ISM Manufacturing Survey Stayed Strong in November

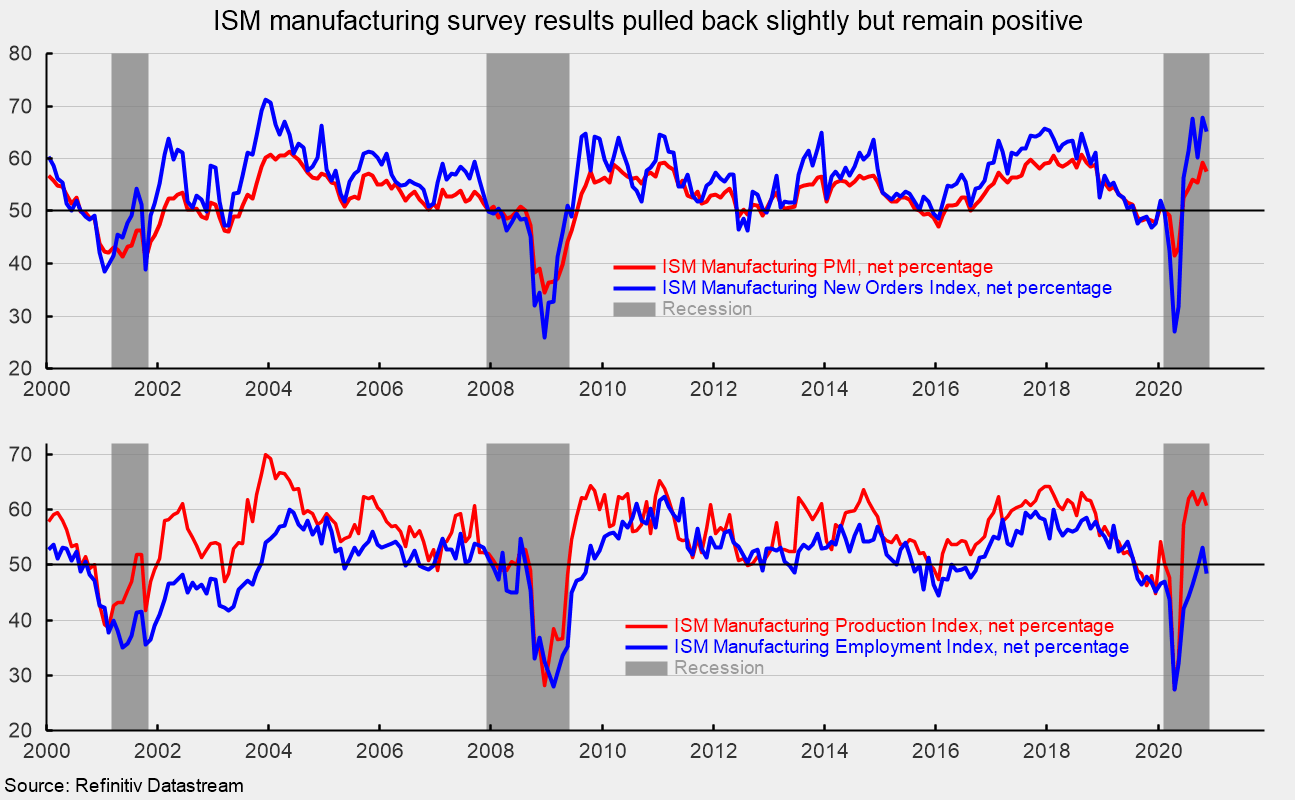

The Institute for Supply Management’s Manufacturing Purchasing Managers’ Index fell slightly in November, posting a 57.5 percent reading for the month, down from 59.3 percent in October. The latest result is the sixth consecutive reading above the neutral 50 threshold (see top of first chart). Over the past six months, the Purchasing Managers’ index has averaged 55.8, the highest since March 2019. Overall, the report notes, “The manufacturing economy continued its recovery in November. Survey Committee members reported that their companies and suppliers continue to operate in reconfigured factories, but absenteeism, short-term shutdowns to sanitize facilities and difficulties in returning and hiring workers are causing strains that will likely limit future manufacturing growth potential. Panel sentiment, however, is optimistic (2.5 positive comments for every cautious comment), an improvement compared to October.”

Among the key components, the New Orders Index came in at 65.1 percent, down from 67.9 percent in October (see top of first chart). The New Orders Index has been above 50 for six consecutive months and above 60 for five consecutive months. The six-month average is 63.1, the highest since June 2018. Fifteen of eighteen industries in the survey reported growth in new orders in November. The New Export Orders Index came in at 57.8 percent in November, up 2.1 percentage points from a 55.7 percent result in October. The Backlog-of-Orders Index came in at 56.9 percent in November, up from 55.7 percent in the prior month and the highest level since August 2018 (see second chart).

The Production Index registered a 60.8 percent result in November, down from 63.0 percent in October. The index has been above 50 for six consecutive months and above 60 for the last five months (see bottom of first chart). The six-month average is 61.3, the highest since October 2018. Fourteen industries reported growth in the latest month.

The Employment Index fell in November, falling 4.8 percentage points to 48.4 percent in November, versus 53.2 percent in October. The October result was the first and only reading above the neutral 50 threshold since July 2019 (see bottom of first chart). The Bureau of Labor Statistics’ Employment Situation report for November is due out on Friday, December 4th. Consensus expectations are for a gain of 495,000 nonfarm-payroll jobs including the addition of 45,000 jobs in manufacturing. The unemployment rate is expected to fall to 6.8 percent from 6.9 percent in October.

The Supplier Deliveries Index, a measure of delivery times from suppliers to manufacturers, rose to 61.7 percent from 60.5 percent in October. Slower supplier deliveries are usually consistent with stronger manufacturing activity. According to the report, “Suppliers continue to struggle to deliver, with deliveries slowing at a faster rate compared to October. Transportation challenges and challenges in supplier labor markets are still constraining production growth, the latter likely to last until Covid-19 is controlled. The Supplier Deliveries Index reflects the difficulties suppliers continue to experience due to Covid-19 impacts. Supplier constraints are not expected to diminish soon, and supplier labor issues appear to be worsening.”

The Prices Index fell slightly to 65.4 percent in November from 65.5 percent in. Seventeen industries paid higher prices for raw materials in November while no industries reported a decline in prices. Higher prices were reported for: apparel, leather and allied products, textile mills, wood products, paper products, fabricated metal products, primary metals, plastics and rubber products, machinery, furniture and related products, electrical equipment, appliances and components, miscellaneous manufacturing, printing and related support activities, food, beverage and tobacco products, transportation equipment, chemical products, nonmetallic mineral products, and computer and electronic products.

Customer inventories in November are still considered too low, with the index remaining below 50 at 36.3 percent versus 36.7 percent in the prior month and the lowest level since June 2010 (index results below 50 indicate customers’ inventories are too low; see second chart). The index has been below 50 for 50 consecutive months. Insufficient inventory may be a positive sign for future production.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.