Confiscatory Taxes Don’t Increase Equality

Over the past decade, the specter of rising inequality has attained renewed prominence in economic analysis. Armed with empirical evidence of increasing income concentration among the proverbial “1 percent,” politicians routinely invoke inequality relief as an explicit objective of taxation.

This emphasis on income distributions represents a shift away from the traditional grounding of taxes in a combination revenue considerations, such as deficit reduction, and macroeconomic fiscal objectives, such as a claimed economic stimulus effects from a tax cut. Instead, most inequality theorists approach tax rates as a tool to supposedly rein in the excesses of wealth and close the gap between the rich and poor.

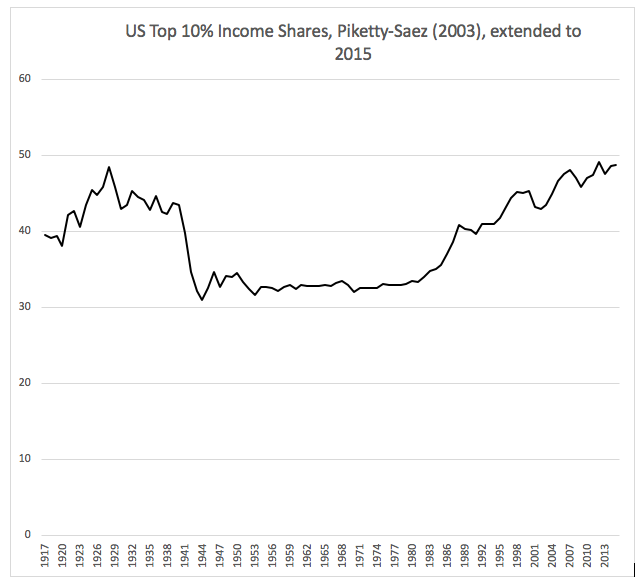

To bolster this argument, academics and political figures alike enlist the influential statistical work of economists Thomas Piketty and Emmanuel Saez, who in 2003 produced a century-long estimate of the top 1% and 10% income shares for the United States (Figure 1). The Piketty-Saez argument is relatively straightforward and attempts to link income distributions to tax rates over time. They show a period of relatively low inequality lasting from about World War II until the 1970s that is bookended by two periods of high inequality: the tail end of the “Gilded Age” that allegedly lasted until the Great Depression, and a post-1980 rebound.

Tax rates occupy center stage in this narrative, as the mid-century low inequality “trough” coincided with a period of extremely high progressive tax rates. From 1946 to 1963, for example, the marginal tax rate on income over $200,000 was an astounding 91%. While these extreme rates applied to the ultra-wealthy, even upper middle class earners faced a stiff penalty from the taxman. For example, earnings above $16,000 (about $137,000 today) for a single filer in 1960 faced a top marginal rate of a whopping 50%.

This all changed in the wake of the Reagan tax reforms of the 1980s and subsequent revisions that have held the top marginal income tax rate below 40% since 1987. Naturally, many inequality theorists blame the post-1980 rebound in income concentrations on this shift in the way we approach taxes on the rich. Their implied solution invariably calls for a resumption of the severe progressive tax rate structure of the mid-century.

There’s a problem with this way of thinking about taxes though, and it cuts to the core of the way inequality is measured. Piketty-Saez and other studies calculate the size of top income shares by using tax-generated data from the IRS. Conceptually, this approach may be the closest we can come to capturing an accurate picture of income earnings in a given year. But it is also an empirically treacherous way to track changing inequality over time because income reporting on tax forms is itself highly sensitive to changes in the tax code.

Effective vs. Statutory

Between 1913 and the present day, the tax laws of the United States have been affected by over 40 major pieces of legislation and numerous other smaller changes. Most taxpayers plan the way they structure their income to minimize their burden to Uncle Sam, so it’s not surprising to see that reported income changes in response to modifications to tax laws and tax rates.

For example, you may donate to charities for the tax write-off benefit, take advantage of a Health Savings Account through your employer to lessen your tax burden, or choose to invest in tax-exempt municipal bonds specifically because of that benefit. You may also change your tax planning strategy for each to soften the blow of a federal tax hike, or cut back on your use of tax incentives in the years after a tax cut. In some cases (1944, 1954, and 1986) the IRS itself has changed its own accounting practices in ways that affect income reporting.

These factors combine to make reported income extremely difficult to measure over long periods of time, as they require several complex adjustments to the “raw” IRS data to account for changes. And since income inequality is also estimated using the same IRS data, the depicted results are extremely sensitive to how tax code changes are handled.

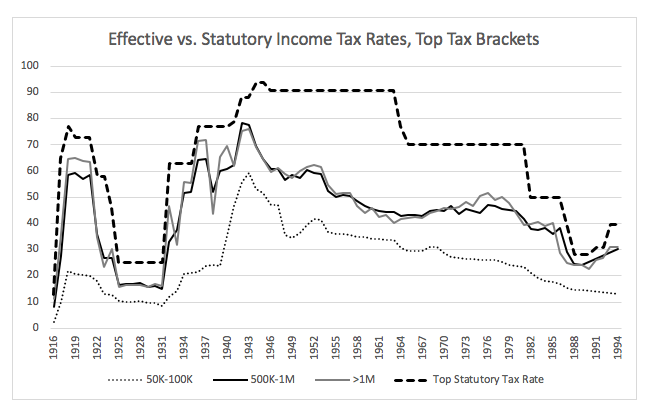

Turning to the claimed link between inequality reduction and high progressive tax rates, an interesting complication emerges at the mid-century trough. While the top marginal rates of 1945-1980 were notoriously high in the statute books, almost nobody in the applicable income brackets actually paid those rates.

Instead, they rationally took advantage of a high number of intentional mid-century tax deductions, exemptions, incentives, and carve-outs to reduce their burden. Incidentally, these legal incentives were a much larger feature of the tax system at the mid-century trough than they are today, owing to a tax code restructuring that closed and consolidated several loopholes in exchange for the Reagan era rate cuts of 1986.

Figure 2 shows this pattern in action by comparing the statutory tax rate on the $1 million income bracket against the actual effective tax rate those same earners paid. (Note: In this figure I hold tax brackets constant to correspond to those used in IRS statistical reporting. The IRS did not begin adjusting brackets for inflation until the late 1970s. A similar pattern may be seen in a different approach that accounts for inflation instead of tax bracket consistency, using data generated from Piketty & Saez’s own work).

Notice that until World War II, the effective rate is slightly lower than the top statutory rate, which we would expect, given that top marginal rates only kick in above a designated income level. but it also closely tracks that rate. The same is true after 1980. But between roughly World War II and 1980, a very different pattern exists: a large gap develops between the top statutory tax rate and the effective tax rate that earners in the same brackets are actually paying. In 1960 for example, an earner in the $1 million bracket paid an effective tax rate of only 46%. Note also that lower tax brackets still qualifying as “wealthy” all display a similar pattern at the mid-century mark.

The posited link between the inequality reduction and highly progressive income tax rates is severely exaggerated. While patterns in income earning are certainly susceptible to taxation, including the extremely high progressive advocated by some inequality theorists, the real story behind inequality measurement is how taxpayers respond to changes in the tax code in order to minimize their liabilities – and legally so.

Far from a vindication, the mid-20th century experience of the United States actually points to the futility of using confiscatory tax rates to counteract inequality.

Phillip W. Magness

Phillip W. Magness works at the Independent Institute. He was formerly the Senior Research Faculty and F.A. Hayek Chair in Economics and Economic History at the American Institute for Economic Research. He holds a PhD and MPP from George Mason University’s School of Public Policy, and a BA from the University of St. Thomas (Houston). Prior to joining AIER, Dr. Magness spent over a decade teaching public policy, economics, and international trade at institutions including American University, George Mason University, and Berry College. Magness’s work encompasses the economic history of the United States and Atlantic world, with specializations in the economic dimensions of slavery and racial discrimination, the history of taxation, and measurements of economic inequality over time. He also maintains an active research interest in higher education policy and the history of economic thought. His work has appeared in scholarly outlets including the Journal of Political Economy, the Economic Journal, Economic Inquiry, and the Journal of Business Ethics. In addition to his scholarship, Magness’s popular writings have appeared in numerous venues including the Wall Street Journal, the New York Times, Newsweek, Politico, Reason, National Review, and the Chronicle of Higher Education.