Bitcoin as a Novel Financial Game

The St. Louis Federal Reserve’s Christine Smith recently published a post on the similarities between Bitcoin and fiat money:

Economists Aleksander Berentsen and Fabian Schär explained in a recent St. Louis Fed Review article that bitcoin units have no intrinsic value. In economic terms, something lacking intrinsic value means it has no value of its own. But as the authors noted, “[s]tate monopoly currencies, such as the U.S. dollar, the euro, and the Swiss franc, have no intrinsic value either.”

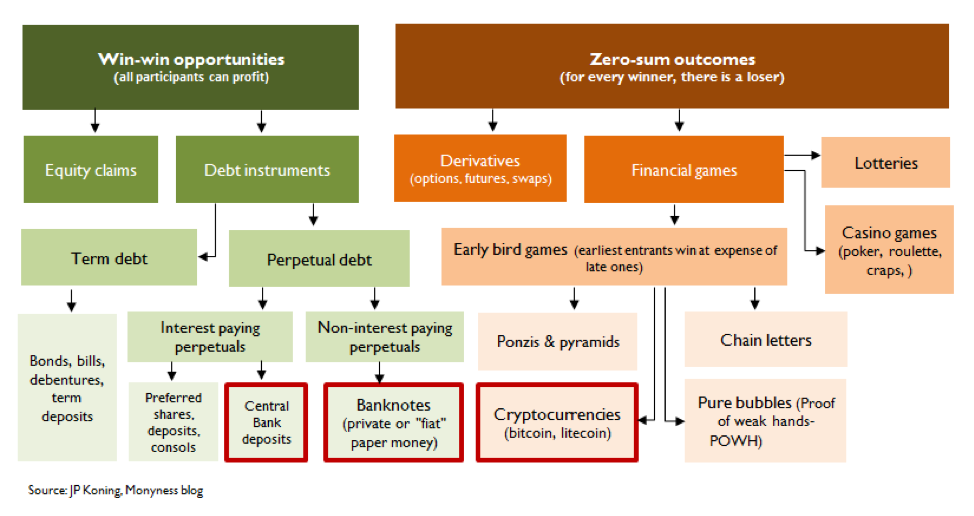

If both bitcoins and national currencies have no intrinsic value, then perhaps they are the same sort of financial instrument, or at least cousins. But I think this is wrong. Below I’ve mapped out a taxonomy of financial assets showing how Bitcoin and fiat money are categorized. Bitcoin and fiat money aren’t even cousins; they’re on entirely different branches of the family tree.

Figure: Classifying Bitcoin and fiat money

Let’s start with banknotes. Banknotes are a type of perpetual debt that, like deposits or consols, has no maturity date. Debt is different from equity in that its owners have first dibs on the issuer’s income. The return on debt is fixed since debt owners do not get to participate in any of the issuer’s upside — all of the residual profits flow through to equity holders. When things turn sour and the issuing institution goes bankrupt, debt claimants have a prior claim on whatever assets remain.

Banknotes are a special type of perpetual debt because, unlike consols, they don’t pay interest. Central banks do issue an interest-paying form of perpetual debt: deposits. Unlike the case of banknotes, however, only commercial banks can hold central bank deposits.

Stocks, banknotes, consols, bonds, and deposits are all win-win opportunities. For an owner of any of these instruments to enjoy a return, another owner doesn’t need to lose out. As long as the issuing institution is generating a profit, everyone enjoys a return.

Win-win games can be contrasted with zero-sum games. In a zero-sum game, the only way to come out ahead is if someone else loses. Derivatives are a good example of a zero-sum game. A futures contract is a bet between two people on the future price of a commodity like corn, one party being obligated to pay the other as the price diverges from what it was when the contract was entered into.

On the zero-sum branch is the subcategory of financial games, which includes poker and lotteries. Poker is a zero-sum game because one player’s winning hand is another player’s losing hand. As for lotteries, a lottery number can only be a winner because all other numbers are losers.

Bitcoin is a specific type of financial game, an early-bird game. This group also includes Ponzi games, pyramids, and chain letters. The payout decision for an early-bird game is based on entrance order, with early adopters winning at the expense of late adopters. In the same way that a Ponzi game comes to an end if no new participants appear, if no new buyers of bitcoins ever emerge, then current owners will find that their tokens are worth zero.

I’m not trying to denigrate Bitcoin by putting it in the category of financial game. As long as they are played in moderation, financial games are a socially valuable form of entertainment, much like movies or sports. Let’s face it, Bitcoin is fun. Day or night, players love checking on its frenetic price. Bitcoin introduces some neat features to the financial-game space. Firstly, everyone in the world can play it (i.e., it is censorship-resistant). Secondly, the task of managing the game has been decentralized. Lastly, Bitcoin’s rules are automated by code and fully auditable.

Unlike Bitcoin, most financial games are run by a centralized administrator and may be opaque and difficult to audit. In certain scenarios, this setup can be dangerous. Because early-bird games like Ponzis and chain letters have been driven underground by the authorities, the people who administer them lack accountability and will often turn out to be scam artists. As I wrote here, Bitcoin has the virtue of providing early-bird-game players with a relatively transparent and trustworthy alternative.

Which gets us to the issue of Bitcoin’s energy consumption. According to David Gerard, Bitcoin currently uses 0.1 percent of world electricity production, soon to be 0.5 percent. That’s a lot. The reason Bitcoin hogs so much electricity is that it decentralizes the task of managing the game to thousands of competing croupiers. Coordinating this multitude of croupiers requires an energy-intensive process — proof of work — which Gerard refers to as an “ugly kludge of a hack.”

While financial games like lotteries and casinos are centralized, I suppose it would be possible to decentralize them in the same way that Bitcoin is decentralized. But this would make them more expensive to run. The only reason for adopting such a costly way to manage a financial game is to evade authorities, say because the lottery or casino is illegal. An illegal game run from a single central server would be easy for the authorities to shut down, but when it is maintained on thousands of independent computers across the globe, the game becomes much more resistant to being shut down. So while a centralized version of Bitcoin would be significantly cheaper to run, it would be an easy target for authorities on the lookout for illegal early-bird games.

What about the motivating principle behind Bitcoin — to function as electronic cash — you may ask? One of the greatest tricks Satoshi Nakamoto, the creator of Bitcoin, ever played was convincing everyone that his invention was just like a banknote, when it was actually a novel type of zero-sum financial game. Zero-sum games are just too volatile to ever become the basis of a generally accepted medium of exchange. But even if it never gains much currency, that doesn’t mean Bitcoin isn’t without merit. If we owe the person who invented poker a debt of gratitude, maybe we owe Satoshi Nakamoto the same.

J.P. Koning

J.P. Koning is a financial writer and blogger with interests in monetary economics, economic history, finance, and fintech. He has worked as an equity researcher at a Canadian brokerage firm and a financial writer and publisher at a large Canadian bank. More recently, he has written several papers for R3, a distributed ledger company, on the topics of central bank cryptocurrency and cross border payments. He founded the popular blog Moneyness in 2012. He designs economics and financial wallcharts at Financial Graph & Art.

Koning earned his B.A. in Economics from McGill University.