Initial Claims Jump and Manufacturing New Orders Fall

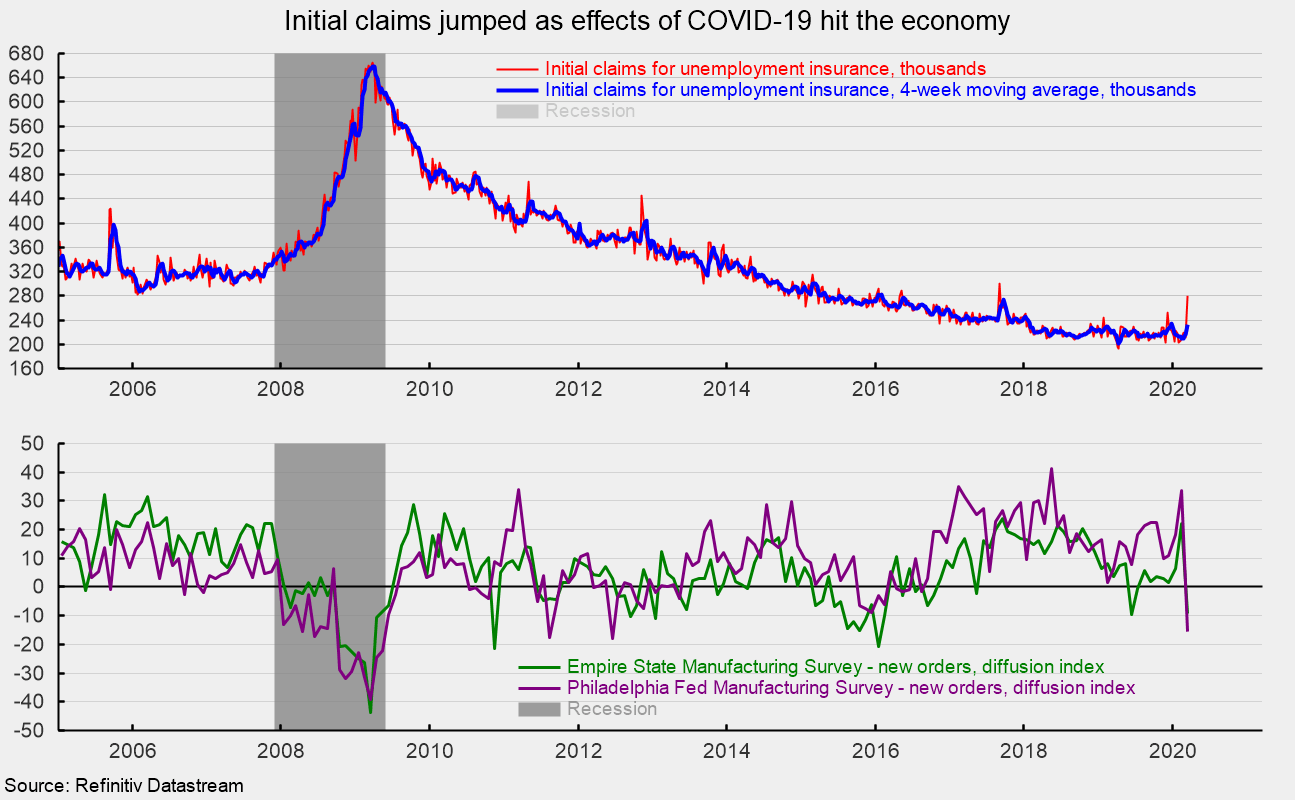

Weekly initial claims for unemployment insurance jumped sharply for the week ending March 14, rising 70,000 to 281,000, the highest level since September 2017. The four-week average came in at 232,250 versus 215,750 in the prior week (see top chart).

According to the Employment and Training Administration within the Department of Labor, “During the week ending March 14, the increase in initial claims are clearly attributable to impacts from the COVID-19 virus. A number of states specifically cited COVID-19 related layoffs, while many states reported increased layoffs in service-related industries broadly and in the accommodation and food services industries specifically, as well as in the transportation and warehousing industry, whether COVID-19 was identified directly or not.”

The results of the Philadelphia Fed’s Manufacturing Business Outlook Survey were generally in line with the New York Fed’s Empire State Manufacturing Survey as both suggest a sharp deterioration in manufacturing conditions in their local regions.

Among the Philadelphia Fed survey’s current-conditions indexes, the general business activity index dropped to -12.7 from 36.7 while the new orders index fell to -15.5 from 33.6 (see bottom chart). The shipments index, number-of-employees index, average-workweek index, unfilled orders index, delivery times index and prices indexes all posted sharp declines.

Among the forward-looking indicators, most indexes posted declines for the month but remained above the neutral zero threshold. The future general-business-conditions index fell to 35.2 in March from 45.4 in February. The future new-orders index fell to 36.7 versus 54.0 in the prior month. Most other forward-looking indexes were lower with the exceptions of the delivery-time index, the inventories index and the number of employees index.

Those results generally confirm the results of The Empire State Manufacturing Survey from the New York Federal Reserve. That survey shows general business conditions deteriorated sharply in March with the index posting a record 34.4-point drop to a -21.5 percent reading versus 12.9 in February. That is the lowest result since 2009. The New Orders Index sank 31.4 points to -9.3, the largest drop since a 31.8-point fall in November 2010 (see bottom chart). The shipments index was -1.7 percent in March, down from 18.9 in February and the lowest level since 2016.

The number of employees index fell to -1.5 percent in March, down from 6.6 in February while the average workweek index fell to -10.6 from -1.0. The delivery time index came in at 2.2, down from 8.3 in February and the unfilled orders index fell to 1.4 from 4.5 in the prior month.

The prices paid index was roughly unchanged, coming in at 24.5 versus 25.0 in the prior month but the prices received index dropped to 10.1 from 16.7 in February.

Among the forward-looking indexes, the general business conditions index fell to 1.2 from 22.9, hitting the lowest level since February 2009 during the last recession. Expectations for new orders also fell, with the index losing 9.9 points to 17.6 from 27.5 in February. The March result is the lowest since January 2016.

The indexes for future shipments, delivery times, prices paid, prices received, number of employees, average employee workweek, capital expenditures, and technology spending all had declines in March. The indexes for future unfilled orders was roughly unchanged while the index for future inventories rose 14.1 points to 5.8.

Today’s reports provide clear evidence of the effects of the outbreak of COVID-19. The widespread disruptions to economic activity are certainly going to cause a drop in aggregate output. Whether the decline is ultimately classified as a recession is not as clear. If the outbreak is contained relatively quickly, there is reasonable expectation for a quick recovery in economic activity.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.