Can the Fed Manage the Excess?

The Federal Reserve began an unprecedented experiment in 2008 under the moniker of quantitative easing. By using its acronym, QE, we might forget that it means that the Federal Reserve is creating large quantities of base money. In fact, it has created so much base money that it has found itself between the devil and the deep sea: choosing whether to let the money circulate in the economy, thereby pushing up prices, or to remove this money quickly, thereby potentially creating a deflationary spiral.

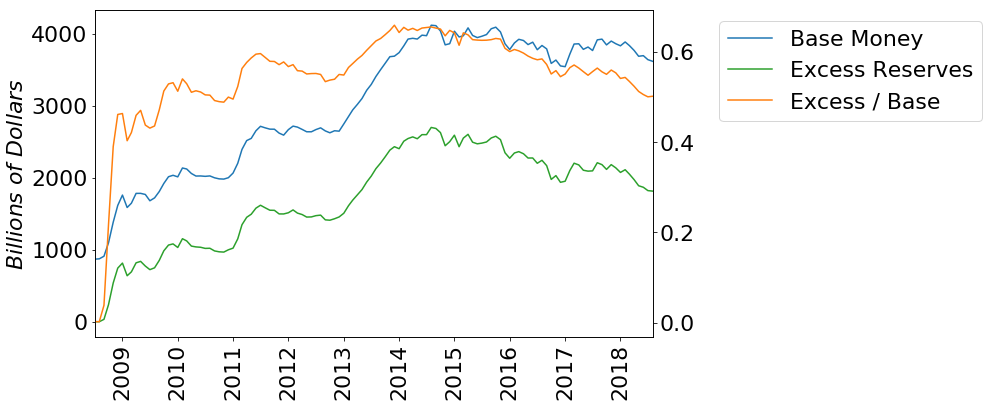

The Fed expanded the quantity of base money in 2008. This was the beginning of a series of monetary expansions that would see the quantity of base money increase by nearly 400 percent within six years. Many have been surprised that the result has not been hyperinflation. How could the quantity of base money increase by nearly five times without fomenting hyperinflation?

During the crisis, the Federal Reserve initiated a second unprecedented policy: payment of interest on excess reserves. Before the 2008 crisis, the Federal Reserve paid interest only on required reserves, those minimum reserves that banks must hold to meet legal requirements. The Federal Reserve began paying interest on excess reserves on October 1, 2008, shortly after the first round of QE began. It has maintained this position since, providing a return more competitive than the rate for overnight lending.

The Federal Reserve is paying banks not to lend. This money could otherwise be loaned to entrepreneurs seeking to profit in the market. Banks have responded by holding over half of the monetary base as excess reserves at the Federal Reserve. Entrepreneurs, who would have received a loan absent this intervention, are no longer able to borrow from these banks.

The payment of interest on excess reserves has decreased the appetite of banks for risk. But as economic activity has begun to show sustained improvement, the Federal Reserve has treaded carefully to maintain a moderate level of inflation. Expectation of economic growth has led banks to draw down the level of their excess reserves and is now putting upward pressure on wages and prices. The Federal Reserve has responded by increasing the rate of interest paid on excess reserves to compete with high-yielding opportunities in the market.

Since the height of QE, the response of banks has been to reduce their holdings of excess reserves at the Federal Reserve, both as an absolute magnitude and as a proportion of the total quantity of base money. On net, money is entering the economy. Rising rates paid on excess reserves seem only to be slowing this trend. Inflation, as measured by the GDP deflator, was 2.47 percent in the second quarter. This is the highest it has been since the 2008 crisis. A rate of 2 to 3 percent is relatively moderate; however, the Federal Reserve may struggle to maintain this low rate of inflation as banks begin investing these funds in a growing market. It must either let the money begin to enter the economy, leading to higher inflation and perhaps an artificial boom, or raise the rate paid on excess reserves, thereby preventing the money from entering the economy. It is unclear which outcome would be worse. Neither is good, but the latter outcome would move our monetary system toward central planning and away from the rule of law.

The Federal Reserve seems interested in preventing an extreme macroeconomic event. However, given the stakes and the uncertainty created by its management of the money stock, a clear path forward, even if it is inflationary, may be superior to manipulation of the rate of interest. Given that half of the base money in the United States is held as excess reserves, the cessation of payment of interest would lead to at least a doubling in prices. Announcement of future policy ahead of time by the Federal Reserve could reduce malinvestment and volatility that would result from such an inflation.

Further, instead of raising the rate paid on excess reserves, the Federal Reserve could announce a timeline in which it lowers the rate until it reaches zero, thus allowing money to enter the market gradually. At that time, it could return to prominence the policy of targeting the federal funds rate through open market operations.

James L. Caton

James L. Caton is an Assistant Professor in the Department of Agribusiness and Applied Economics and a Fellow at the Center for the Study of Public Choice and Private Enterprise at North Dakota State University. His research interests include agent-based simulation and monetary theories of macroeconomic fluctuation. He has published articles in scholarly journals, including The Southern Economic Journal, the Journal of Entrepreneurship and Public Policy, and the Journal of Artificial Societies and Social Simulation. He is also the co-editor of Macroeconomics, a two-volume set of essays and primary sources in classical and modern macroeconomic thought. Caton earned his Ph.D. in Economics from George Mason University, his M.A. in Economics from San Jose State University, and his B.A. in History from Humboldt State University.