Consumers Drive Third-Quarter GDP Higher

Real gross domestic product rose at a 3.5 percent annualized rate in the third quarter, down from a 4.2 percent pace in the second quarter, according to the Bureau of Economic Analysis. Growth was driven primarily by strong gains in consumer spending; business investment and government spending made small contributions. Consumer-price increases decelerated in the third quarter versus the prior quarter. Overall, the report suggests the U.S. economic expansion remains on track.

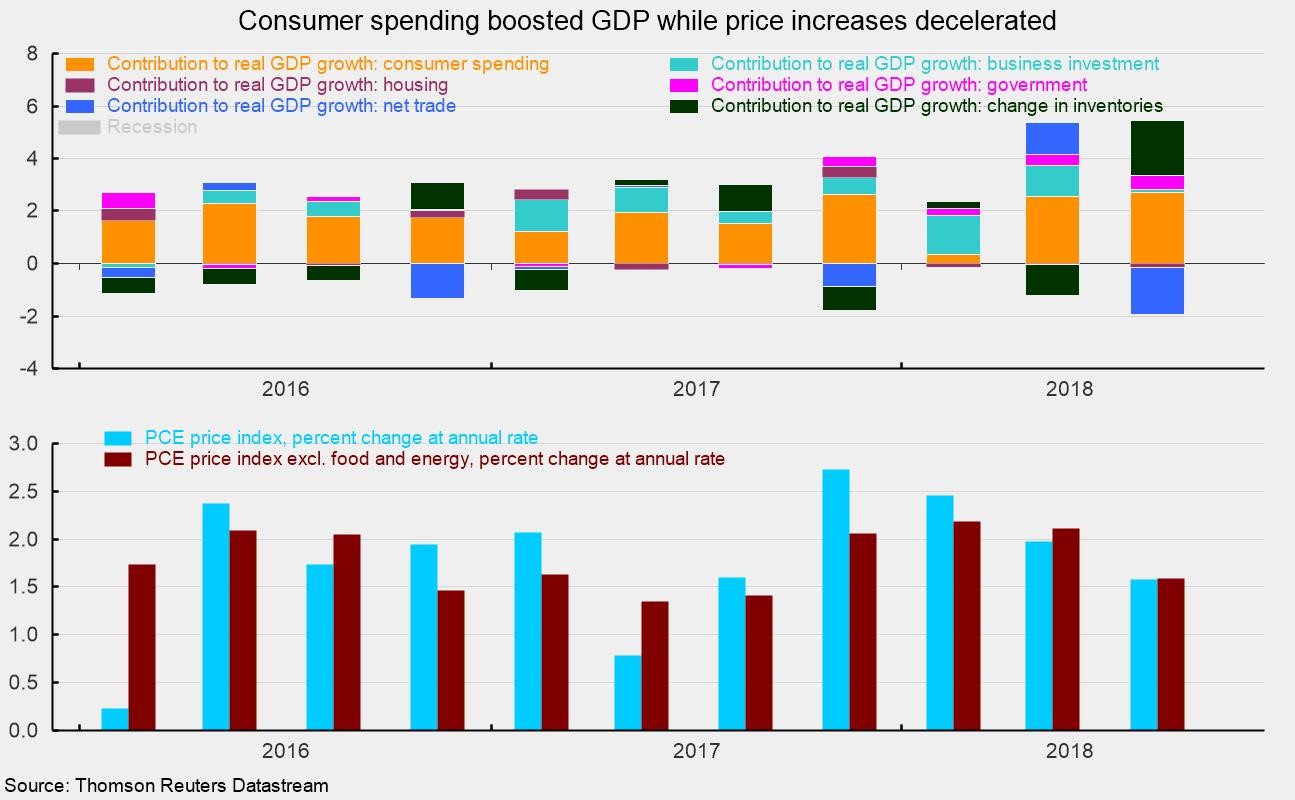

Consumer spending accelerated in the third quarter, rising at a robust 4.0 percent pace compared to a 3.8 percent growth rate in the second quarter. The acceleration was broad-based across the major segments of consumer spending, with durable-goods spending rising 5.8 percent, nondurable-goods spending up 5.2 percent, and services gaining 3.2 percent. Consumer spending contributed 2.7 percentage points of the 3.5 percent real GDP growth rate versus 2.6 percentage points in the second quarter (see chart).

Business fixed investment rose at a 0.8 percent annualized rate in the third quarter, slower than the 8.7 percent pace of the second quarter. At annualized rates, the gain was led by a 7.9 percent jump in intellectual property spending while spending on equipment rose 0.4 percent. Investment spending on structures fell 7.9 percent following two quarters of double-digit growth. Real business investment contributed 0.12 percentage points to overall real GDP growth versus a 1.15 percentage-point contribution in the second quarter.

Residential investment, or housing, fell at a 4.0 percent pace in the third quarter compared to a 1.3 percent decline in the prior quarter and a 3.4 percent drop in the first quarter. Housing continues to face a challenging environment with rising interest rates and elevated home prices dragging down affordability.

Altogether, business and residential investment declined at a 0.3 percent pace in the third quarter, subtracting 0.04 percentage points from total GDP growth compared to a 1.10 percentage-point contribution in the second quarter.

Inventory accumulation by businesses surged in the third quarter, adding 2.07 percentage points to third-quarter growth after subtracting 1.17 percentage points in the prior quarter. However, that was mostly offset by weaker net trade. Net trade had a negative impact on overall GDP growth in the third quarter, subtracting 1.78 percentage points. Exports fell at a 3.5 percent pace while imports grew at a 9.1 percent rate. It is unclear whether trade patterns are being impacted by uncertainty over trade policy and the deteriorating environment for global trade.

Government spending rose at a 3.3 percent annualized rate in the third quarter compared to a 2.5 percent increase in the second quarter, contributing 0.56 percentage points to growth versus a 0.43 percentage-point contribution in the prior quarter. Government spending rose in nearly every category, with federal defense spending up 4.6 percent, federal nondefense spending up 1.5 percent, and state and local spending up 3.2 percent. Exploding federal deficits remain one of the most significant risks to the medium- and long-term outlook for the economy.

Real final sales to private domestic purchasers, a key measure of private domestic demand, rose at a very healthy 3.1 percent annualized rate in the third quarter, down from a 4.3 percent pace in the second quarter. The third-quarter gain was the fifth time in the past seven quarters that growth exceeded 3 percent.

The underlying trend in real private domestic demand remains well-supported by continued job creation, rising wages, healthy corporate and consumer balance sheets, solid corporate-sales and corporate-earnings growth, and high levels of business and consumer confidence. The virtuous cycle between the consumer and corporate sectors is likely to provide ongoing support for further gains in real private domestic demand, suggesting continued economic expansion in the months and quarters ahead. The positive outlook is further support by the results of the AIER Leading Indicators index, which scored a healthy 88 in September.

The main risks to the outlook include disruptions to global trade flows due to policy uncertainty or policy changes (such as tariffs or abandoning trade agreements), ballooning federal budget deficits that may drive long-term interest rates higher, and a policy mistake by the Federal Reserve. For now, there are few data to support a change in the current path of monetary policy. Getting to a neutral rate and moving to the sidelines may be the best path forward, while maintaining as much transparency as possible.

On the prices side, consumer prices — the PCE (personal consumption expenditures) price index — rose at a 1.6 percent pace in the third quarter, slower than the 2.0 percent pace in the second quarter. The rate of increase in the PCE price index has decelerated for three consecutive quarters (see chart). Over the past four quarters, the increase is 2.2 percent. For core consumer prices, which exclude volatile food and energy components, the index rose 1.6 percent, down from 2.1 percent in the prior quarter. Over the last four quarters, core consumer prices rose 2.0 percent. Core consumer-price increases have been slowly drifting higher over the past several quarters but appear unlikely to accelerate dramatically in the quarters ahead.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.