Home Constructions Stays Strong in November

Homebuilding remains a bright spot for the economy as housing starts and permits posted gains in November while homebuilder sentiment remained strong across the country in December. Total housing starts rose to a 1.547 million annual rate from a 1.528 million pace in October, a 1.2 percent increase. The November gain is the sixth rise in the last seven months since hitting an April low.

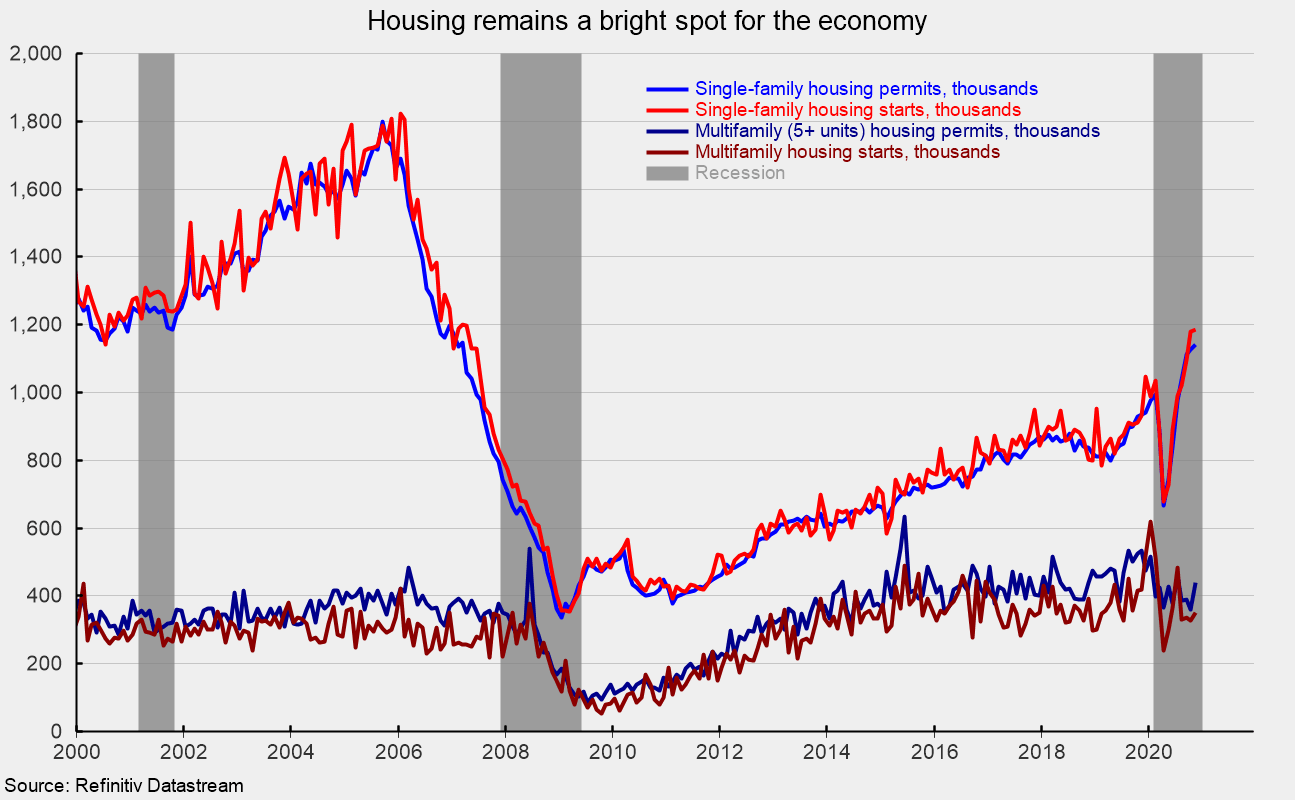

The dominant single-family segment, which accounts for more than three-fourths of new home construction, rose 0.4 percent for the month to a rate of 1.186 million (see first chart). Starts of multifamily structures with five or more units rose 8.0 percent to 352,000 (see first chart). From a year ago, total starts are up 12.8 percent with single-family starts up 27.1 percent and multifamily starts down 16.0 percent.

For housing permits, total permits rose 6.2 percent to 1.639 million in November. Total permits are 8.5 percent above the November 2019 level. Single-family permits were up 1.3 percent at 1.143 million, the highest rate since March 2007 (see first chart) while permits for two- to four-family units fell 3.5 percent to 55,000 and permits for five or more units jumped 22.8 percent to 441,000 (see first chart). Overall, single-family starts and permits are showing persistent strength since the April low while multifamily starts and permits are essentially trending sideways or slightly lower but at a level well above the lows following the 2008-09 recession (see first chart).

Among the regions in the report, total starts rose in two of the four regions. The South, the largest region by volume, fell 6.0 percent while the Midwest declined by 4.9 percent. However, the Northeast gained 58.8 percent and the West rose 8.2 percent. For the single-family segment, the pattern was similar with the South down 3.1 percent and the Midwest off 9.3 percent while the Northeast gained 5.4 percent and the West rose 12.7 percent.

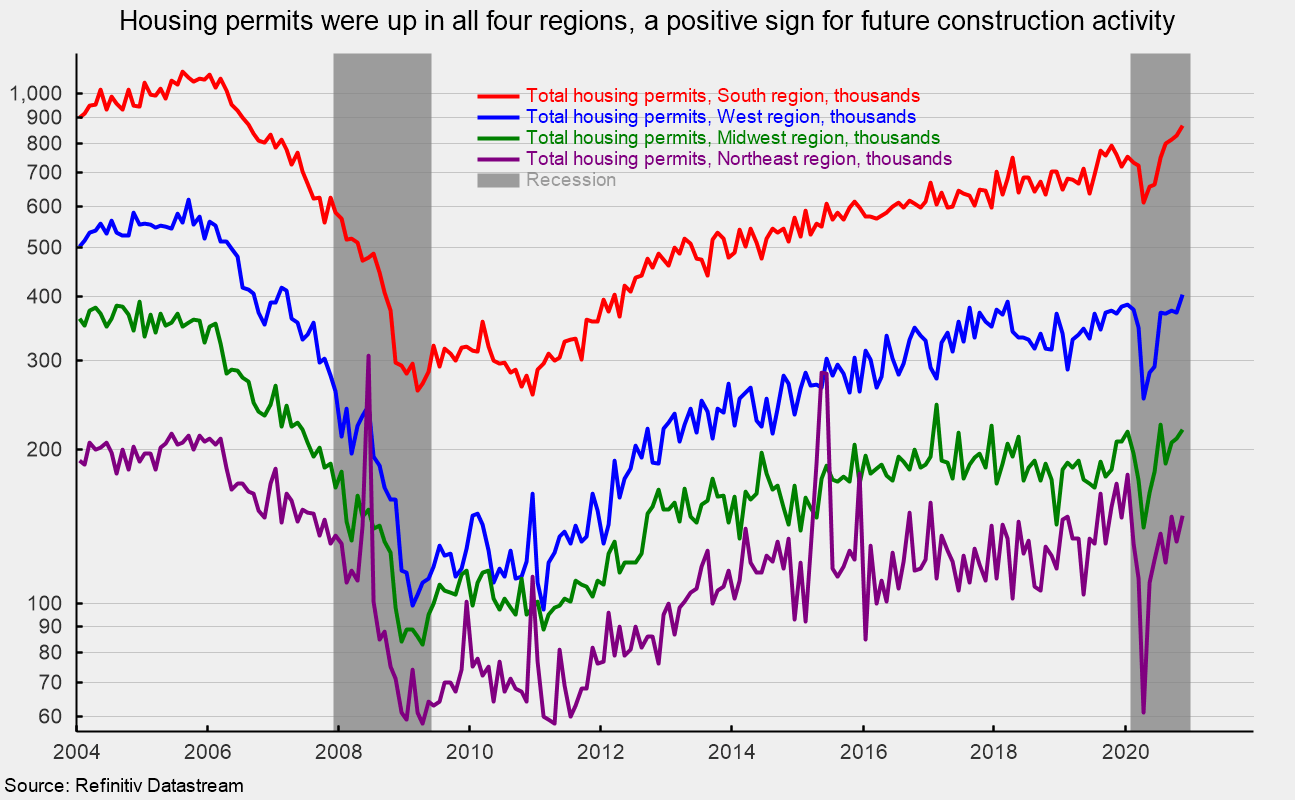

For housing permits among the regions, total permits rose in all four regions. The Northeast gained 12.9 percent, the South increased 4.7 percent, the West rose 8.3 percent and the Midwest added 3.8 percent (see second chart). Total housing permits for the South and the West are at the highest levels since the late 2000s. Permits for the Northeast and the Midwest are well above the lows following the 2008-09 recession (see second chart). For the single-family segment, permits for the Northeast increased 11.7 percent, the South gained 0.8 percent and the West rose 1.1 percent, while the Midwest was unchanged for the month.

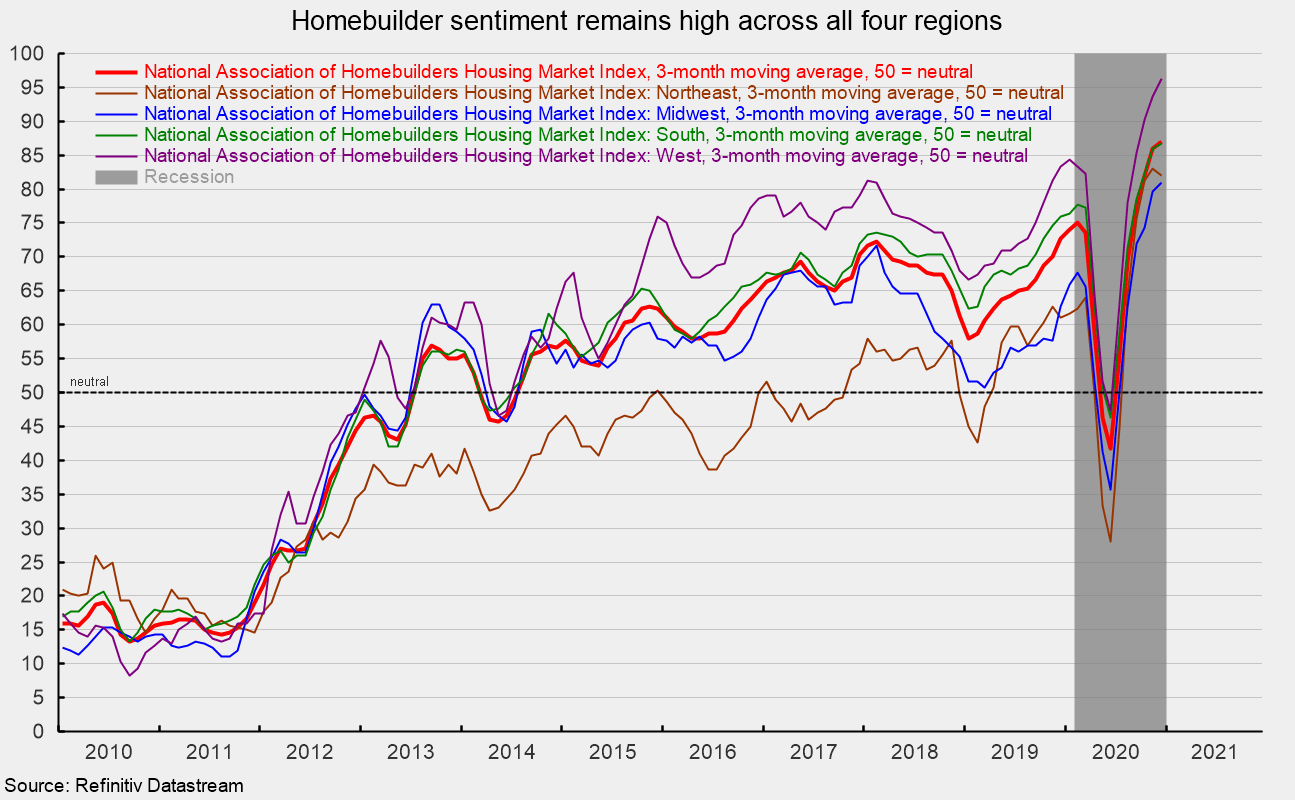

The National Association of Home Builders’ Housing Market Index, a measure of homebuilder sentiment, fell to 86 in December, down from 90 in November but still a very strong result. The three-month average, to smooth out monthly volatility, was 87 in December versus 86 in November, a record high (see third chart). All three components of the index had declines in the latest month but also remained at very high levels. On a regional basis, all four regions had declines in December but on a three-month average basis, three of the four regions have gains; all four regions were at historically high levels (see third chart).

Single-family home construction activity has recovered sharply since the April low as lockdown restrictions that impacted both construction workers and potential customers were eased. Furthermore, mortgage rates remain near all-time lows, providing support for the recovery though lending standards have tightened amid the policy-induced economic malaise.

Housing is one of the areas that may be experiencing structural change. There appears to be sustained marginal demand for less dense suburban and rural housing as urban dwellers, primarily renters, seek alternative housing. This trend could be boosted if businesses implement permanent work from home policies, to make employees happy but also to cut down on high-cost commercial real estate, especially in high-density, high-cost cities.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.