Housing Starts and Permits Rose Again in November, But Upside Remains Limited

Housing starts and permits increased in November as total starts rose by 3.2 percent and permits for future construction rose 1.4 percent. Total housing starts increased to a 1.365 million annual rate from a 1.323 million pace in October. For housing permits, total permits were 1.482, million up from 1.461 million in October.

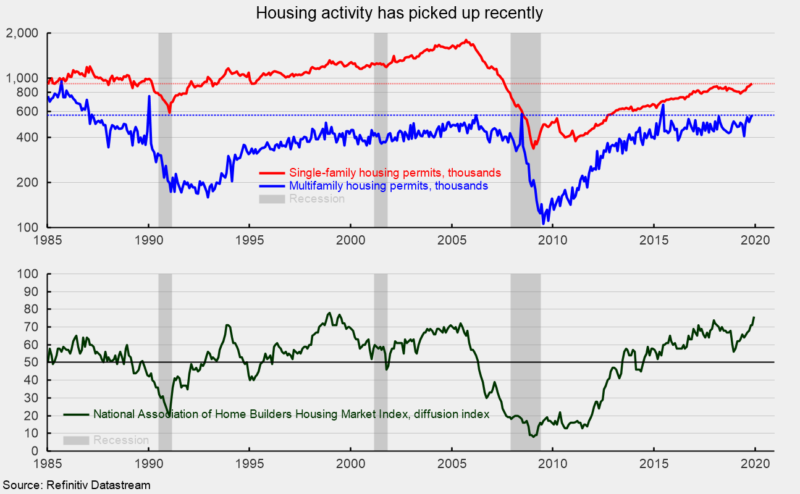

The dominant single-family segment, which accounts for about three-fourths of housing starts, rose 2.4 percent for the month to a rate of 938,000 units, marking the fifth gain in in the last six months. From a year ago, single-family starts are up 16.7 percent. Single-family permits rose 0.8 percent to 918,000 in November, the seventh monthly gain in a row and the highest level since 2007 (see top chart). Despite the recent gains, single-family starts are running below the pace of the 1990s and early 2000s.

Starts of multifamily structures with five or more units rose 2.3 percent to 404,000. From a year ago, multifamily starts are up 4.4 percent. Permits for all multifamily structures rose 2.5 percent in November to 564,000. Multifamily permits have only been at this level or higher seven times since 1987 (see top chart).

Among the four regions in the report, total starts rose in the two largest regions as the South gained 10.3 percent to 752,000 and the West rose 1.4 percent to 351,000. The Midwest fell 15.5 percent to 158,000 while the Northeast saw a 3.7 percent drop for the month to 104,000. For the single-family segment, starts surged 67.6 percent to 62,000, and rose 8.8 percent in the West to 246,000 but fell 4.1 percent to 512,000 in the South and 0.8 percent in the Midwest to 118,000.

The National Association of Home Builders’ Housing Market Index rose to 76 in December, up from 71 in November (see bottom chart). All three components of the index had gains in the latest month. The current single-family sales index rose to 84 from 77 in the prior month, expected single-family sales over the next six months rose to 79 from 78, and the index for traffic of prospective buyers increased to 58 from 54 in November. These results suggest there may be some remaining tailwind from the drop in mortgage rates earlier in the year. However, the benchmark 10-year Treasure yield has drifted higher in recent weeks which may restrain the tailwind.

Overall, single-family housing activity has posted a solid rebound over the last six months following a period of weakness from early 2018 through early 2019. The drop in mortgage rates through mid-third quarter likely provided a bit of a tailwind, but there is little evidence to suggest a significant, sustained acceleration in single-family housing activity in coming quarters. After a long economic expansion, there is likely relatively low pent-up demand, and with mortgage rates and the unemployment rate being so low for quite some time, it’s hard to see a major catalyst for a surge in activity from these levels.

Multifamily housing remains generally robust, sustaining activity at levels consistent with the prior two economic expansions. However, given the high level, it’s unlikely that it will go much higher. Therefore, total residential investment is unlikely to be a significant and sustained source of growth for the economy over the coming quarters.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.