Consumer Attitudes Remain Buoyant

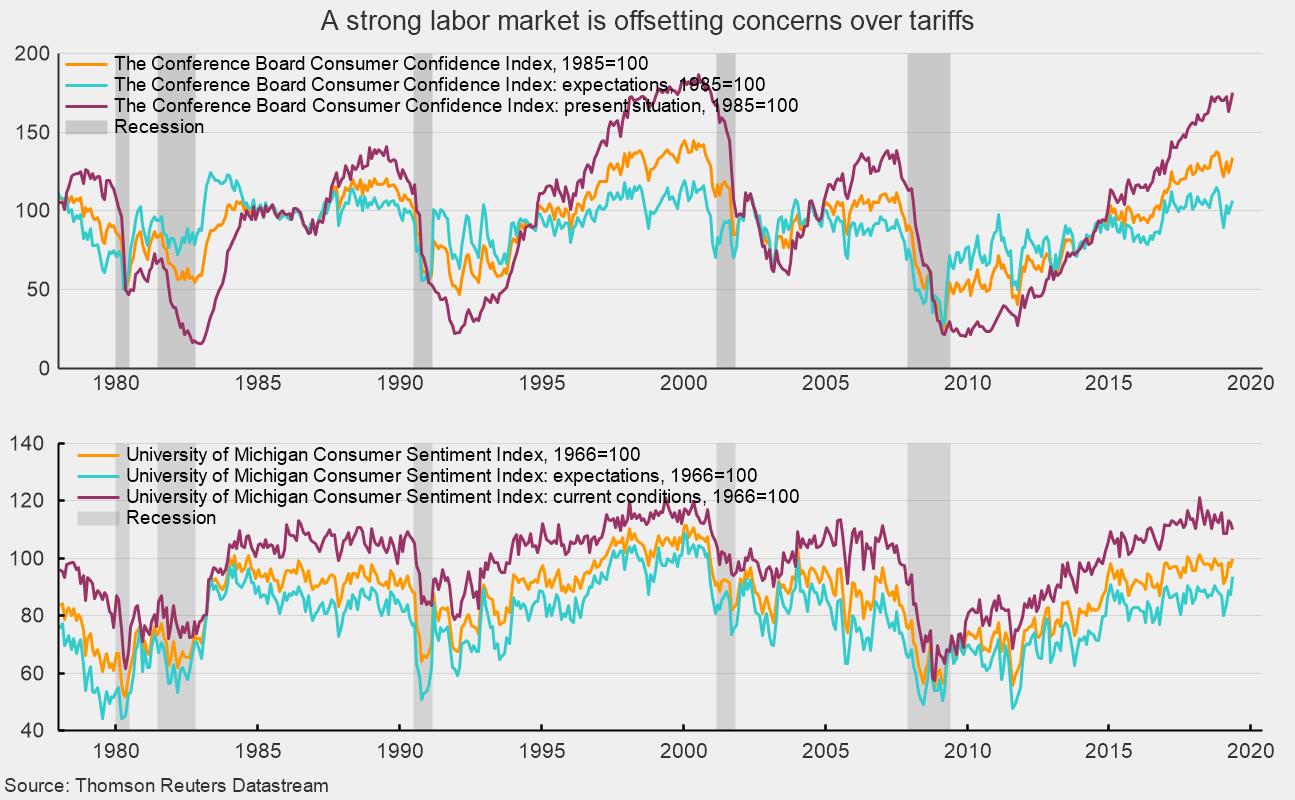

The Consumer Confidence Index from The Conference Board rose in May, increasing by 4.9 points to 134.1. The index is constructed so that it equals 100 in 1985. May was the third increase in a row for overall consumer confidence and is at the highest level since November, just 3.8 points below the recent high of 137.9 in October (see top chart).

Both components of the index posted gains for the month. The present-situation component rose 6.2 points to 175.2, hitting a new cycle high and reaching the highest level since December 2000. This index has posted a remarkable rebound, rising 155 points from a low of 20.2 in December 2009, just after the end of the Great Recession.

The expectations component added 3.9 points, taking it to 106.6 from 102.7 in the prior month. The expectations index has been a bit more restrained compared to the present-situation index but has risen sharply from a reading of 27.3 in May 2009. The index has been trending sideways over the last two years, averaging 104.8 over the last 30 months and registering readings above 100 in 25 of those 30 months. The all-time high for the expectations component is 125.8, recorded in April 1967.

According to The Conference board, “The increase in the Present Situation Index was driven primarily by employment gains. Expectations regarding the short-term outlook for business conditions and employment improved, but consumers’ sentiment regarding their income prospects was mixed. Consumers expect the economy to continue growing at a solid pace in the short-term, and despite weak retail sales in April, these high levels of confidence suggest no significant pullback in consumer spending in the months ahead.”

The May results from the University of Michigan Surveys of Consumer Sentiment show overall consumer sentiment improved from the final April result. Consumer sentiment increased to 100 in May, up from 97.2 in April, a 2.9 percent gain. From a year ago, the index is up 2.6 percent. Overall sentiment is holding at a very favorable level (see bottom chart).

The two sub-indexes had mixed performances in May. First, the current-economic-conditions index fell to 110.0 from 112.3 in April (see bottom chart). That is a 2.0 percent decline for the month and a 1.6 percent decrease from May 2018.

The second sub-index — that of consumer expectations, one of the AIER leading indicators — increased a robust 7.0 percent for the month, to 93.5 (see bottom chart), and was 4.9 percent higher than a year ago.

According to the Survey of Consumers chief economist, Richard Curtin, “Although consumer sentiment remained at very favorable levels, confidence significantly eroded in the last two weeks of May. The late-month decline was due to unfavorable references to tariffs, spontaneously mentioned by 35% of all consumers in the last two weeks of May, up from 16% in the first half of May and 15% in April and equal to the peak recorded last July in response to the initial imposition of tariffs.”

Furthermore, with regard to the potential impact of the higher tariffs, the report states, “The year-ahead inflation expectations jumped to 2.9% in May up from last month’s 2.5%. Year-ahead inflation expectations among those who unfavorably mentioned tariffs was 0.5 percentage points higher than those who made no references to tariffs. Importantly, the gain in inflation expectations was recorded prior to the actual increases in consumer prices due to the most recent hike in tariffs. While higher inflation expectations modestly reduced real income expectations, the largest impact was on buying conditions for appliances and other large household durables, which fell to their lowest level in four years.”

Overall, consumer attitudes remain at historically favorable levels, supported by a strong labor market and positive short-term expectations for the economy. However, the escalating trade wars and higher tariffs are having a significant negative impact on consumer attitudes and could potentially impact consumer spending habits.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.