Is the Rydex S&P 500 Fund the Worst Mutual Fund in the World?

It is generally a reasonable approach to invest in passively managed index funds because research has shown that actively managed funds have not shown a consistent ability to beat their indexes.

Index funds simply buy and sell the stocks that comprise an index, such as the S&P 500. With such a simple approach, they are generally able to operate at a low cost while avoiding risks that result from concentrating too heavily in a small group of securities. This is good, because if you can operate at a lower cost, you can generally pass along more of the investment gains to investors.

As an example of these low costs, Vanguard’s 500 Index Fund charges anywhere from 0.05-0.16 percent depending on the share class, and the Fidelity S&P 500 Index fund now advertises fees as low as 0.045 percent.

The Vanguard 500 Index Fund (VFIAX), which charges 0.05 percent per year, has performed almost exactly as expected. In the last five years, The S&P 500 benchmark has returned 12.55 percent, while the Vanguard 500 Index Fund has returned 12.51 percent per year – almost exactly the benchmark minus expenses.

However, just because a mutual fund tracks an index doesn’t mean that it has super-low fees. Allow me to introduce what just might be the worst mutual fund in the world, the Rydex S&P 500 Fund – Class C (RYSYX).

The Rydex fund tracks the S&P 500, just like hundreds of other index funds, but charges more than 2 percent more per year. The Rydex fund charges 2.31 percent for its seemingly simple task of buying and selling stocks based on what the Index tells them. This fund, not surprisingly, has performed nearly exactly as expected as well: it has earned the benchmark return minus expenses. The 5-year return for the Rydex fund has been 9.88 percent, about 2.67 percent below the benchmark.

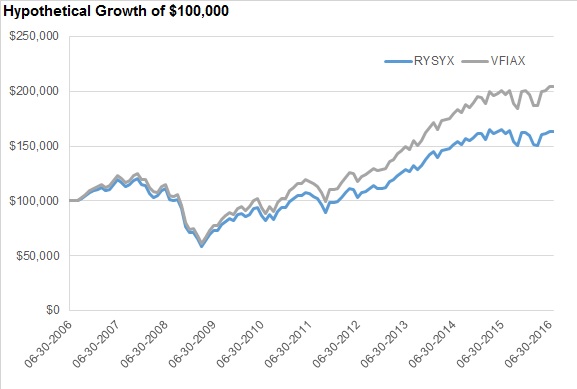

To put some dollar figures on this, an investor who bought $100,000 worth of the Rydex fund in June 2006 (when data are first available), would have about $163,619 today. Another investor who bought $100,000 worth of the low-cost Vanguard option would have $204,758, an extra $41,139. That is a travesty for Rydex investors.

Source: Morningstar advisor tools.

I should note that these returns are actually quite good given the recent past, but only because the S&P 500 Index itself has outperformed many other asset classes. However, using a fund such as this one essentially “locks in” a return that will be more than 2 percent below the benchmark.

The charges on this Class C fund include a 0.75 percent management fee (highway robbery), a 1.00 percent 12b-1 fee (the marketing or distribution fee which compensates advisors for selling the fund), and a deferred sales load of 1.00 percent (another bonus for the seller that may or may not be collected based on how long you hold the fund).

Why would anyone buy such a fund when funds from Vanguard, Fidelity or others, which seek to match the same index, are available with total costs roughly 97 percent less?

According to Morningstar, this fund has about $228 million in assets under management. With a net expense of 2.31 percent, people affiliated with selling and managing this fund collect more than $5 million per year. This fund is not the only one of its kind. According to one source, there are more than $23 billion invested in S&P 500 Index funds with expense ratios of at least 0.50 percent.

There are times when Index fund fees will likely be higher than 0.05 percent. For example, if you want exposure to international or emerging market stocks, you may find the lowest cost funds charge as much as 0.25-0.50 percent. But there is no excuse for investors continuing to pay fees of greater than 1 percent for funds if an alternative is readily available at a lower cost.

The trouble with these funds is that they may be all that you’re offered as an investor. Maybe you’ve got an advisor that stands to benefit from selling the funds, and this is all he or she offers. Or maybe you’ve got a 401(k) plan that only offers one choice of S&P 500 Index fund. Whatever the case, I urge people to explore alternative options so that we can put these funds out of their misery.

Click here to sign up for the Daily Economy weekly digest!

American Investment Services, Inc. (AIS) is an S.E.C. Registered Investment Adviser founded in 1978. AIS is wholly-owned by the non-profit scientific and educational organization American Institute for Economic Research.

Past performance may not be indicative of future results. Therefore, no current or prospective investor should assume that the future performance of any specific investment, investment strategy or product made reference to directly or indirectly, will be profitable or equal to past performance levels. Indexes are not available for direct investment. Historical performance results for investment indexes and/or categories generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing historical performance results. The results portrayed in this portfolio reflect the reinvestment of dividends and capital gains. Returns depicted are hypothetical and do not constitute recommendations.

Luke F. Delorme

Luke F. Delorme is Director of Financial Planning for American Investment Services. Articles do not constitute personal investment advice. Please seek the advice of a professional before implementing any financial decision. Luke can be reached at LukeD@americaninvestment.com.