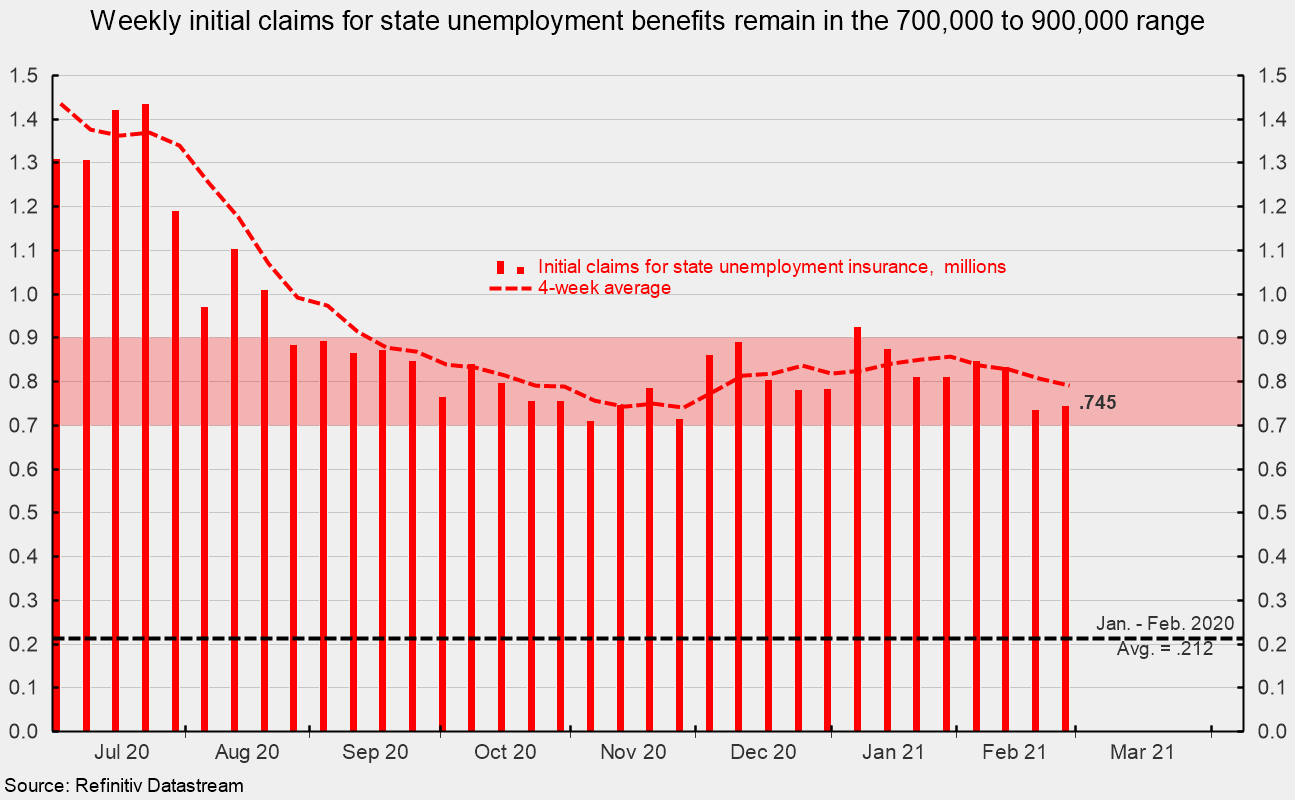

Initial Claims Remain Range Bound

Initial claims for regular state unemployment insurance totaled 745,000 for the week ending February 27, up 9,000 from the previous week’s upwardly revised tally of 736,000 (see first chart). The latest week is the second in a row below 800,000 and follows a run of six consecutive weeks above the 800,000 level. However, over the last six months, initial claims have been bouncing around in the 700,000 to 900,000 range and remain well above the pre-pandemic level of 212,000 in early 2020 (see first chart).

The four-week average fell 16,750 to 790,750, the fourth weekly decline in a row and the first week below 800,000 since early December. However, the four-week average has been in the 700,000 to 900,000 for 27 consecutive weeks. Persistent initial claims at such a historically high level remain a headwind for the labor market recovery and the economy.

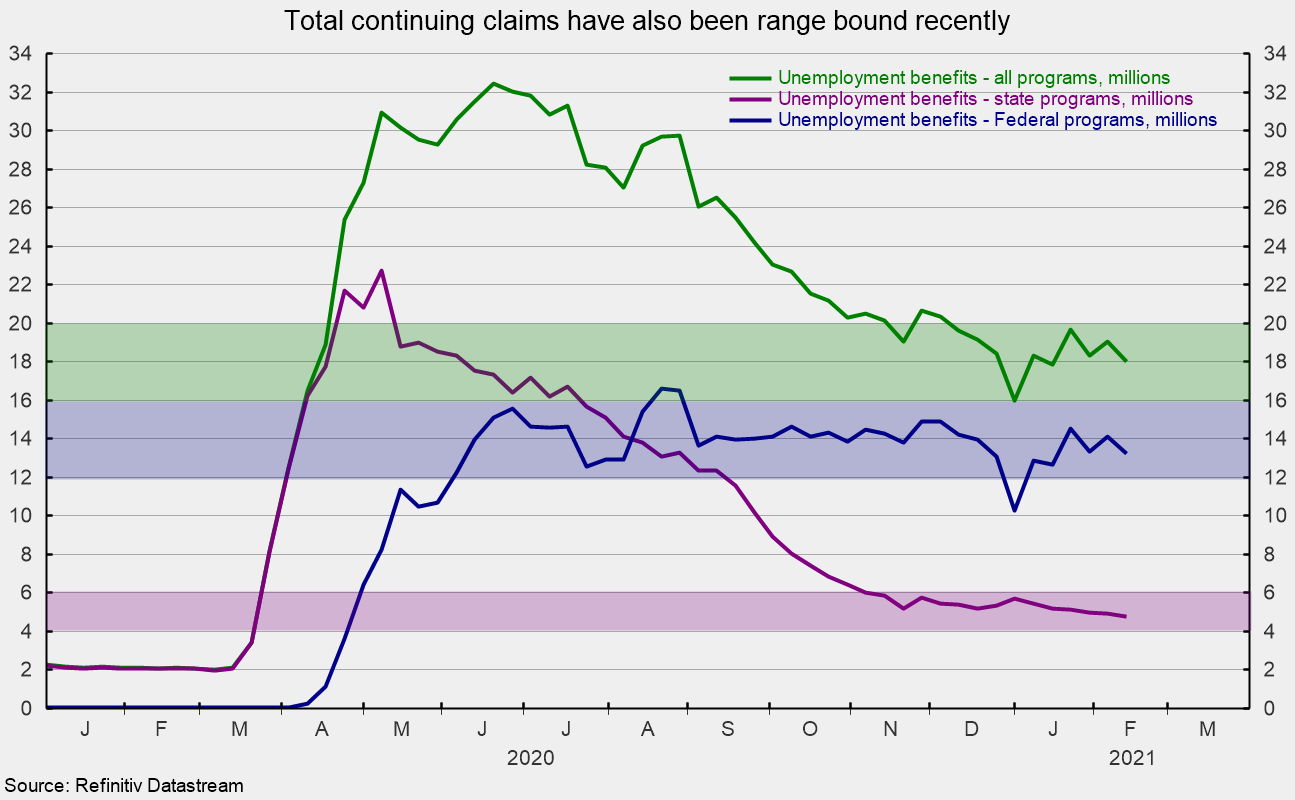

The number of ongoing claims for state unemployment programs totaled 4.794 million for the week ending February 13, down 140,129 from the prior week and the lowest level since March 21, 2020. State programs had been trending lower since early May, but the downward trend has turned to a flattish-to-slightly-lower trend since November, decreasing by an average of just 34,970 per week over the past 12 weeks (see second chart). For the same week in 2019, ongoing claims were 2.058 million.

Continuing claims in all federal programs ticked down in the latest week, coming in at 13.232 million for the week ending February 13 (see second chart). Since the beginning of June 2020, continuing claims in all Federal programs have been in the 12 to 14 million range, averaging 14.029 million.

The total number of people claiming benefits in all unemployment programs including all emergency programs was 18.027 million for the week ended February 13, down 1.019 million from the prior week. Total claims have been in the 16 to 20 million range since November (see second chart).

Government restrictions on consumers and businesses continue to distort economic activity and remain a significant threat to the outlook for economic growth. The distribution of vaccines is a very positive factor and should eventually lead to sharply less government restrictions. In the meantime, the claims data combined with the disappointing jobs report for January suggest the labor market remains fragile. The longer the virus continues to spread (along with the possibility of variants prolonging the outbreak), consumers remain restricted, and businesses remain closed or limited, the more uncertain a labor market recovery becomes and the higher the probability of a slow and drawn-out economic recovery.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.