Business Confidence, Big and Small, 2004-present

As part of a larger study, I’ve generated time series of small and big business confidence since 2004. The larger study tracks business confidence since 1929, including business confidence during the Great Depression and other tumultuous times. The larger study involves ferreting out long forgotten surveys of business and using the surveys to form a consistent time series. The present study is much simpler: to average and then compare the finding of three ongoing surveys each of small and big business.

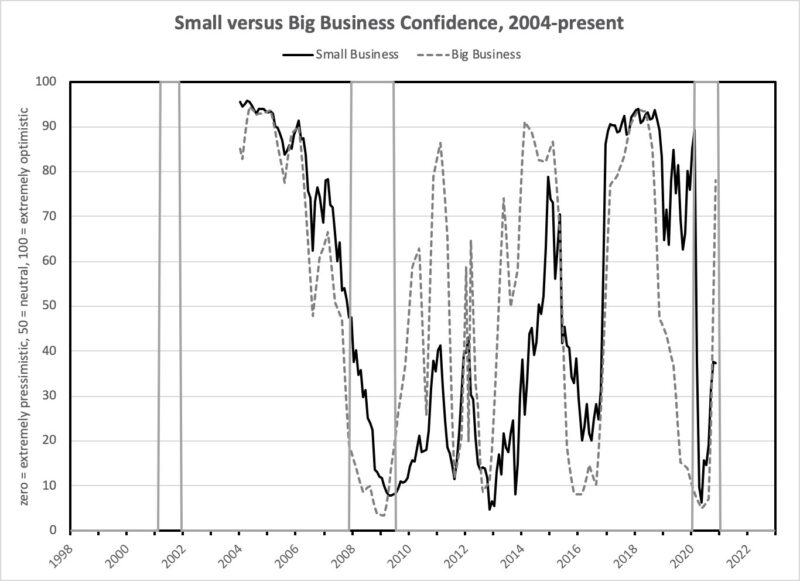

You may have heard of one or more of them. For small business: the National Federation of Independent Business survey, the Wells Fargo/Gallup survey of small business, and the Wall Street Journal/Vistage survey. For big business: the Conference Board CEO survey, the Business Roundtable CEO survey, and the recently ended PriceWaterhouseCoopers Trendsetter Barometer. These surveys are to varying degrees copyright protected and, so, their individual data will not be revealed here. Besides, my concern is not with any particular survey.

In these and similar surveys of other businesses and of consumers, respondents are asked about their assessment of the current situation, and their outlook and plans concerning the near future.

From the answers to questions such as “Are you planning a net increase in employees?” and “Are you budgeting an increase in marketing and promotion?”, we infer business willingness and ability to hire, invest, expand production, and in other ways to take what they perceive to be prudent risks.

From one to another survey, the actual questions differ. In addition, the scales employed by the survey takers vary; e.g., in one, 50 may be nominally neutral, and in another 100, or else an index is constructed that refers to an essentially arbitrarily chosen base year. What I’ve done to deal with this mess is calculate the cumulative probability, assuming the underlying data of each survey is normally distributed. It’s a function in Excel, so this wasn’t a big deal. Then, I averaged the three cumulative probabilities for each of small and big business. The results are shown on the accompanying chart.

While there is maybe an overall similarity in the behavior of small and big business confidence over time, there are some notable differences. I count four:

- 2010-11 – when big business confidence rebounded sharply from the recession associated with the Financial Crisis of 2008; and small business confidence lagged.

- 2013-14 – when big business confidence rebounded sharply from a mere slowdown of the U.S. economy in 2012; and, again, small business lagged.

- 2018-19 – when big business confidence fell prior to the recession associated with the shutdown of the economy; and, small business confidence remained high.

- late 2020 – when big business confidence fully rebounded; and small business only partially rebounded.

Any number of reasons might be cited to explain these differences. Back in 2009 and 2010, the TARP, the stimulus, quantitative easing and expanding the Fed’s balance sheet seemed predicated on “too big to [be allowed to] fail.” Money was easy for some, but credit wasn’t available for many. The bigs – like GM and Chrysler – got bailed out; while the smalls got the shaft. Subsidies for alternative energy were big money-makers for GE and other well-connected businesses, while electricity bills went up.

An alternative explanation might posit that the bigs have better ability to forecast and, so, can see the economy turning up or turning down more quickly. This alternative explanation kind of flips the narrative about small business being the engine of the American economy. At least with respect to the business cycle, the bigs move first and the smalls follow.

I have looked at other groupings of business; e.g., surveys of people in finance, and surveys of people in production. The other groupings don’t show meaningful differences. But, between small business versus big business, there are real differences.

Clifford F. Thies

Clifford F. Thies is a Professor of Economics and Finance at Shenandoah University, He is the author, co-author, contributor and editor of more than a hundred books, encyclopedia entries and articles in scholarly journals.

He is a member of the editorial board of the Journal of Private Enterprise and is a former Bradley Resident Scholar at the Heritage Foundation. He is a past president of the faculty senates of Shenandoah University and the University of Baltimore. He also served in the U.S. Army and the Army Reserve.