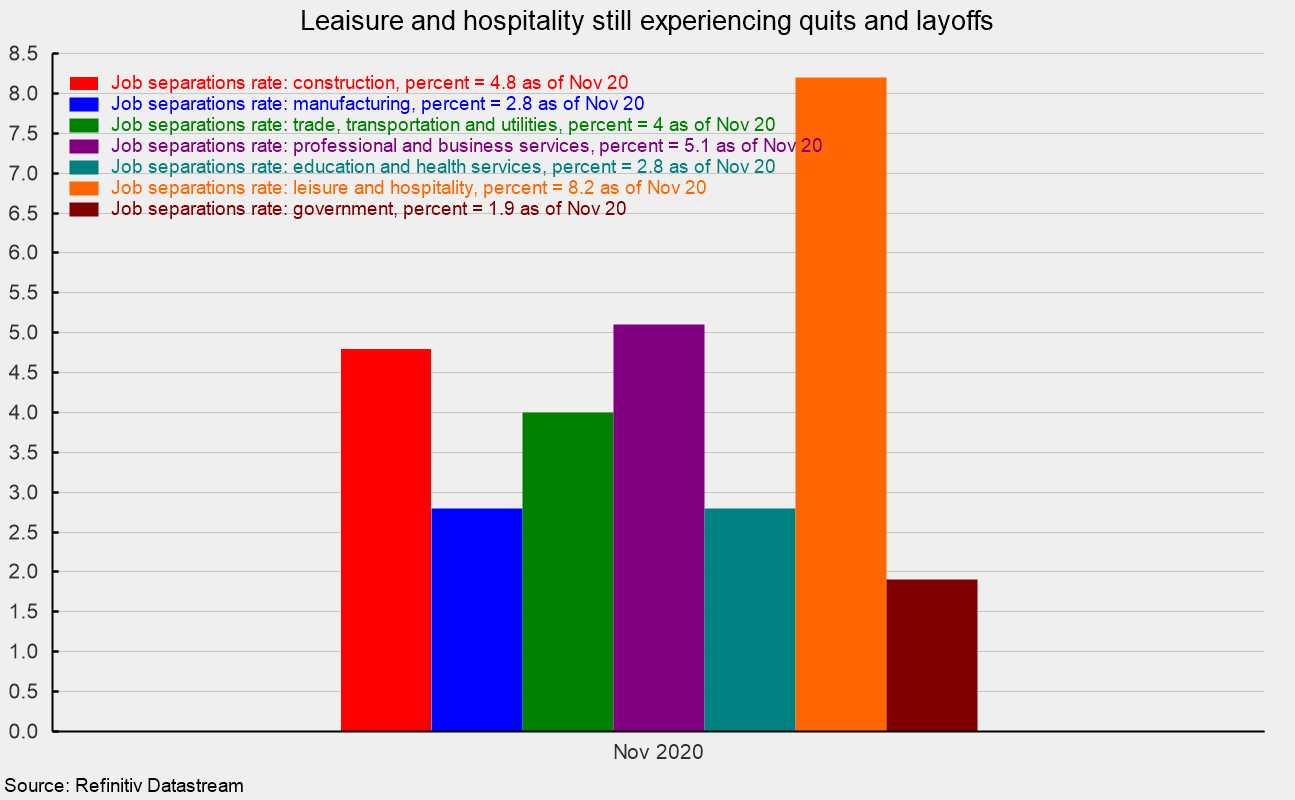

By industry, leisure and hospitality leads with a separations rate of 8.2 percent (layoffs of 439,000 versus 177,000 in October and quits of 631,000 versus 574,000 in the prior month), followed by professional and business services at 5.1 percent and construction at 4.8 percent (see fourth chart).

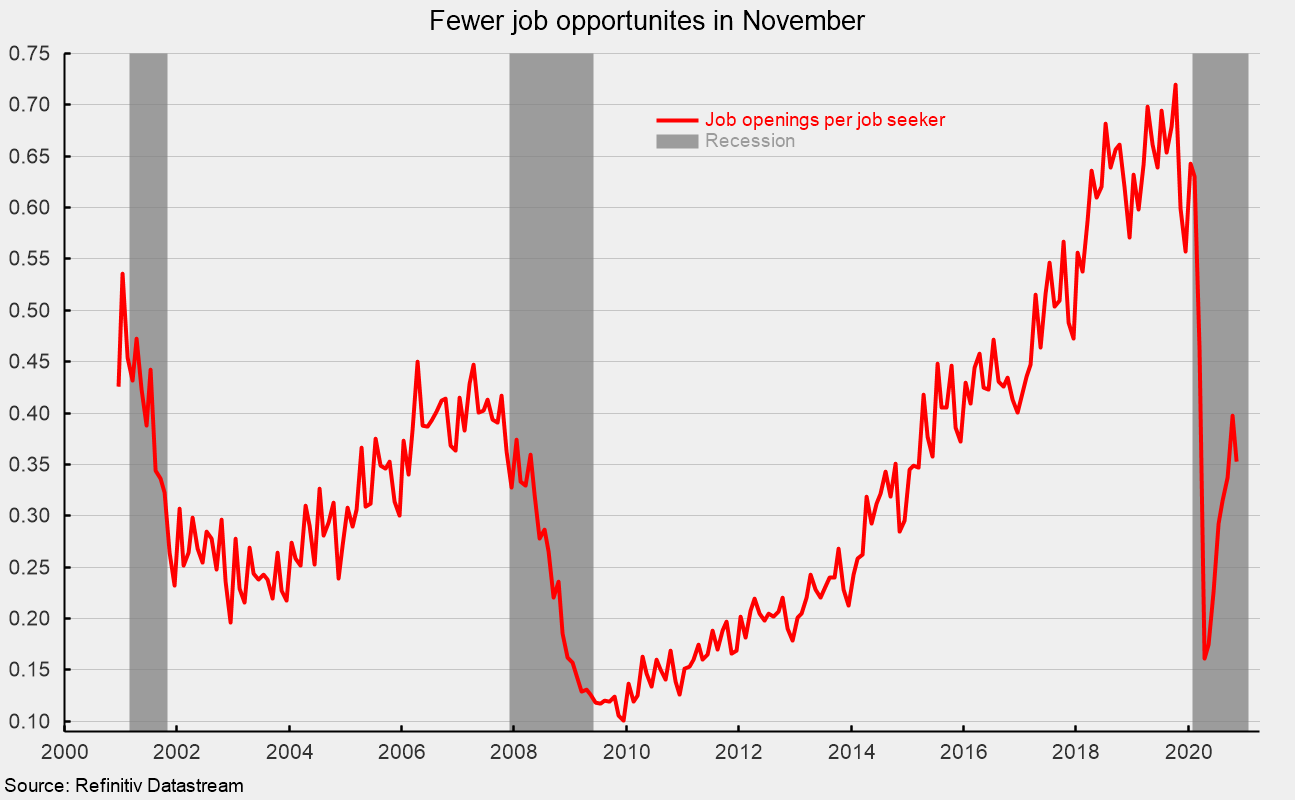

From the worker perspective, labor market conditions remain challenging. The drop in openings and still elevated number of job seekers (unemployed plus those not in the labor force but who want a job) leaves the ratio of openings to seekers at a modest 0.353. That is about in line with the peaks in 2006-2007 but well below the 0.72 openings per seeker in October 2019 (see fifth chart).

Overall, the data relating to the labor market paint a mixed picture of recovery from the massive damage of nationwide lockdowns. The impacts of those lockdowns vary widely among industries. With new restrictions on the rise, the outlook for the economy remains highly uncertain.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.