Humans Aren’t Wired For Investing

Economists are frustrated by investors. Investors will just not follow their models. You see, there is a tendency among investors to sell stocks after a big drop in price, at exactly the time when the expected return has increased. On the flip side, there is a tendency to buy just after prices have risen, when expected returns are lower.

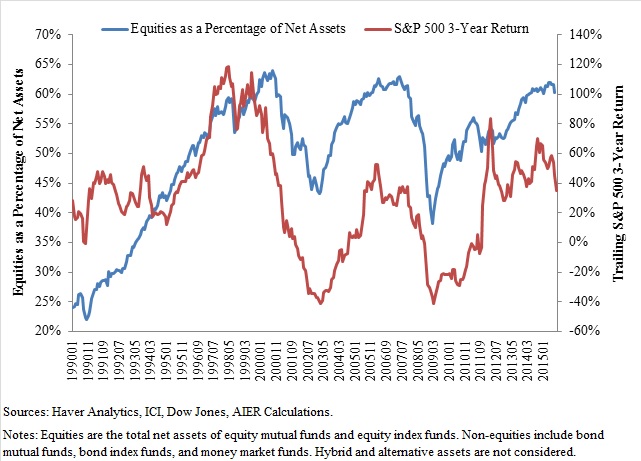

In the late 1990’s, Alan Greenspan famously used the term “irrational exuberance” to describe the dot-com bubble. Investors tend to increase stock holdings after such periods of good stock performance, and decrease them after periods of poor performance (see chart below). This does not fit neatly with “rational” behavior.

Economists typically assume that risk aversion is constant. I have a level of risk with which I am comfortable, and therefore I invest in a portfolio that reflects that tolerance. If I’m risk averse — maybe because I’m approaching retirement or just afraid of losing money — I tilt toward safer assets such as cash and treasuries. If I’m risk seeking — either because I need higher returns or because I have a long time horizon — I tilt toward risky assets such as stocks.

The notion of constant risk aversion suggests that we can find the right static portfolio for any individual by balancing risk and return. We can find a portfolio that compels investors to act rationally. We can construct portfolios that maximize return while reducing the urge to trade during volatile times.

This notion is under scrutiny. Recent research suggests that “irrational” investing behavior may be explainable by science. It is known that as humans endure greater stress and anxiety — the kinds of emotions our ancestors felt as they were confronted by wolves — cortisol levels increase. New research finds that as cortisol levels increase, financial risk aversion spikes. Our bodies are telling us to run away as fast as we can. From Narayanan Kandasamy and the other authors of the article “Cortisol Shifts Financial Risk Preferences”:

“…risk preferences are highly dynamic. Specifically, the stress response calibrates risk taking to our circumstances, reducing it in times of prolonged uncertainty, such as a financial crisis. Physiology-induced shifts in risk preferences may thus be an underappreciated cause of market instability.”

Today, we face a different kind of stress and anxiety than our ancestors. We are confronted with spikes in cortisol as markets get choppy and our investments lose value. It is agonizing to think about losing money. We’ve all felt that pain — it is a physical reaction to financial turbulence. This human reaction was perfectly rational when we had to face a pack of wild animals. Today, we find that it can be detrimental when dealing with bears and bulls.

Outside of the jungle, it is important for advisors and investors to understand this human behavior. Practically speaking, I think there are two primary ways to mitigate bad decision-making that could result from this physical human reaction to volatile markets:

- Investors should acknowledge that these tendencies are real and that this pain will exist. They must constantly train themselves — their brains and their bodies — to suffer through it. This requires almost constant reassurance that we’re doing the right thing, even when it feels wrong. I find that the best way to do this is to read some financial literature every day that appreciates these nuances of human behavior and investing (Barry Ritholtz, Josh Brown, Jason Zweig, and Carl Richards are a good place to start). Some people choose to lean on financial advisors or planners when their bodies are telling them to run away.

- Investors can understand this natural tendency and choose to take less risk in their portfolios, settling at a level below which they “think” they are comfortable. If you think you’re comfortable with a 60/40 (i.e. 60 percent equities, 40 percent bonds) portfolio allocation plan, maybe try a 40/60 instead, understanding that your body may not be able to handle the stress of 60 percent equities.

It is critical that we understand ourselves and our impulses before we can make wise financial decisions. Maybe we can change so that we can fit more neatly into economic models, but it’s going to take work.

Click here to sign up for the Daily Economy weekly digest!

Sources:

Kandasamy, et. al., “Cortisol Shifts Financial Risk Preferences,” March 4, 2014.

Wesley Gray, PhD, “How Market Volatility Affects Our Brains,” September 2, 2015.

Ben Carlson, CFA, “Selling is the Easy Part,” September 29, 2015.

Luke F. Delorme

Luke F. Delorme is Director of Financial Planning for American Investment Services. Articles do not constitute personal investment advice. Please seek the advice of a professional before implementing any financial decision. Luke can be reached at LukeD@americaninvestment.com.