Centralized, Decentralized, and Distributed Payment Mechanisms

I often hear people describe bitcoin as a decentralized payment system. And they are in good company. For example, Erik Voorhees has said that “one of Bitcoin’s most important features—and perhaps its true core innovation—is its decentralized structure.”

Voorhees is a smart guy. But I feel compelled to push back. Dividing the world into “centralized” and “decentralized” obscures important features of the bitcoin protocol. A more sophisticated lexicon would leave scope for “distributed” processes.

To understand the differences, let’s consider some familiar payment mechanisms.

Centralized

A bank functions as a centralized clearinghouse. Suppose we are both customers of the same bank. When I write you a check or swipe my debit card at your merchant terminal, our bank debits my account and credits yours. The bank—a central entity—processes the transaction. Indeed, we might depict all of the transactions being made between a bank’s customers as passing through a single, centralized node (i.e., the bank) as in Figure 1 below.

Figure 1. Centralized Network

Suppose we are not customers of the same bank. In this case, there is a transaction between our respective banks. In the U.S., these transactions are processed through Fedwire or the Clearing House Interbank Payment System (CHIPS)—centralized entities that debit one bank’s account and credit another’s when an interbank payment is made.

Decentralized

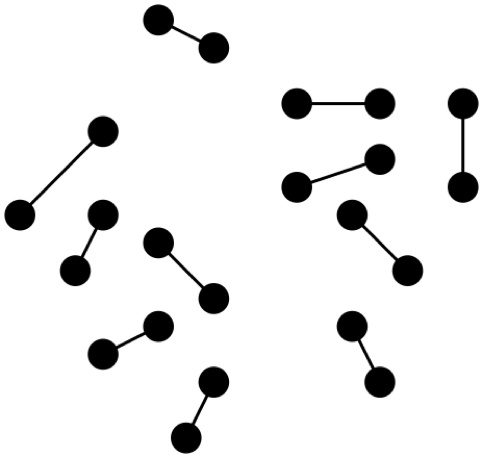

Cash transactions are decentralized—that is, they are processed by the parties to the transaction without reliance on some trusted third party. Suppose I pay you $20 in cash. When I hand over the $20, my cash account is debited. When you receive the $20, your cash account is credited. No central entity is required to processes cash transactions because cash balances are physical. Indeed, no one else even needs to know that the transaction between us occurred. Hence, we might depict all of the cash transactions being made between the respective parties (i.e. individuals) as in Figure 2 below. There is no central node and a transaction is only observed by the parties to the transaction.

Figure 2. Decentralized Network

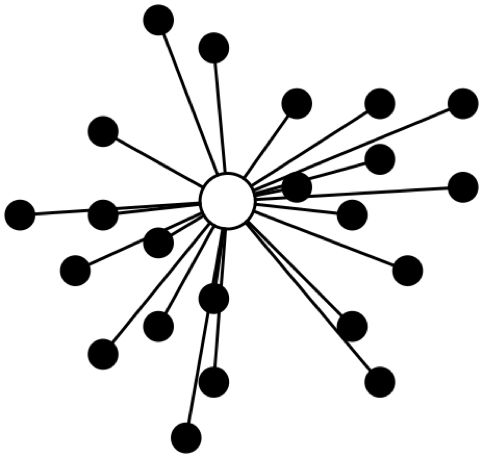

Distributed

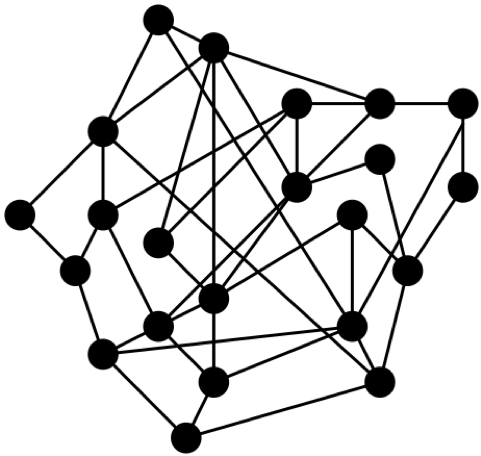

Bitcoin is not centralized. It doesn’t rely on a trusted third-party to process transactions. But bitcoin is not decentralized either. Instead, bitcoin transactions are processed over a distributed network.

When I send you a balance of bitcoin, the transaction is grouped together with others into a block of transactions. Computers running the bitcoin protocol then race to update a shared ledger, known as the blockchain, to account for the new block of transactions. The updated blockchain reflects the fact that my account has been debited and your account has been credited. We might depict all of the bitcoin transactions being made on the network as in Figure 3 below. There is no central node. Transactions are processed by the network. As a result, all transactions are observable to the entire network—not just the parties to the transactions. Hence, the users on the network are connected.

Figure 3. Distributed Network

William J. Luther

William J. Luther is the Director of AIER’s Sound Money Project and an Associate Professor of Economics at Florida Atlantic University. His research focuses primarily on questions of currency acceptance. He has published articles in leading scholarly journals, including Journal of Economic Behavior & Organization, Economic Inquiry, Journal of Institutional Economics, Public Choice, and Quarterly Review of Economics and Finance. His popular writings have appeared in The Economist, Forbes, and U.S. News & World Report. His work has been featured by major media outlets, including NPR, Wall Street Journal, The Guardian, TIME Magazine, National Review, Fox Nation, and VICE News. Luther earned his M.A. and Ph.D. in Economics at George Mason University and his B.A. in Economics at Capital University. He was an AIER Summer Fellowship Program participant in 2010 and 2011.