ISM Manufacturing Purchasing Managers Index Points to Slower Growth in December

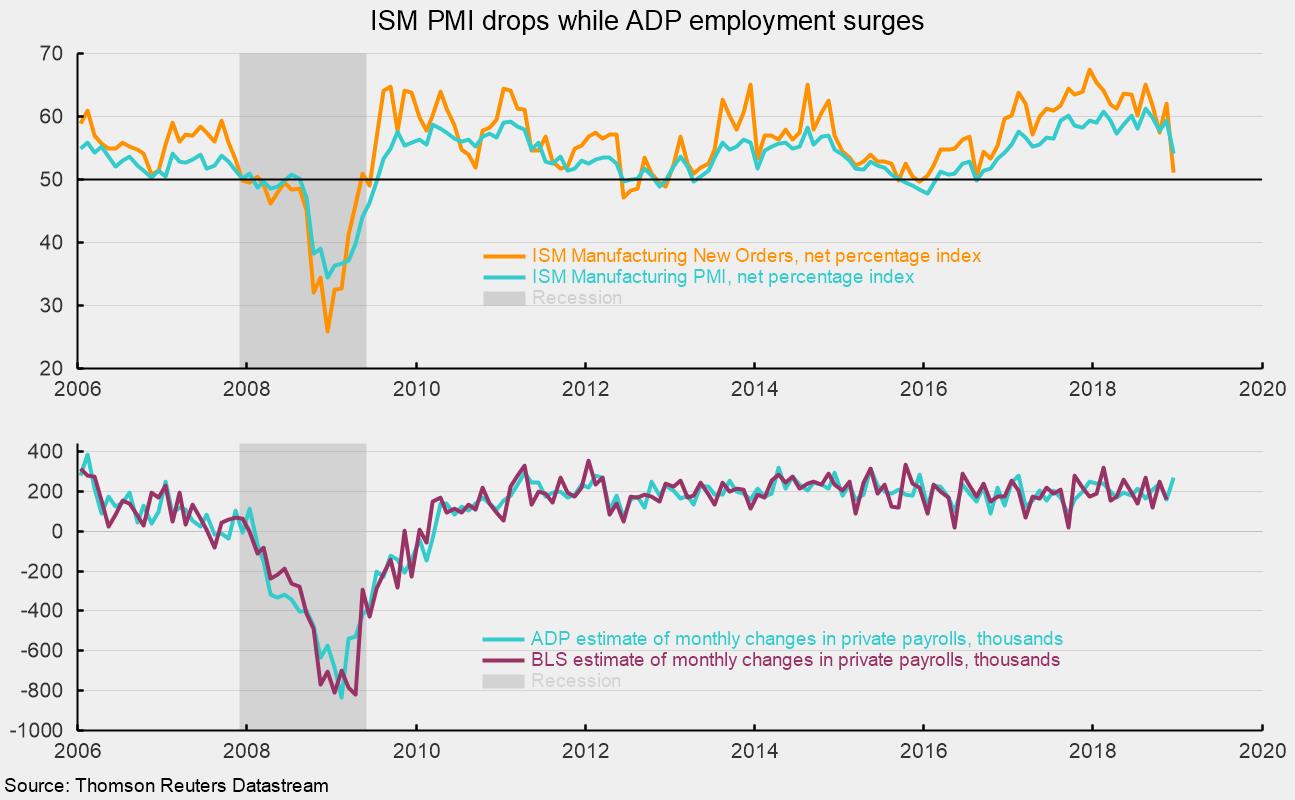

The Manufacturing Purchasing Managers Index from the Institute for Supply Management registered a 54.1 percent reading in December, down 5.2 points from 59.3 in November and the lowest reading since November 2016 (see top chart). December is the 28th month in a row above the neutral 50 level and the 116th above the 43.2 percent threshold consistent with expansion in the overall economy. Comments from purchasing executives highlight international concerns including trade wars and rising tariffs, signs of slowing global growth, and Brexit, along with increased uncertainty regarding the U.S. economy, as significant issues.

Among the key components of the Purchasing Managers Index, the New Orders Index plunged 11.0 points to 51.1, the lowest reading since August 2016. The result was the 36th consecutive month with readings above 50, but the weak reading suggests a significant deceleration in demand (see top chart). New export orders ticked up slightly, adding 0.6 points to 52.8. The backlog of unfilled orders dropped 6.4 points to a neutral reading of 50.0.

The production index was at 54.3 percent in December, down from 60.6 in November. December marks the 28th month in a row above 50. Historically, readings above 51.5 are consistent with growth in the industrial-production index from the Fed. In December, 10 industries surveyed reported growth while 4 reported a decrease in production.

The employment index fell to 56.2 percent in December, down from 58.4 in November. Despite the decline, the result suggests employment in manufacturing likely increased in December. The Bureau of Labor Statistics’ Employment Situation report for December is due out on Friday, January 4. Consensus expectations are for 170,000 new nonfarm-payroll jobs including 20,000 new jobs in manufacturing. Payroll processor ADP released its estimate for private payrolls for December, projecting a very strong 271,000 new employees for the month (see bottom chart). Those data stand in stark contrast to the generally weak results from the ISM.

Supplier deliveries, a measure of delivery times from suppliers to manufacturers, came in at 57.5, down from 62.5 in November. December was the 27th consecutive month above 50, and the results suggest suppliers delivering to manufacturers are still falling behind but at a somewhat slower pace.

The prices index eased again, though it is still above neutral. The index fell 5.8 percentage points to 54.9 in December from 60.7 in November. However, the index had been trending higher since early 2016 and has been above 50 for 34 months. These results suggest manufacturers are experiencing materials-costs pressures though the pressures are less robust. Some inputs may be pressured by both strong demand and higher tariffs.

Customer inventories in December are still considered too low, with the index falling to 41.7 from 41.5 in the prior month (index results below 50 indicate customers’ inventories are too low).

Today’s report from the Institute for Supply Management suggests the manufacturing sector continued to grow in December but the pace decelerated significantly. This report adds support for a cautious outlook.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.