Ask the Economist: Hours Worked and Wage Growth

Kevin C. Donnelly asks: “Where does the data suggest the average American is in terms of work hours a week and wage growth less inflation, and what does that mean for long-run trends?”

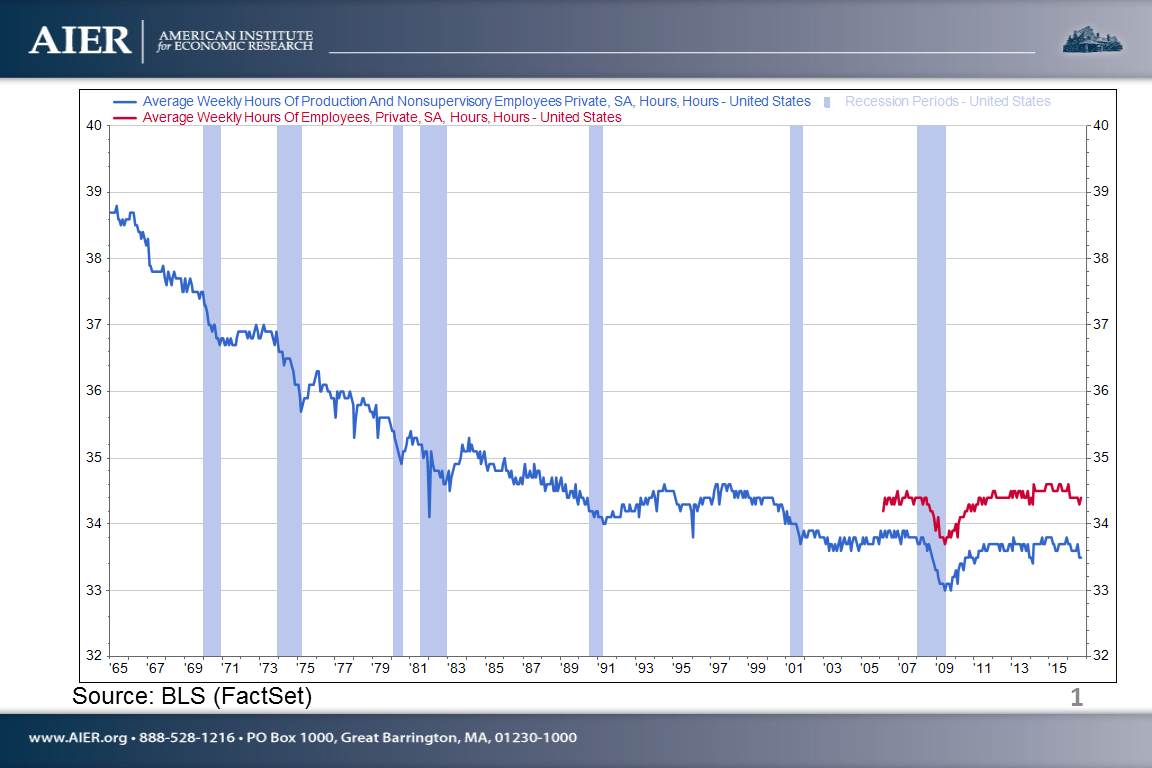

Thanks for the question. For hours worked, there has been a long-term declining trend in the average workweek for production and nonsupervisory workers. Chart 1 shows that the average workweek for this group has fallen from just under 39 hours in 1965 to about 33.5 hours currently. For all private sector employees, the average workweek is about 1 hour longer (historical data for this series is only available back to 2006). In both cases, the length of the workweek is up from the lows following the Great Recession.

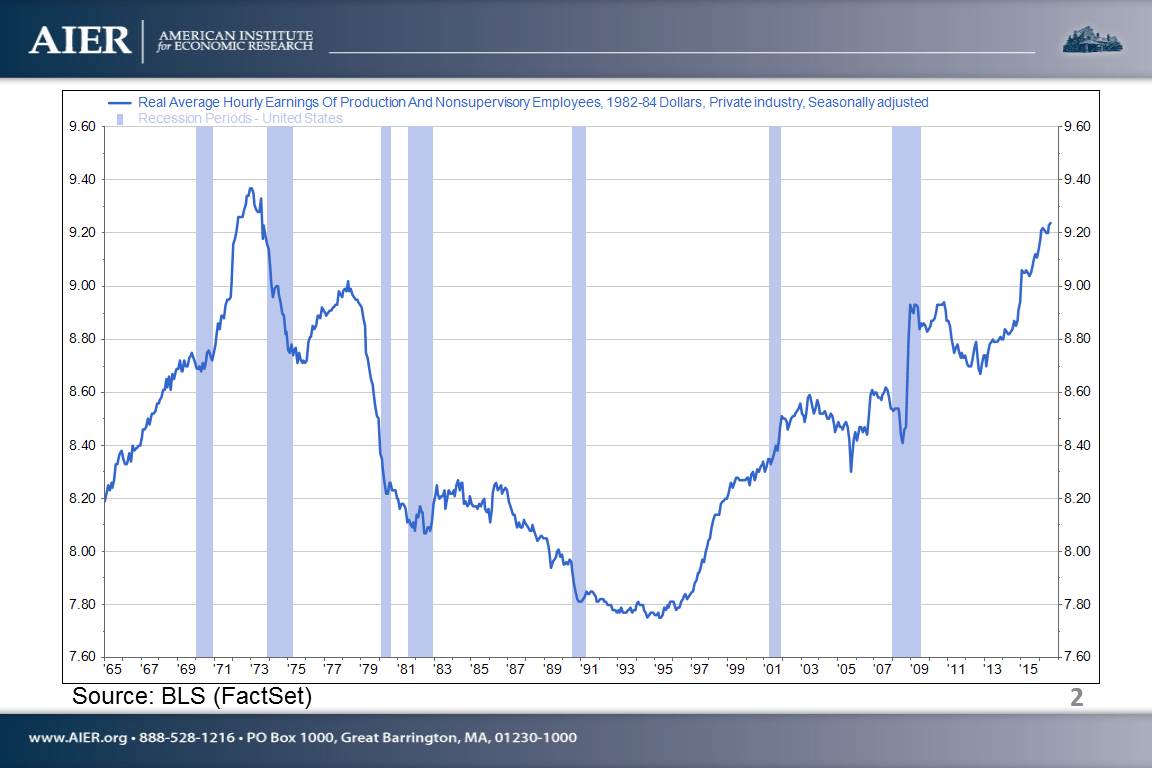

Hourly wages adjusted for inflation (real hourly wages) have actually been rising more rapidly recently thanks to a combination of nominal wage growth and slow price increases. Chart 2 shows that real average hourly earnings are at the highest level since 1973!

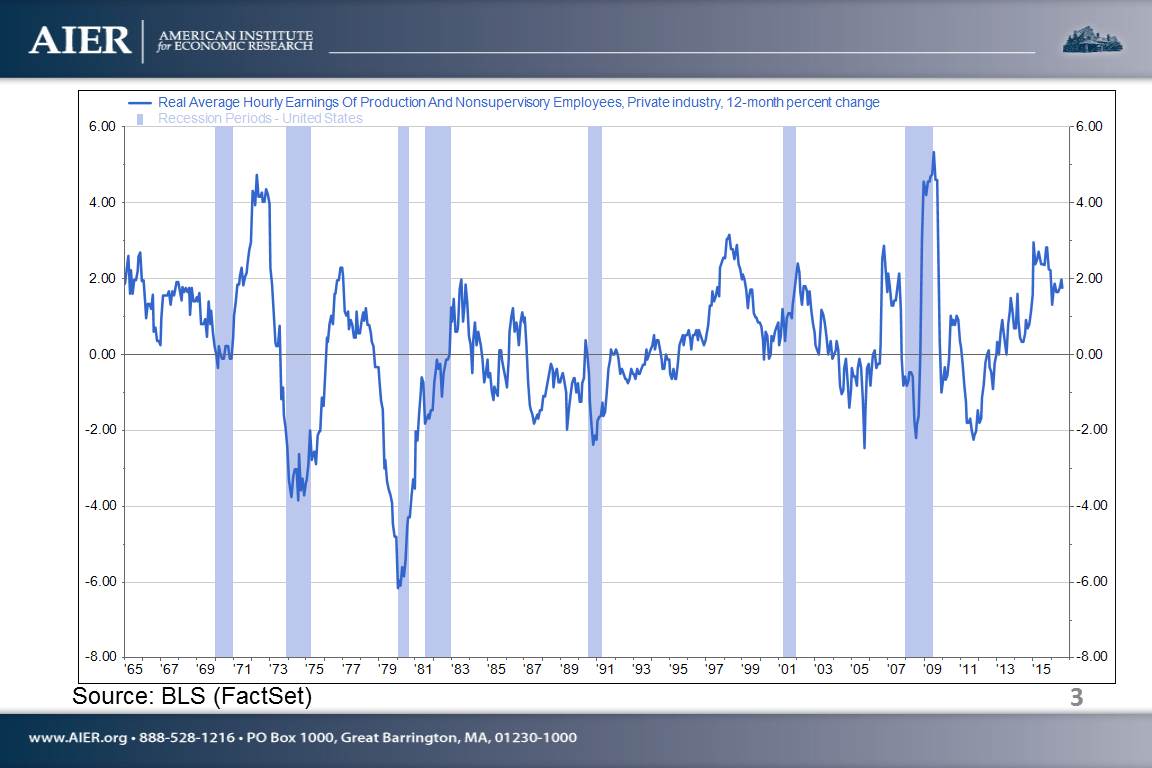

Chart 3 shows that the pace of growth is currently around 2 percent, which is near the highest rates of growth over the past 50 years.

In general, a faster pace of growth in real average hourly earnings is good for consumers. However, faster wage growth means higher labor costs for employers. If the faster wage growth is not offset by faster productivity growth, then profit margins and profits may come under pressure, and that may be bad for investors.

To submit a question about the economy for a future edition of Ask the Economist, send an email to Aaron Nathans at aaron.nathans@aier.org.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.