Does Anyone Trust the Fed?

In August, the Federal Reserve introduced its new monetary policy strategy of Average Inflation Targeting. This measure was expected to increase price inflation in the short run by raising the public’s expectations of higher prices in the future. Based on evidence from financial markets and even from the Fed’s own forecasts, it does not appear to have done so.

The reason the new policy has failed is that no one seems to trust the Fed to achieve its policy goals. There are, however, tools the Fed could use to improve its credibility and make its monetary policies more effective.

The new policy: Average Inflation Targeting

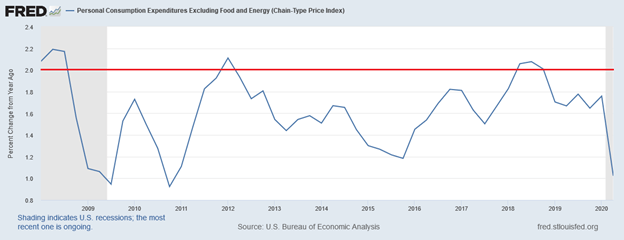

In 2012, the Fed officially adopted a target rate of 2 percent inflation. Since that time, however, rates of inflation have been consistently below the 2 percent target. The rate of inflation in “core” personal consumption expenditures (PCE), for example, has averaged just 1.6 percent over the past decade and has met or exceeded the 2 percent objective in only four quarters over that period.

The 2 percent target was intended to be symmetric. Any deviations from 2 percent were expected to be random errors due to the imprecise nature of monetary policy. Sometimes inflation would stray above 2 percent, and sometimes it would fall below, but it would average out to 2 percent over time. Since inflation has repeatedly undershot the Fed’s target for more than a decade, it is clear that this symmetry has not been achieved.

The new policy of Average Inflation Targeting explicitly commits the Fed to the symmetric outcomes it had hoped to achieve with its previous policy. The new policy dictates that if inflation has recently been below its 2 percent target, the Fed will intentionally allow inflation to run above 2 percent in the future to make up for its past shortfalls.

This change in future policy should also affect the current rate of inflation. If consumers and businesses believe that prices will be higher in the future, then some consumers will spend more today, and some businesses will begin to raise prices. Thus, by raising expectations of long-run inflation, the policy can increase short-run inflation as well.

One problem with this strategy is that it will only be effective if the Fed is credible in its commitment to the new policy and, hence, to future inflation. Here the Fed faces a paradox of trust. The policy of Average Inflation Targeting only matters if inflation has been persistently above or below the target rate. But if inflation has persistently missed the target rate in the past, the public might not trust the Fed to achieve its new target rate in the future.

If the Fed has consistently undershot its old target, why would anyone trust it to hit the new one?

The current inflation outlook

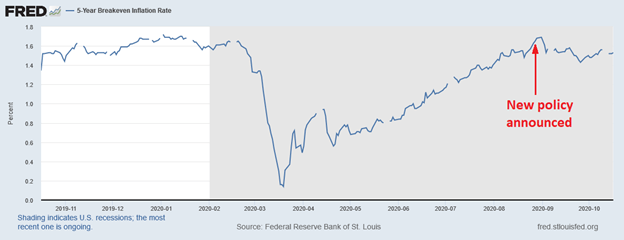

Has the new policy of Average Inflation Targeting raised the public’s expectations of long-term inflation? If so, we should see an increase in short-run inflation expectations reflected in financial market prices.

One common market indicator of inflation is the breakeven rate on Treasury Inflation Protected Securities (TIPS). The difference between market rates on 5-year Treasury securities and 5-year TIPS tells us what average rate of inflation investors expect over the coming five years. This market rate accurately predicted the below-target rates of inflation over the previous decade. The spread collapsed in March during the early days of the coronavirus crisis, but it has since climbed back to its prior level of around 1.6 percent.

If the Fed’s new policy of Average Inflation Targeting were effective, we should see an increase in inflation expectations around the time of its announcement in late August. But inflation expectations have not increased since the announcement. If anything, they have fallen. This evidence indicates that investors do not trust the Fed to achieve above-target rates of inflation in the future.

In fact, it is not clear that the Fed itself believes it can achieve its inflation goals. At the September 15 meeting of the Federal Open Market Committee (FOMC), which sets the Fed’s monetary policy, the members forecast that the rate of PCE inflation would not reach 2 percent until the year 2023.

The fact that FOMC members did not raise their own expectations of short-run inflation indicates that not even they trust the Fed to achieve its monetary policy goals.

What can the Fed do?

To build credibility, the Fed must take actions to show the public it is committed to achieving its policy goals. Even with its policy rates cut to near zero, and despite undershooting its inflation target for more than a decade, Fed Chair Jerome Powell said in September that the Fed is “not out of ammo” and still has tools for expansionary monetary policy.

One tool is open market purchases which, according to Powell, “total $120 billion per month.” These purchases, he said, are “providing accommodative financial conditions and supporting growth.” But if they are supporting growth, then why not expand them until inflation moves closer to the Fed’s inflation target?

Another, possibly more effective, method is to reduce the rate of interest on reserves (IOR) that the Fed pays to U.S. banks. A higher rate of IOR reduces the effectiveness of open market purchases since it encourages banks to hold higher excess reserves rather than lending the money out to businesses or individuals. A lower rate, in contrast, encourages lending.

Following the 2008 financial crisis, the Fed used IOR to sterilize its asset purchases to prevent them from creating inflation. Its recent open market purchases have also been muted by this IOR policy. While the current IOR rate of 0.1 percent is lower than the 0.25 percent following the financial crisis, even this low rate makes reserves attractive relative to lending since reserves at the Fed are completely risk-free. Lowering the rate of IOR would make the Fed’s asset purchases more effective and possibly even unnecessary.

Powell’s comment that the Fed is not “out of ammo” was intended to reassure the public that the Fed will do whatever it takes to achieve its monetary policy goals. Unfortunately, the Fed’s actions do not support that sentiment.

Until the Fed acts to build trust and credibility with the public, its policy of Average Inflation Targeting will have little effect on inflation or economic activity.

Thomas L. Hogan

Thomas L. Hogan, Ph.D., is senior research fellow at AIER. He was formerly the chief economist for the U.S. Senate Committee on Banking, Housing and Urban Affairs. He has also worked at Rice University’s Baker Institute for Public Policy, Troy University, West Texas A&M University, the Cato Institute, the World Bank, Merrill Lynch’s commodity trading group and for investment firms in the U.S. and Europe. Dr. Hogan’s research has been published in academic journals such as the Journal of Macroeconomics and the Journal of Money, Credit and Banking. He has appeared on programs such as BBC World News, Stossel TV, and Bloomberg Radio and has been quoted by news outlets including CNN Business, American Banker, and the National Review.