Consumer Spending and Manufacturing Output Improve in June

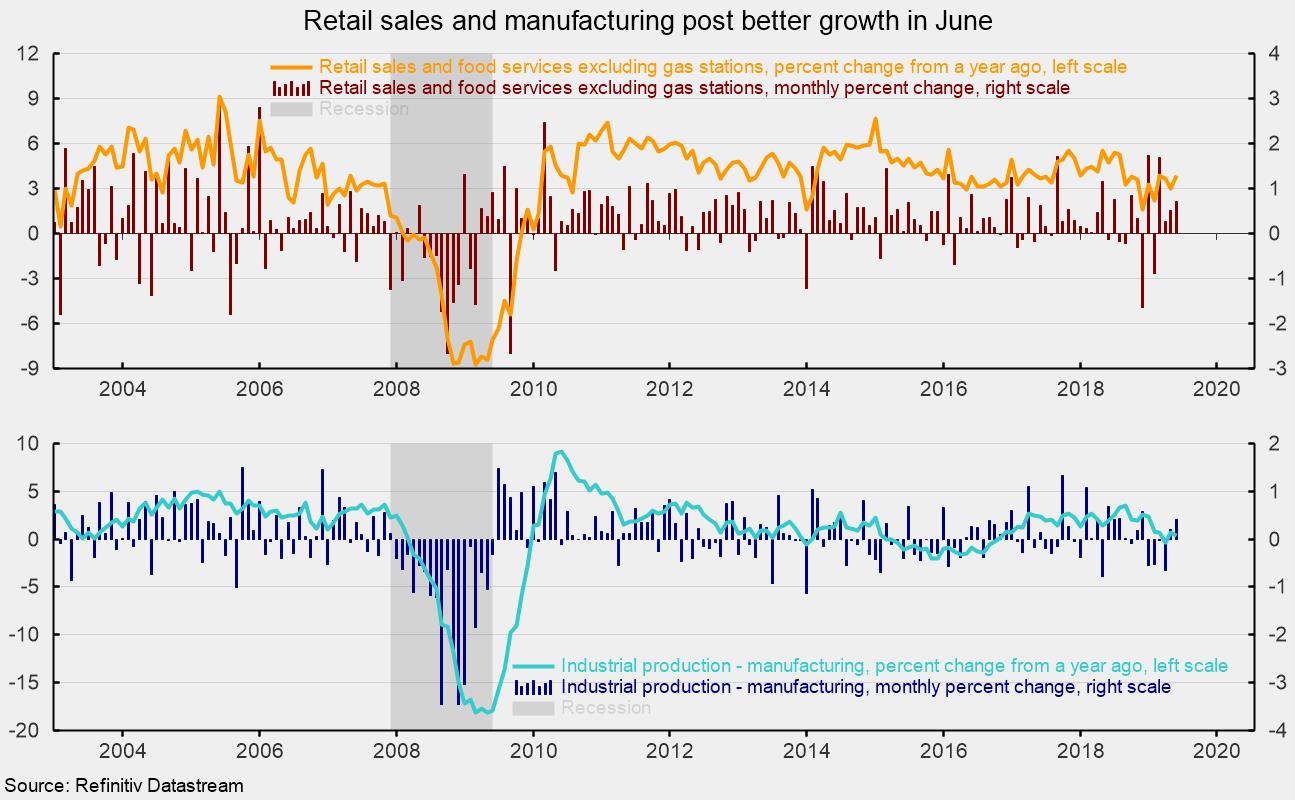

Retail sales and food-services spending increased 0.4 percent in June following a 0.4 percent gain in May. Excluding gasoline station sales, retail sales and food services were up 0.7 percent in June after a gain of 0.5 percent in May. Over the past year, total retail sales and food services were up 3.4 percent through June, while retail sales and food services excluding gas have increased 3.9 percent (see top chart).

Strength in June was widespread, with gains in 10 retail-spending categories, with just two showing declines and one essentially unchanged. Gains were led by a 1.7 percent increase for nonstore retailers, a 0.9 percent gain for food services, a 0.7 percent rise in motor vehicles and parts, and a 0.6 percent boost in miscellaneous store retailers. Five other categories had gains of 0.5 percent for the month.

On the negative side, gas station sales were down 2.8 percent, though volatility in gasoline spending tends to reflect changes in prices rather than changes in volume. Lower expenditures at gasoline stations can mean more disposable income in consumers’ pockets. Also declining in June were sales for electronics and appliance stores while sporting-goods, hobby, musical-instruments, and book stores were essentially unchanged for the month.

Industrial production was unchanged in June, following a 0.4 percent gain in May. Over the past year, industrial production is up just 1.3 percent. Total capacity utilization decreased 0.2 percentage points to 77.9 percent as capacity posted a 0.2 percent gain for the month and 2.1 percent increase over the past year.

Manufacturing output, which accounts for about 75 percent of total industrial production, rose 0.4 percent after increasing 0.2 percent in May. Manufacturing output has been flat or down for four of the past six months, contributing to a very weak 0.4 percent rise over the past year (see bottom chart).

Mining output posted a 0.2 percent gain for the month while utilities output dropped 3.6 percent in June. Over the past year, mining output is up 8.7 percent while utilities output is down 2.6 percent.

Manufacturing-sector strength was led by sharp gains in production of motor vehicles and petroleum products. Total motor vehicle and motor vehicle–parts production was up 2.9 percent for the month as vehicle assemblies increased to 11.63 million at a seasonally adjusted annual rate from 11.10 million in May. Both segments of light vehicles showed increases for the month with automobile assemblies rising to 2.62 million and light trucks rising to 8.65 million. Medium and heavy trucks fell to 0.35 million from 0.37 million in the prior month. Petroleum-products production grew 2.5 percent after posting a 0.4 percent rise in the prior month. Over the past year, motor vehicle production is up 2.4 percent while petroleum-product production is up 0.2 percent.

Measured by market segment, consumer-goods production was unchanged in June, with consumer durables up 1.3 percent and consumer nondurables down 0.4 percent. Business-equipment production increased 0.5 percent in June, the same gain as construction supplies.

Materials production (about 46 percent of output) decreased 0.2 percent for the month but is up 2.6 percent from a year ago. The energy component has been a major source of volatility in this category, particularly following the collapse of energy prices in mid-2014. The non-energy component rose 0.2 percent for the month and is up 0.2 percent from a year ago.

Manufacturing-capacity utilization rose to 75.9 percent in June, up 0.3 percentage points from 75.6 percent in May.

The stronger retail sales and manufacturing data for June are positive signs for second-quarter gross domestic product. However, the persistence of mixed economic data and uncertainty surrounding monetary and trade policy suggest continued caution.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.