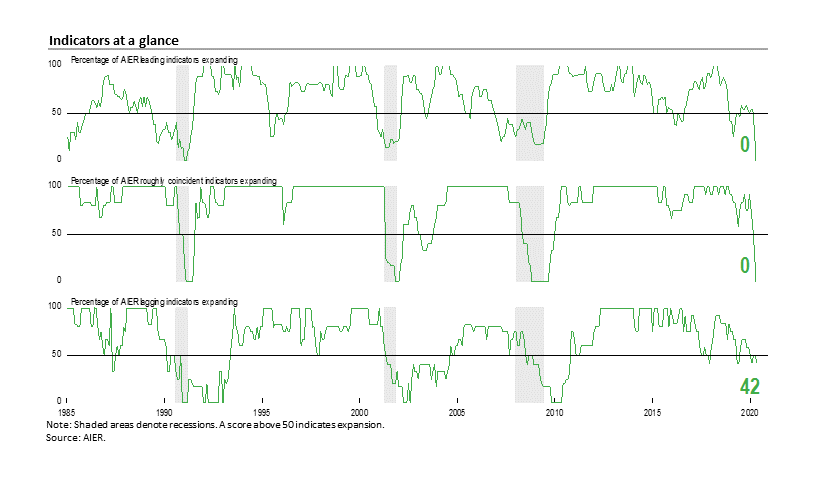

Hitting Bottom: AIER’s Leading and Roughly Coincident Indicators Indexes Drop to 0

The speed, breadth, and magnitudes of the declines in nearly every aspect of economic conditions are evident in the latest update of AIER’s Business Cycle Conditions indexes. The Leading Indicators index dropped to a reading of 0 in May, the first time since 1991 that all 12 leading indicators are showing negative trends. The Roughly Coincident Indicators index also fell to 0 while the Lagging Indicators index pulled back to 42, matching the lowest result since 2010 (see chart). The latest results leave little doubt that the U.S. economy has entered a recession, ending the longest U.S. economic expansion on record.

Despite the widespread devastation to the economy, there are reasons to be optimistic. While many economic statistics are just now reflecting the severity of the declines in activity and economic conditions, there are a few more-timely statistics that are showing signs of bottoming and modest rebounds. Those early signs are supported and encouraged by the easing of restrictions placed on people and businesses around the country.

While significant damage has been done to many industries, some parts of the economy, some measures of economic activity, may rebound relatively quickly as restrictions are lifted. The focus going forward will be to monitor progress on recovery, identifying areas that can and do rebound versus those that may be burdened with longer-lasting damage or facing new or accelerating pressures for structural change.

AIER Leading Indicators index falls to zero in May

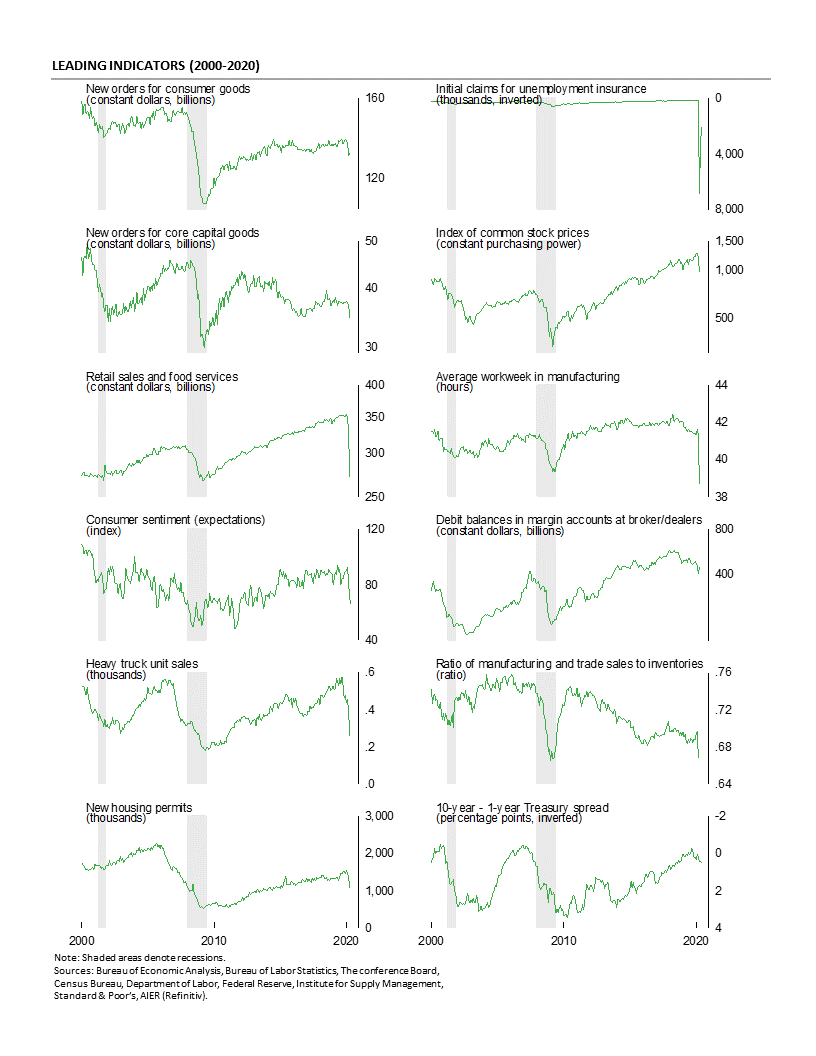

The AIER Leading Indicators index fell to 0 in May, down from 33 in the prior month. May was the first month since February 1991 that all 12 leading indicators were in unfavorable trends. Last month, 3 of the 12 leading indicators maintained a positive trend while 7 were unfavorable and 2 were in neutral trends.

Among the five leading indicators that changed trends in May, the three that went from favorable trends to unfavorable trends were the real manufacturing and trade sales to inventories ratio, housing permits, and real stock prices. The two leading indicators that went from neutral trends to unfavorable trends were the average workweek in manufacturing and real new orders for consumer goods. Initial claims for unemployment insurance, real retail sales and food services, the University of Michigan index of consumer expectations, real new orders for core capital goods (nondefense capital goods excluding aircraft), the 10-year – one-year Treasury spread, and debit balances in margin accounts all maintained unfavorable trends in May.

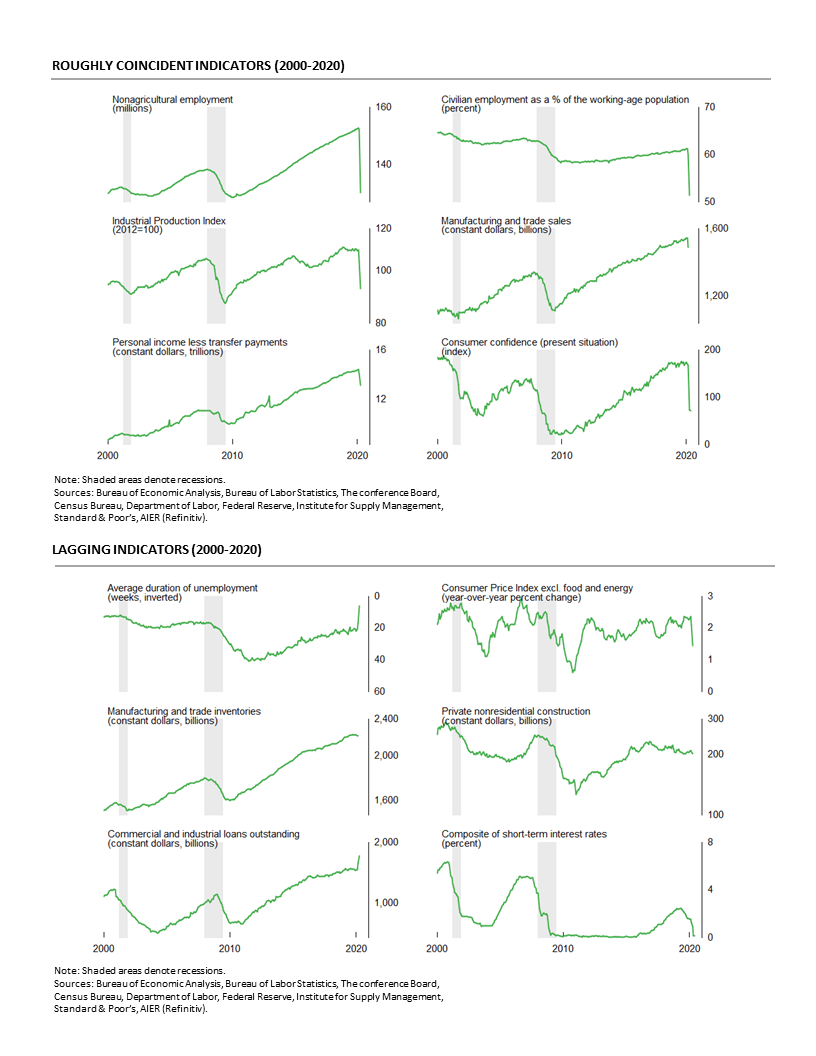

The Roughly Coincident Indicators index also fell to 0 from 33 in April. Two indicators changed direction in May. Nonfarm payrolls and real manufacturing and trade sales weakened from favorable trends to unfavorable trends. Overall, all six Roughly Coincident Indicators were trending lower in May.

Overall, the extremely weak results for both the Leading Indicators index and the Roughly Coincident Indicators index suggest the economy is in recession. However, with government mandates for shuttering of nonessential businesses and sheltering-in-place for workers and consumers already in the process of being eased, there is a rising likelihood that the rapid and severe contraction in economic activity may have hit bottom.

AIER’s Lagging Indicators index retreated to a 42 in May from 50 in April. One indicator, the 12-month change in the core consumer price index, changed trend in May, weakening from a neutral trend to a negative trend. Overall, two indicators were trending higher, three had unfavorable trends and one was neutral.

Careful monitoring of the progression of the lifting of restrictive policies (normalization), the extent of the destructive impacts across the economy and financial system, and emergence of early signs of rebound will be the key elements of useful economic analysis. Ultimately, it will be progress in understanding, treating, and preventing COVID-19 as well as policy responses to any future outbreaks that could have a significant impact on long-term prosperity.

Financial and Commodity Markets

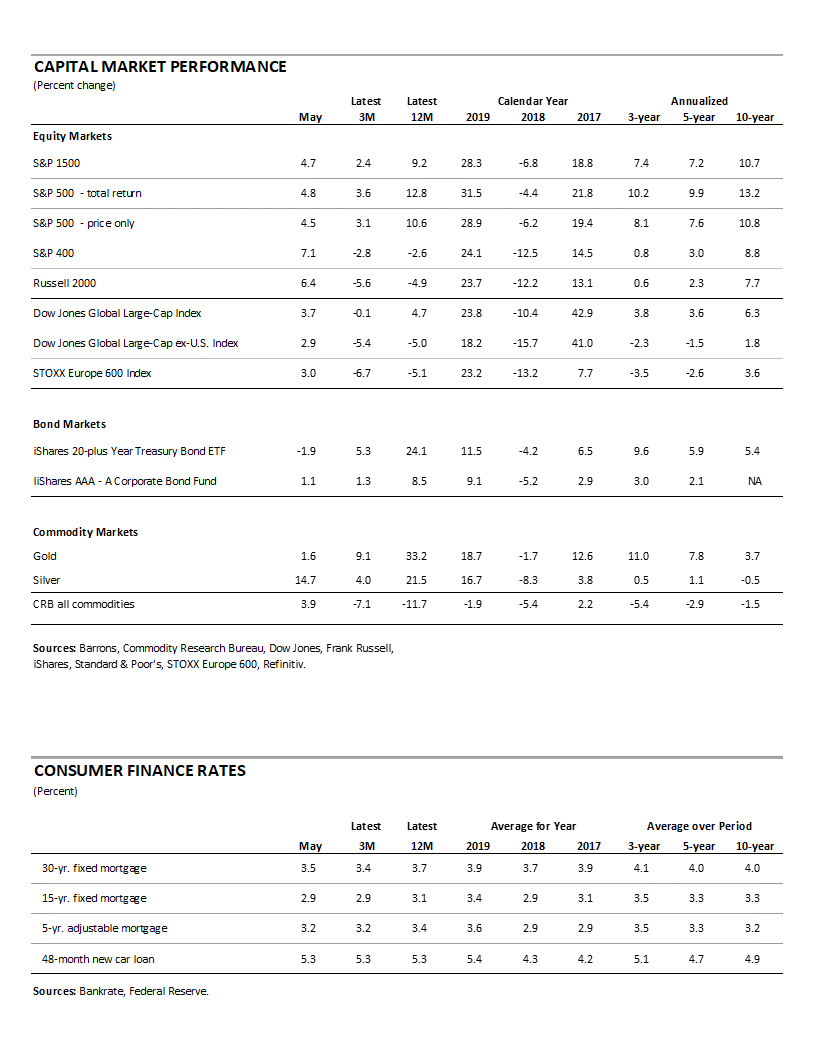

U.S. equity markets suffered deep setbacks at the outset of the COVID-19 pandemic with the Standard and Poor’s 500 index falling from a peak of 3,386 on February 19 to a low of 2,237 on March 23. That 34 percent drop, covering just 23 trading days, is one of the sharpest declines in history.

Since the low in March, the index has recovered to 3,123 as of the close on June 3, a gain of 39 percent, leaving the index just 9 percent below the all-time peak. While it may seem like a disconnect to have the U.S. equity market nearing an all-time high as many economic statistics suggest the economy may be in the midst of the worst downturn since the Great Depression, equity indexes presumably reflect investors’ expectations about the future, not necessarily current conditions or the recent past. It should also be remembered that equity indexes are not perfect predictors of the future performance of the economy and are subject to emotional and behavioral biases. Nevertheless, the strong rebound by the S&P 500 is a positive sign about the potential for economic recovery.

The VIX index, a measure of equity market volatility (often referred to as the Fear Gauge), was just under 25 on June 4, down sharply from a record high 82.69 on March 16. Though the current level is still somewhat elevated (the VIX has generally been in the 10-20 range over the last 8 years), the sharp pullback from the peak in March has a positive connotation.

While equities have recovered, Treasury yields remain near all-time lows. The yield on the benchmark 10-year Treasury note was about 0.8 percent on Thursday, June 4, just slightly above the low of 0.5 percent in early March. The extremely low yields largely represent a combination of aggressive Fed policy (0 percent fed funds target and renewed bond-buying programs), expectations of low rates of price increase, and some degree of risk aversion.

Corporate bond yields have remained relatively stable with the Moody’s BAA composite yield holding at just below 4 percent, about where it was for most of the second half of 2019. The relatively stable performance suggests corporate bond investors are not anticipating a wave of defaults among investment-grade issues.

Commodities markets have experienced a wide range of performances over recent months. Commodities tend to be more global than equities or bonds issued by any one issuer. Crude oil experienced an extremely unusual period in mid-April as spot prices and near-term futures went negative. A combination of excess supply and geopolitical tensions sent prices deeply into negative territory as the front-month contract expired. Prices have since rebounded to about $37 per barrel for West Texas Intermediate. The rebound reflects an easing of geopolitical tensions, especially between Russia and Saudi Arabia, as well as expectations for improving global demand as prospects for global economic growth recover.

Gold prices are heading back towards an all-time high, trading just over $1,712 an ounce, about 10 percent below the peak around $1,900 in September 2011. Gold often acts as a safe haven as well as a hedge against loss of purchasing power.

Banking

Financial intermediation may be at risk during crises. The health and stability of the financial institutions providing banking services as well as the willingness of those institutions to provide funding to consumers and businesses can be major factors in the depth and duration of economic downturns.

The most recent data on commercial bank lending shows total loans and leases to borrowers rose rapidly in recent weeks, posting a 12-month growth rate of 11.1 percent in April versus growth generally in the 4 – 6 percent range for most of the past 3 years. However, the increase is almost entirely from commercial and industrial loans, likely reflecting the government loans programs. Commercial real estate and residential real estate both have modest increases over the past two months while consumer loan growth has slowed sharply, posting a 12-month gain of just 1.5 percent.

Labor

The labor market remains among the most crucial components of a potential economic rebound. The national Employment Situation report for May showed U.S. nonfarm payrolls staged a modest rebound in May, adding 2.5 million jobs, with gains spread across most private-sector industries. Like the April report, there were a number of technical issues with the May report including an unusually low response rate from the household survey portion and improper coding of some classifications.

Overall, private payrolls added 3.1 million jobs in May with private services adding 2.4 million and goods-producing industries rising by 669,000. For private service-producing industries, the gains were led by a 1.2 million increase in leisure and hospitality followed by health care and social-assistance industries with a 391,000 increase and retail which added 368,000. Within the 669,000 gain in good-producing industries, construction added 464,000 jobs, durable-goods manufacturing increased by 119,000, and nondurable-goods manufacturing rose by 106,000. Mining and logging industries lost 20,000 jobs.

The unemployment rate eased down to 13.3 percent while the participation rate ticked up to 60.8 percent. Despite the improvement, the 13.3 percent rate is still higher than the two next highest cycle peaks, the 10.7 percent peak in November 1982 and the 10.0 percent peak in 2009. Though data collection was much less reliable, the unemployment rate following the Great Depression was estimated to have peaked at about 25 percent in 1933. The Bureau of Labor Statistics also noted that the technical issues with this report likely underestimated the unemployment rate by about 3 percentage points in May, meaning the actual rate was closer to 16 percent versus about 20 percent in April (if adjustments were made). The officially reported underemployed and unemployed rate, referred to as the U-6 rate, fell from 22.8 percent in April to 21.2 in May.

Initial claims for unemployment insurance totaled 1.88 million for the week ending May 30, marking the eleventh consecutive week of massive layoffs. However, claims have slowed for the ninth straight week after registering 6.87 million for the week ending March 28.

The 11-week total of 42.65 million initial claims through May 30 is almost 5 times the total 8.7 million job losses that occurred over 25 months versus during the Great Recession and nearly triple the 15.4 million peak number of unemployed people for the Great Recession of 2008-09, as measured in the household survey portion of the monthly Employment Situation report.

Consumer Spending

For the second month in a row, retail sales and food-services spending posted a record drop, plunging 16.4 percent in April following a revised 8.3 percent drop in March. Excluding the volatile motor vehicle and gas categories, core retail sales and food services were down 16.2 percent in April after a revised fall of 2.6 percent in March. Over the past year, total retail sales and food services were down 21.6 percent in April, the worst performance on record since data on retail sales began in 1992, while core retail sales and food services have fallen 16.0 percent, also a record drop.

Declines were broad-based across industries with the one exception being nonstore retailers, primarily online shopping. Nonstore retail sales rose 8.4 percent following a 4.9 percent rise in March. Over the past year, nonstore retail sales are up 21.6 percent.

There were declines in twelve retail-spending categories, with eleven posting double-digit declines. Declines were led by a 78.8 percent drop for clothing and accessory stores, followed by a 60.6 percent fall for electronics and appliance stores, a 58.7 percent fall in furniture and home furnishings, a 38.0 percent drop in sporting-goods, hobby, musical-instrument, and bookstores, a 29.5 percent decline for food services, a 28.8 percent decline for gas station sales, a 24.7 percent decrease for miscellaneous store sales, a 20.8 percent fall for general merchandise, a decrease of 15.2 percent for health and personal care store sales, a drop of 13.1 percent for food and beverage stores, a 12.4 percent decline for motor vehicle and motor vehicle–parts dealers, and a 3.5 percent pullback for building-material, garden-equipment, and garden-supplies dealers.

Sales of light vehicles totaled 12.2 million at an annual rate in May, partially rebounding from the 8.7 million pace in April (reflected in the retail sales spending above). The pace of sales in April was the lowest on record since this data series began in 1976 and follows a run of 72 months in the 16 to 18 million range from March 2014 through February 2020.

For the month of May, light-truck sales totaled 9.6 million at an annual rate, a sharp increase from the 6.7 million rate in April. Car sales had a more modest gain, rising to a 2.7 annual rate versus 2.0 in April. On a percentage basis, light trucks posted a 43 percent gain while cars had a 35 percent rise.

Manufacturing

The Institute for Supply Management’s Manufacturing Purchasing Managers’ Index improved slightly, registering a 43.1 percent reading in May, up from 41.5 percent in April. The May result is the third month in a row below the neutral 50 threshold but the first improvement following three consecutive declines and 11 declines in the last 14 months. Overall, the ISM report notes, “Three months into the manufacturing disruption caused by the coronavirus (COVID-19) pandemic, comments from the panel were cautious (two cautious comments for every one optimistic comment) regarding the near-term outlook. As was the case in April, the PMI indicates a level of manufacturing-sector contraction not seen since April 2009; however, the trajectory improved…May appears to be a transition month, as many panelists and their suppliers returned to work late in the month. However, demand remains uncertain, likely impacting inventories, customer inventories, employment, imports and backlog of orders.”

Many of the key components of the Purchasing Managers’ Index remained near levels not seen since the lows of the Great Recession in 2008-09. The New Orders Index came in at 31.8 percent, up from 27.1 percent in April. The results suggest production as measured by the Federal Reserve’s industrial production for manufacturing index may show steep declines in the coming months. The New Export Orders Index came in at 39.5 percent in May, up 4.2 percentage points from a 35.3 percent result in April.

The Industrial production report from the Federal Reserve shows output sank 11.2 percent in April, following a 4.5 percent drop in March. The April fall is the fourth drop in five months and the largest monthly decline on record. Over the past year, industrial production is down 15.0 percent and is at the lowest level since March 2010. Total capacity utilization decreased 8.3 percentage points to 64.9 percent, the lowest on record since 1950.

Manufacturing output, which accounts for about 75 percent of total industrial production, fell 13.7 percent after sinking 5.5 in March. Manufacturing output has been flat or down for four consecutive months, resulting in an 18.0 percent drop over the past year. Manufacturing utilization fell 9.7 percentage points to 61.1, also the lowest on record since 1950. Manufacturing-sector weakness was widespread with every category showing a decline.

Mining output posted a 6.1 percent decline for the month while utilities output dropped 0.9 percent in April. Over the past year, mining output is down 7.5 percent while utilities output is down 3.8 percent.

Measured by market segment, consumer-goods production was down 11.7 percent in April, with consumer durables off 36.0 percent and consumer nondurables down 5.5 percent. Business-equipment production fell 17.3 percent in April while construction supplies decreased 12.6 percent for the month. Materials production (about 46 percent of output) decreased 9.9 percent for the month and is down 12.8 percent from a year ago.

Nonmanufacturing

Like its manufacturing-sector counterpart, the Institute for Supply Management’s nonmanufacturing index showed improvement in May, rising to a reading of 45.4 from 41.8 in the prior month. The May result is the second consecutive month below the neutral 50 threshold but is also the first gain following two sharp declines in March and April. The results do suggest contraction for the services sector but at a slowing pace. They are consistent with other signs of an emerging modest rebound, coming amid efforts to ease government-imposed restrictions on people and businesses implemented to slow the spread of COVID-19.

Among the key components of the nonmanufacturing index, the business-activity index (comparable to the production index in the ISM manufacturing report) was 41.0 in May, up from 26.0 in April (the lowest reading since the survey began in 1997. For May, 13 industries in the nonmanufacturing survey reported contraction versus 17 in April.

The nonmanufacturing new-orders index rose to 41.9 from 32.9 in April. Just one industry reported growth in new orders, Agriculture, Forestry, Fishing & Hunting, while 14 reported contraction (versus 16 in April). The new-export-orders index, a separate index that measures only orders for export, was 41.5 in May, versus 36.3 in April (the lowest since November 2008.) Five industries reported growth in export orders versus three in April. Eleven industries reported declines in new-export orders compared to 14 reporting declines in April.

Housing

Housing construction activity sank in April as starts fell by 30.2 percent while new permits dropped 20.8 percent. Total housing starts dropped to 891,000 at an annual rate from a 1.276 million pace in March, the slowest pace since February 2015. The dominant single-family segment, which accounts for about three-fourths of new home construction, decreased 25.4 percent for the month to a rate of 650,000 units, also the slowest since 2015. Starts of multifamily structures with five or more units slumped 40.3 percent to 234,000, the worst since June 2013. From a year ago, total starts are off 29.7 percent with single-family starts down 24.8 percent and multi-family starts posting a 38.6 percent decline.

Total and single-family starts fell across all four regions in the report. Total starts fell 43.6 percent in the Northeast, 43.4 percent in the West, 26.0 percent in the South, and 14.9 percent in the West. For the single-family segment, starts were down 66.0 percent in the Northeast, 41.6 percent in the West, 15.0 percent in the South and 13.3 percent in the Midwest.

For housing permits, total permits fell 20.8 percent to 1.074 million from 1.356 million in March. Total permits are 19.2 percent below the April 2019 level. Single-family permits were down 24.3 percent to 669,000 in April while permits for two- to four-family units were down 30.4 percent to 32,000 and permits for five or more units were down 12.4 percent to 373,000. Combined, multifamily permits were 405,000, the slowest pace since March 2016. Permits for single-family structures are down 16.4 percent from a year ago while permits for two- to four-family structures are down 33.3 percent and permits for structures with five or more units are down 22.6 percent over the past year.

Mortgage rates have been falling since late 2018. The market reaction to the COVID-19 outbreak as well as Fed rate cuts have driven rates even lower in recent weeks. The rate on the 30-year fixed rate conventional mortgage is back below 3.5 percent, near all-time lows.

The decline in mortgage rates has helped give a small boost to the National Association of Home Builders Housing Market Index, rising 7 points to 37 in May. The 7-point gain follows a plunge of 42 points, from 72 in March to 30 in April. Lower mortgage rates and an easing of shelter-in-place restrictions should provide support for housing activity. There has been some speculation and anecdotal stories of rising demand for the lower density housing of suburbs and rural areas given the more devastating impact of the COVID-19 outbreak on high-density urban areas. Whether this turns out to be a sustained trend or a temporary reaction is likely dependent on whether an effective vaccine is developed, new, permanent regulations are imposed on urban dwellers and businesses, and whether remote work becomes a widely-available permanent option.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.