Consumer Confidence Holds Steady While Home Prices Move Higher

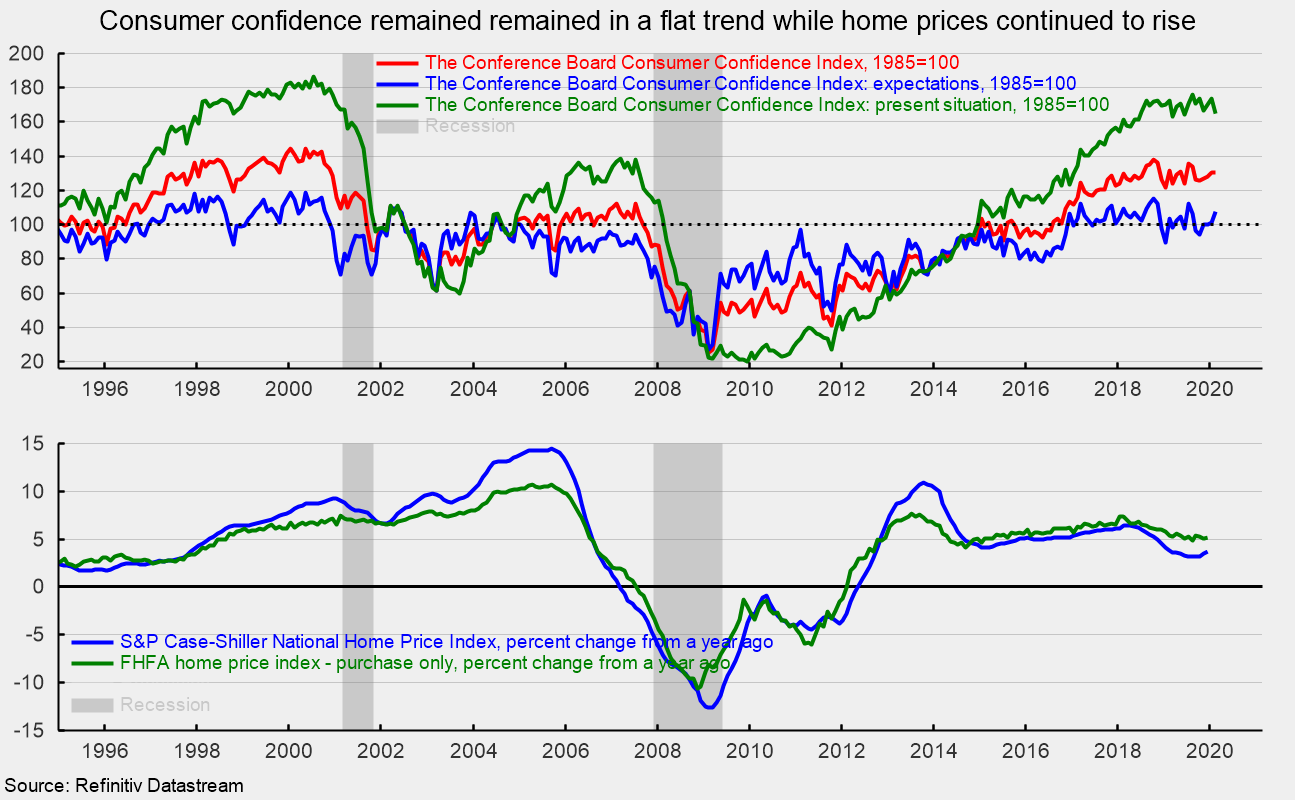

The Consumer Confidence Index from The Conference Board was little changed in February, increasing by just 0.3 points to 130.7, and just slightly ahead of the two-year average of 129.5. The index is constructed so that it equals 100 in 1985 (see top chart).

The two components had nearly offsetting results for the month. The present-situation component fell 8.8 points to 165.1, about in line with the July 2018 reading of 166.1. The two-year average for this index stands at 168.3 (see top chart again).

The expectations component added 6.4 points, taking it to 107.8 from 101.4 in the prior month. The expectations index has been a bit more restrained compared to the present-situation index. The index has been holding around the 100 level since December 2016, averaging 104.1 over the last 36 months.

Overall, consumer attitudes remain at historically favorable levels, driven by solid gains in income and a tight labor market. The persistently high level of consumer confidence is a positive sign for consumer spending and the economy overall.

The S&P Case-Shiller National Home Price Index rose 0.5 percent in December, pushing the 12-month change to 3.7 percent. A related measure, the home price index from the Federal Housing Finance Agency shows home prices for recently purchased homes rose 0.6 percent for the month of December and are up 5.2 percent from a year ago. Both measures suggest home prices have been averaging around 5 percent per year gains since 2013 (see bottom chart). They also suggest home prices are anywhere from 15 percent to 25 percent above peak prices from the housing bubble of 2004 through 2007.

Elevated home prices are offsetting the positive benefits of low mortgage rates and solid consumer fundamentals of low unemployment, rising incomes, and high consumer confidence. Elevated home prices are likely contributing to the generally moderate pace of home sales and new home construction. Given the countervailing forces, housing is unlikely to contribute significantly on a sustained basis to economic growth over the next several quarters.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.