Is Big Oil Really Manipulating Market Prices?

A recent study by the California Energy Commission, as reported by the Los Angeles Times, has suggested the state’s high gas prices may be the result of “market manipulation” on the part of Big Oil. The memo passed along to Governor Gavin Newsom also suggested other factors such as refinery outages and environmental regulations, but it was the term “market manipulation” that was plastered across the headlines, most likely designed to fuel customer anger at private market suppliers.

But the logic that “market manipulation” by oligopolistic producers is to blame, even in part, for high prices fails to hold up to a few simple questions: If Big Oil is so powerful as to raise California gas prices to such exorbitant levels, why don’t they do this on a consistent basis? Why not raise the price of gasoline to its highest-water mark over the past five years and leave it there? Why should gasoline prices ever fall?

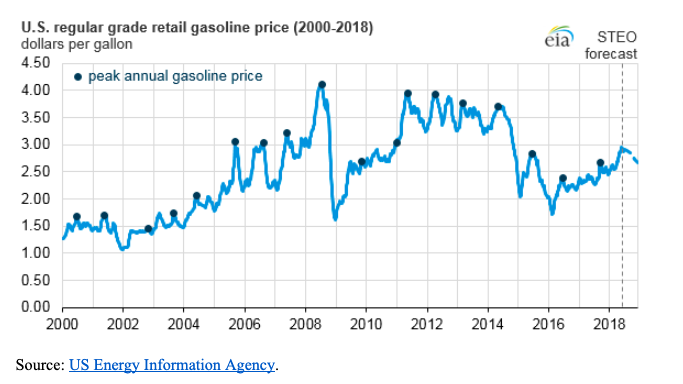

When you consider all of the “generic, processed commodities” you purchase on a regular basis – from bread to coffee and from beer to petrol – gas prices exhibit the greatest volatility. The USEIA chart below clearly shows the wild swings in prices of gas. While data on bread or Starbucks coffee are not as easily available, a casual consideration of your own consumer habits probably reveals that such radical swings are rare for those (and other) common items.

If Big Oil, an industry that is certainly less competitive than coffee or bread, is so powerful, shouldn’t it be able to set prices at a consistently high level? Their market power should be more enhanced by the inelastic nature of gasoline relative to bread or coffee. If coffee prices steam upwards, people can switch to tea or soda for their caffeine fix; if the price of bread rises, a keto diet is always a possibility.

One possible explanation is that the producer market for these other commodities is so competitive that prices have been whittled down to their lowest sustainable level and thus cannot exhibit wild swings. Fair enough, but that doesn’t explain why an industry with a small handful of firms can’t collude to set prices. Indeed, mainstream economic theory seems to suggest that market concentration comes with price-setting power, either explicitly via backroom collusion or implicitly by merely observing the prices of your relatively few competitors.

Gas stations might even make such implicit collusion easy by advertising their prices in glaring bright signs on the roadside. It is as if they are saying to one another: “Hey buddy, we’re selling at $4.10 a gallon. If you do the same, we’ll both make a killing.”

Alas, the highly-visible signage of gas prices presents another problem for the price fixing theory of petrol. If you were intent on “market manipulation,” why advertise it so clearly? Gas is one of the most inelastic products we buy, so why not simply have a sign that reads “Buy Gas Here: Nothing You Can Do About It Sucker!”

Market manipulation would be so much easier if you didn’t declare what your price is relative to the station down the street. And yet, of all the things we buy on a regular basis, the price at the pump is the most visible.

If oil executives were really in the business of manipulating market prices, they are going about it in the most incompetent manner possible.

The goal here is not to explain why gas prices are so high today. There are numerous factors at play, including excise taxes which go up but rarely ever down. (Indeed, if there was ever a case to be made for monopolistic market manipulation, the good folks in the California legislature would do well by looking in a mirror.) Rather, the purpose of this simple exercise is to show how a few common sense, economic questions can help undermine conspiratorial theories of “market manipulation” that unfortunately shape public policy.

The next time somebody complains that Big Oil is manipulating the market, it might be worthwhile to ask them to explain why gas prices would ever fall?

As any good economist will tell you, asking the right question is often more important than finding an answer.

Anthony Gill

Anthony Gill is a professor of political economy at the University of Washington and a Distinguished Senior Fellow with Baylor University’s Institute for the Study of Religion.

Earning his PhD in political science at UCLA in 1994, Prof. Gill specializes in the economic study of religion and civil society.

He received the UW’s Distinguished Teaching Award in 1999 and is also a member of the Mont Pelerin Society.