Industrial Production Jumped in October but the Trend Remains Weak

Industrial production jumped 1.1 percent in November, following a 0.9 percent decline in October. That is just the second increase in the past 6 months. Over the past year, industrial production is still down 0.8 percent. Total capacity utilization increased 0.7 percentage points to 77.3 percent as capacity posted a 0.2 percent gain for the month.

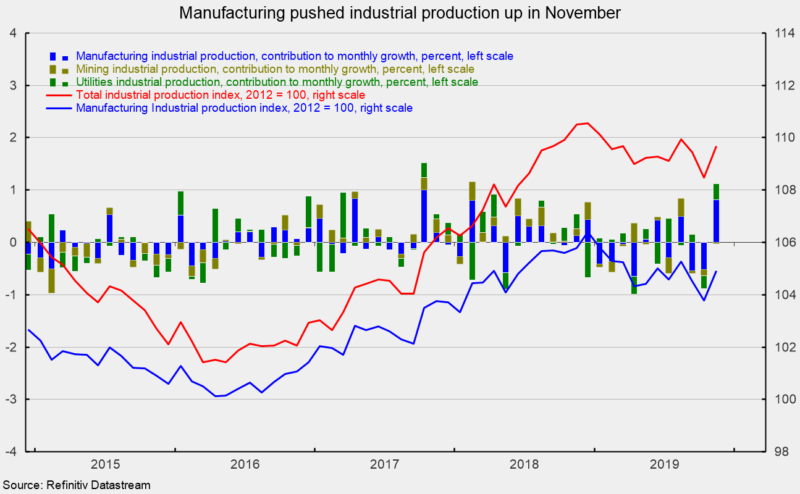

The gain in industrial production was broad-based. The manufacturing sector, which accounts for about 75 percent of total industrial production, rose 1.1 percent for the latest month, the third monthly gain in the past 6 months (see chart). However, over the past year, manufacturing output has fallen 0.8 percent (see chart). It’s too early to know whether the strong gain in November is the beginning of a better trend or just month-to-month volatility. Improved trade conditions and stronger global growth would be positive developments for manufacturing output growth.

Utilities output also posted a strong gain for the month, rising 2.9 percent, while mining output fell 0.2 percent in November. Weather is often a driver of month-to-month changes in utility output while mining is closely related to conditions in the energy commodity markets. Over the past year, mining output is up 2.0 percent while utilities output is down 4.1 percent.

Within manufacturing, durable-goods production rose 2.2 percent while nondurable-goods production moved up by 0.1 percent. Leading the durable-goods production were motor vehicle production (up 12.4 percent and likely related to the resumption of production at GM following a strike by employees), primary metal products (up 2.9 percent), and computer and electronics products (up 1.4 percent). Among nondurable-goods producers, plastics and rubber products rose 1.1 percent while food-products production gained 0.8 percent. On the downside, apparel and leather product output fell 1.6 percent while petroleum and coal products fell 1.2 percent.

Measured by market segment, consumer-goods production jumped 2.1 percent in November, with consumer durables up 6.4 percent and consumer nondurables up 0.9 percent. Business equipment rose 1.7 percent in November but is down 1.7 percent from a year ago. The monthly gain was boosted by a 6.4 percent gain in transit equipment. Construction supplies increased 0.2 percent for the month and is up 0.8 percent over the past year, suggesting a mildly positive outlook.

Materials production (about 46 percent of output) rose 0.7 percent for the month but is off 0.6 percent from a year ago. The non-energy component rose 0.6 percent for the month but is down 2.1 percent from a year ago, with most categories showing declines from a year ago.

Manufacturing capacity utilization rose to 75.2 percent in November, up 0.7 percent from 74.5 percent in October. The November result is right in line with the average of 75.2 since 2012.

Today’s report from the Federal Reserve could be the end of the downward trend in place since December 2108 but it’s too early to be sure. The manufacturing sector is exposed to global trade conditions, both global growth rates and trade policies. The sector may see better performances in the months ahead if global growth reaccelerates and trade policies become more favorable.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.