Initial Unemployment Claims Continue to Fall

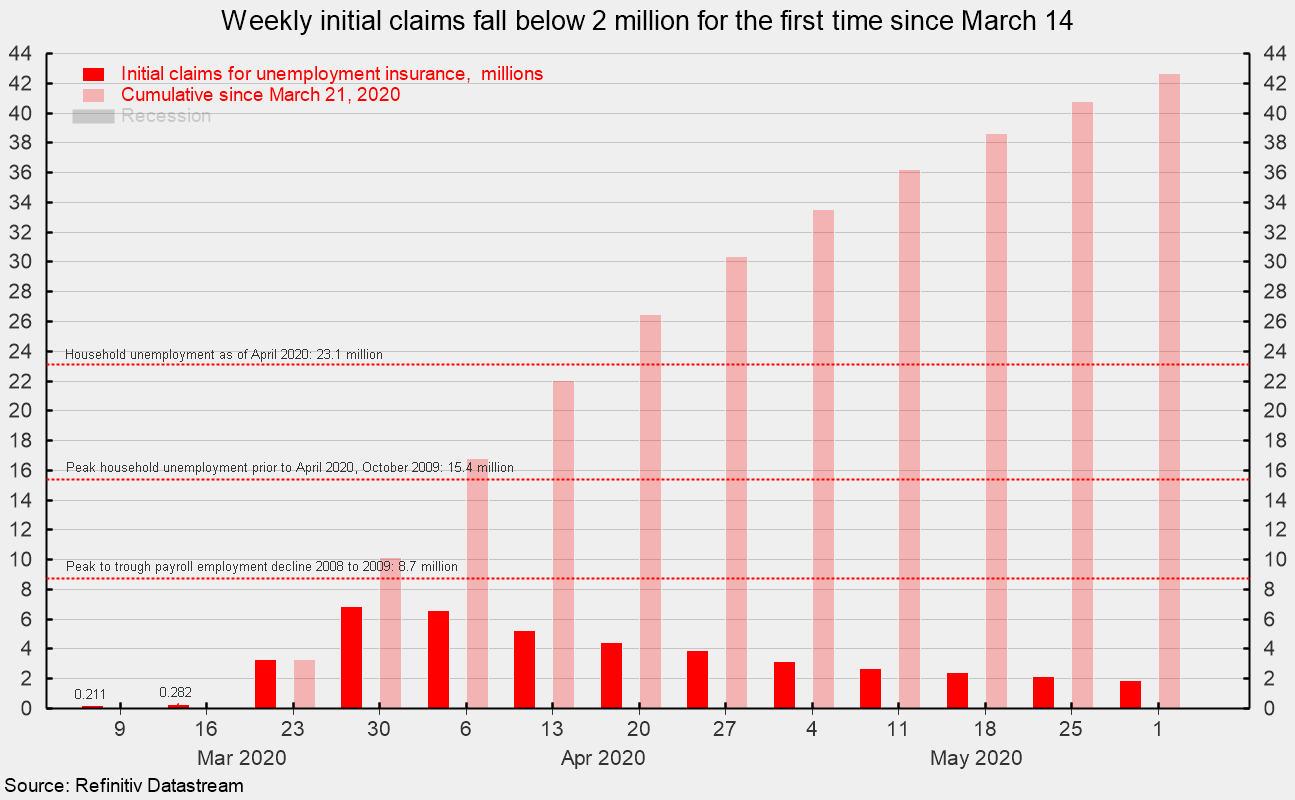

Initial claims for unemployment insurance totaled 1.88 million for the week ending May 30, marking the eleventh consecutive week of massive layoffs (see chart). However, claims have slowed for the ninth straight week after registering 6.87 million for the week ending March 28.

The current 11-week total of 42.65 million initial claims is almost 5 times the total 8.7 million job losses that occurred over 25 months versus during the Great Recession (see chart). The current total is also two and three-quarters times the 15.4 million peak number of unemployed people for the Great Recession, as measured in the household survey portion of the monthly Employment Situation report (see chart).

The national Employment Situation report for April was released on Friday, May 8 and showed a drop of 20.5 million in nonfarm jobs while the unemployment rate surged to 14.7 percent (though the Bureau of Labor Statistics noted that improper responses likely underreported the rate and is likely about 5 points higher, near 20 percent); total unemployed in April was 23.1 million. The previous cycle peak in the unemployment rate was 10 percent in October 2009 while the highest unemployment rate since 1950 came in November 1982 at 10.7 percent. Though data collection was much less reliable, the unemployment rate following the Great Depression was estimated to have peaked at about 25 percent in 1933.

The employment report for May is due out on Friday June 5. Consensus is for a loss of 8 million nonfarm jobs, with 7.5 million coming from the private sector. The unemployment rate is expected to be 19.8 percent. Those numbers are significantly more pessimistic than the 2.8 million private-sector job loss estimated by payroll processor ADP. Massive layoffs as a result of government shutdown policies have occurred over the last eleven weeks, crushing the labor market, consumer confidence, and retail spending, sending the economy into recession. Despite massive government spending and extraordinary monetary policy efforts, the outbreak of COVID-19 and ensuing policy responses brought the longest economic expansion in U.S. history screeching to a sudden end. However, as government restrictions are eased, there are early signs of healing starting to emerge, suggesting the economy may be bottoming and setting the stage for growth later in the year.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.