Energy and Vehicle Production Fall While Other Industries Continue to Rebound

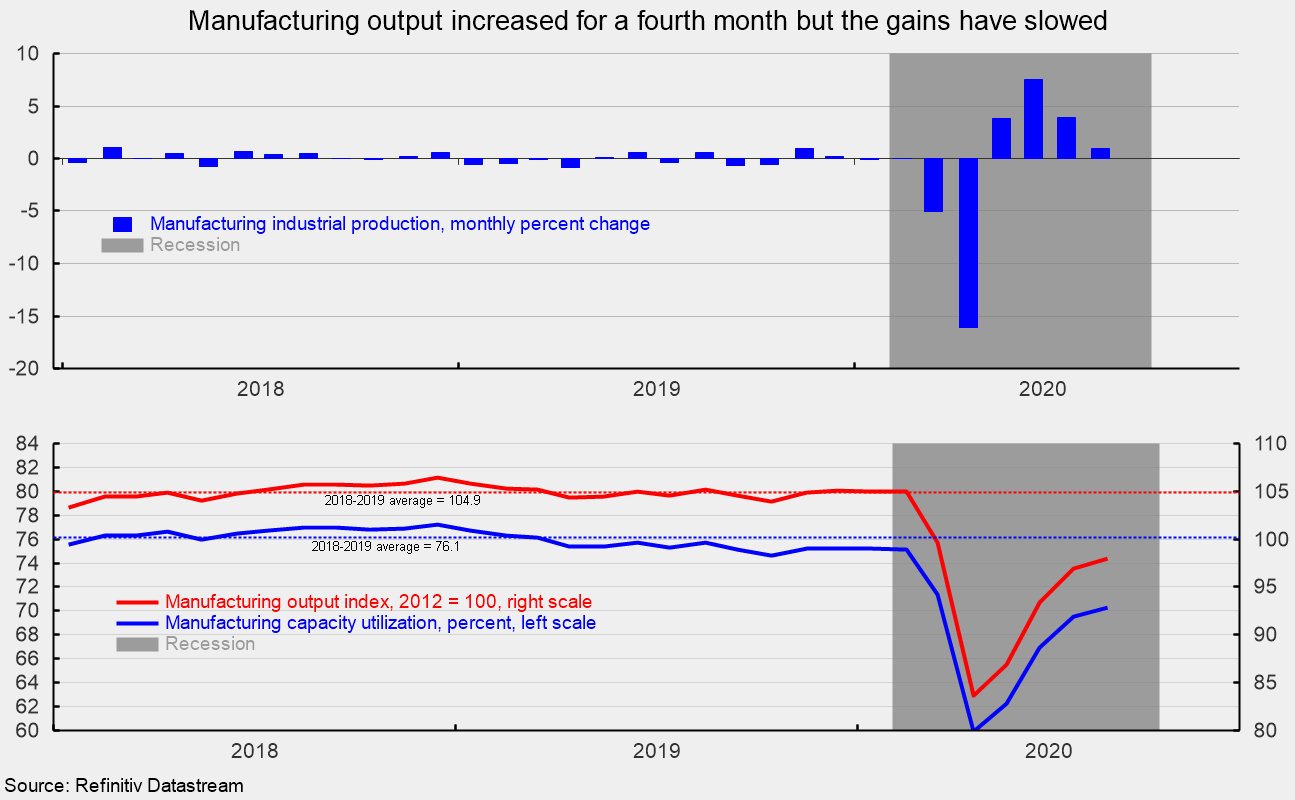

Industrial production rose 0.4 percent in August following a jump of 3.5 percent in July, a surge of 6.1 percent in June and a gain of 1.0 percent in May. However, the four consecutive months of gains were not enough to overcome the back-to-back declines of 4.4 percent and 12.9 percent in March and April, respectively. Over the past year, industrial production is down 7.7 percent and 7.2 percent below the pre-pandemic level in February.

Manufacturing output, which accounts for about 75 percent of total industrial production, rose 1.0 percent after a gain of 3.9 in July, a record increase of 7.5 percent in June, and an increase of 3.9 percent in May (see top of first chart). The four gains follow declines of 5.0 percent and 16.1 percent in March and April. The four consecutive gains still leave manufacturing output 6.9 percent below year-ago levels. With the manufacturing output index at 97.9 for August, output is 6.7 percent below the 2018-2019 average index level (see bottom of first chart).

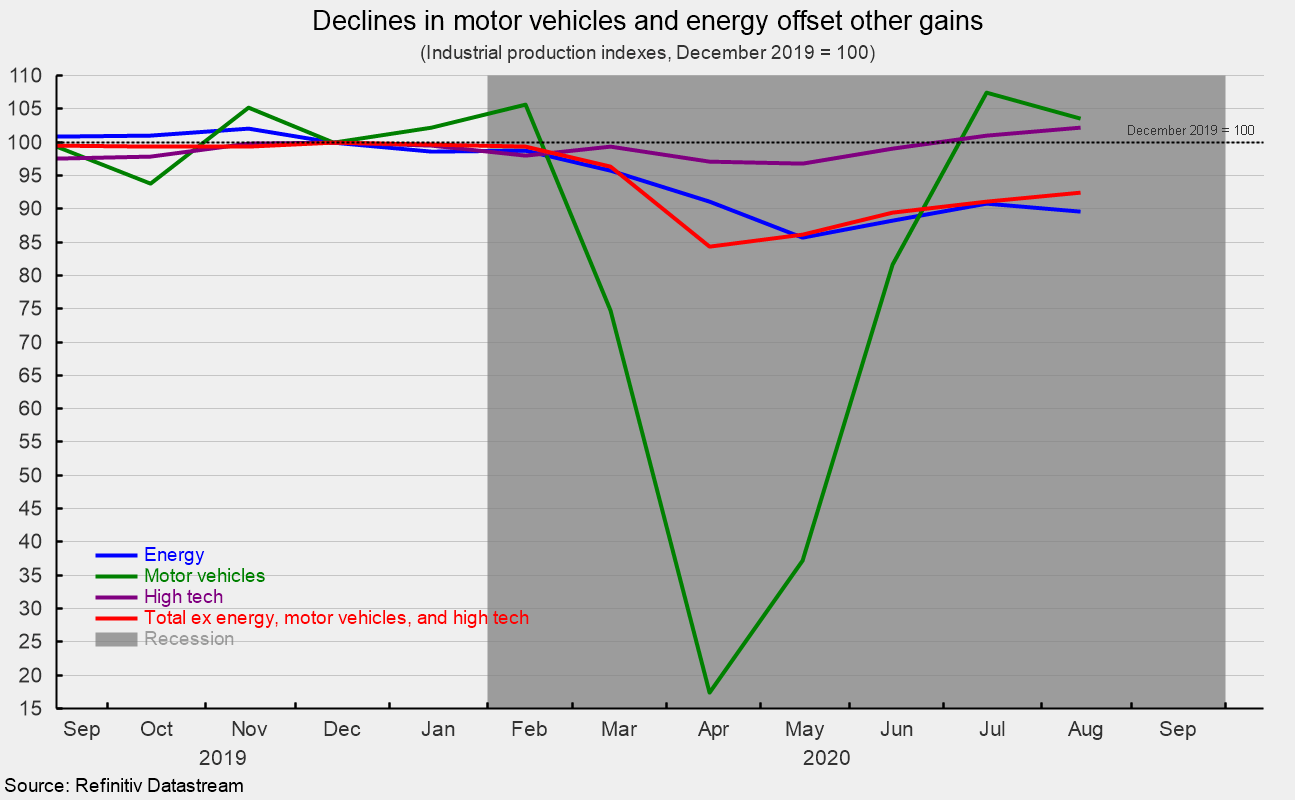

The gains in industrial production in August were generally widespread across nearly all major market and industry groups with two notable exceptions: energy and motor-vehicle production (see second chart). Energy production fell 1.3 percent for the month after gains of 2.8 percent in July and 3.0 percent in June. From a year ago, energy production is down 10.9 percent.

Motor-vehicle production, one of the hardest hit industries during the lockdowns, fell 3.7 percent in August after gains of 113.9 percent in May, 119.5 percent in June and 31.7 percent in July. Motor-vehicle production had fallen by 80 percent in March and April (see second chart).

High-tech industries output rose by 1.2 percent in August, the third monthly gain in a row and is up 4.9 percent versus a year ago. All other industries combined gained by a healthy 1.4 percent in August but are still 7.3 percent below August 2019. Compared to pre-pandemic levels, motor vehicles and high tech are above the December 2019 level while energy and the total production excluding energy, motor vehicles and high-tech index were still below (see second chart).

Total industrial utilization rose to 71.4 percent in August from 71.1 percent in July. That is well below the long-term (1972-2019) average utilization of 79.8 percent. Manufacturing utilization rose 0.7 percentage points to 70.2 percent, well below the long-term average of 78.2 percent and below the 2018-2019 average of 76.1 percent (see bottom of first chart). August data suggest that while manufacturing output is recovering, output and utilization remain soft and it may take substantial time before manufacturing returns to pre-pandemic levels.

Lockdown policies to combat the spread of Covid-19 pummeled economic activity in March and April while the easing of restrictions over the last several months has helped reverse some of the economic carnage. However, it will likely be a slow path back to pre-pandemic levels of activity for the manufacturing sector overall. But as with the rest of the economy, individual industries are showing significantly varying paths of recovery.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.