Existing-Home Sales Fell Again in July

Sales of existing homes fell in July, dropping 0.7 percent, the fourth consecutive decline. Recent data suggest momentum continues to slow. For all existing homes, including single-family and multifamily, sales fell to a 5.34 million annual rate in July versus 5.38 million in June. Sales are 1.5 percent below the July 2017 pace. Sales declined in three of the four regions tallied: the Northeast (−8.3 percent from June to July and −1.5 percent from a year ago), the Midwest (−1.6 percent for the month and −0.8 percent for the past year), and the South (0.4 percent for the month and the past year). Sales rose 4.4 percent for the month in the West but are still 4.0 percent below the July 2017 rate. Total inventory of existing homes for sale fell 0.5 percent to 1.92 million, resulting in a months’ supply of 4.3, the same as in June.

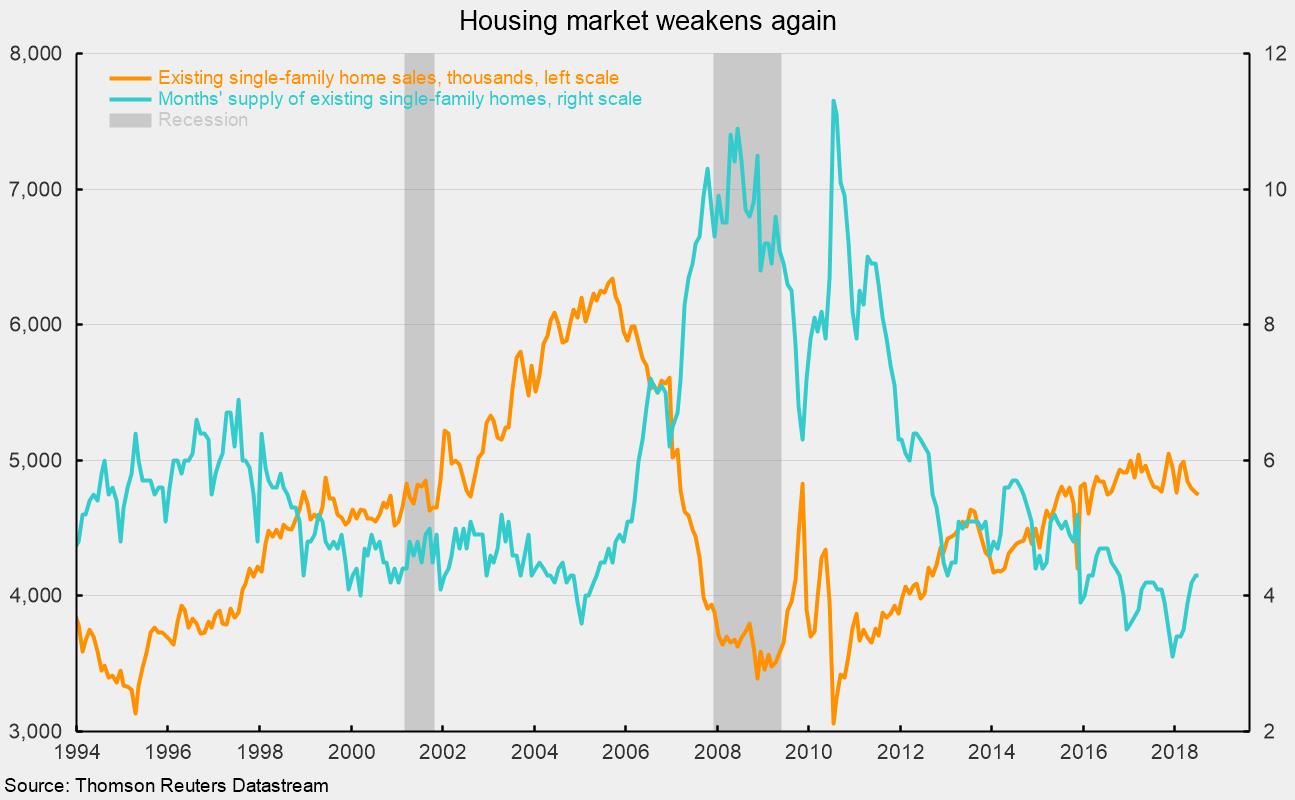

For the market for existing single-family homes, sales fell 0.2 percent to a 4.75 million seasonally adjusted annual rate in July versus 4.76 million in June (see chart). From a year ago, sales are down 1.2 percent. Across the four regions, sales fell 8.2 percent in the Northeast to 560,000 from 610,000 in the prior month while sales fell 0.8 percent in the Midwest to 1.18 million. However, sales were unchanged in the South in July, the largest region by volume, holding at a 1.97 million pace. Sales rose 5.1 percent in the West to 1.04 million versus 990,000 in the prior month.

The inventory of existing single-family homes fell 0.6 percent for the month to 1.71 million, resulting in a months’ supply of 4.3. That is unchanged from June but up 2.4 percent from a year ago and up 38.7 percent from the recent low of 3.1 months in December 2017. The sharp rise in months’ supply has brought it back from ultra-low levels to the range that prevailed during the early 2000s (see chart).

The combination of rising home prices and higher interest rates is likely weighing on housing activity in general. Home affordability overall has been trending lower after surging from 2009 to 2012 because a combination of extraordinarily low interest rates and falling home prices then made for a buyer’s market. For the housing market overall, affordability remains favorable, though the declining trend is likely to continue. For first-time home buyers, affordability is less favorable. Though it did surge along with overall affordability in the 2009–12 period, it then continued at much lower levels and is now close to neutral.

Declining affordability due to rising home prices and rising interest rates is likely to continue weighing on housing activity in general. Sales are unlikely to move significantly higher in the coming months, and new-home construction is unlikely to contribute significantly to growth in gross domestic product in coming quarters. Still, the economy overall remains very healthy, supported by a tight labor market, rising incomes, strong balance sheets, and high levels of consumer confidence. The main risks on the horizon are fallout from escalating trade wars and the ballooning federal deficits, which are likely to require significant funding in coming quarters and may drive long-term rates significantly higher.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.