As the U.S. Government Grows, American Prosperity Slows

Myopic accounts of American economic performance are common today, permitting political partisans to cite whatever period they wish to prove any case they want. Republicans today insist that President Trump’s policies have revitalized U.S. economic growth after years of supposed stagnation under President Obama, while Democrats say Obama’s policies started the recent revival, reversing the disastrous “Great Recession” of 2008-09 which was caused by President Bush’s policies. If you pick your own period, you can “prove” almost anything.

Let’s reject partisan analysis for a moment, look back 150 years (from the end of the Civil War), ignore whatever party or president was dominant, and try to discern a relationship between the size, scope and power of the U.S. federal government and America’s economic growth rate. Let’s consider U.S. federal spending, tax revenues and debt as a share of GDP and use the longest, most reliable time series for output: the U.S. Industrial Production Index (IPI). Unlike GDP, the IPI excludes government outlays, so it’s a purer measure of real U.S. output. Avoiding arbitrary period selection, let’s also use three, sequential 50-year periods: 1868-1917, 1918-1967, and 1968-2018.

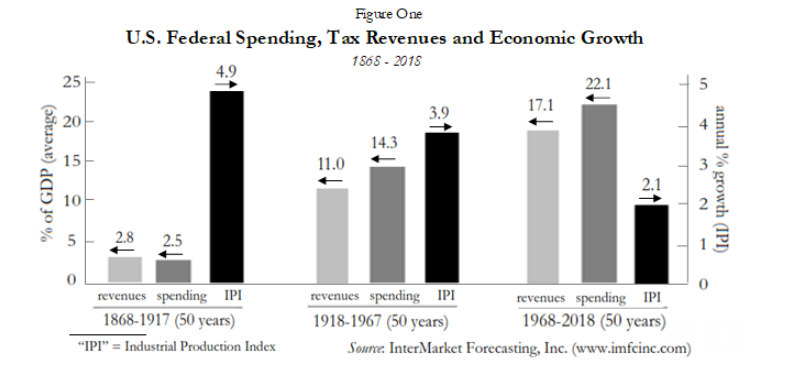

Figure One illustrates how economic growth has been faster when the federal government has been smaller (relative to GDP) – and vice versa. From 1868 to 1917 (the so-called “Gilded Age”) the IPI grew at a compounded annual rate of 4.9%, while U.S. federal outlays and revenues averaged less than 3% of GDP. In contrast, since 1968 IPI has grown by only 2.1% per annum, while U.S. outlays and revenues have averaged 22.1% and 17.1% of GDP, respectively. Far more federal spending and taxing occurred during the intermediate 50 years (1918-1967) relative to the Gilded Age, but even though those years including two world wars and the start of the New Deal, even greater spending and taxing has occurred since 1968.

If there’s any relationship here, is it correlation or causation? Suppose it’s causal. Is it more likely that slower economic growth boosts government outlays and taxes or that a larger government diversion of private-sector resources slows the economic growth rate? The latter.

How might U.S. federal debt relate to the ever-rising share of U.S. federal spending and taxing? In any unrestrained democracy, devoid as it is of enforceable monetary or fiscal rules, it pays politicians, electorally and financially, to spend more (as Democrats prefer) and tax less (as Republicans prefer). That means it pays politicians to adopt chronic deficit-spending, whether in good economic times or bad – which means it pays them to fund their outlays more by debt and less by taxes – which means it pays them to generate an ever-rising share of national debt to GDP (while claiming they’re “very concerned” about it). To the extent this public profligacy proves costly or precarious, the unrestrained democratic state pressures its central bank to “monetize” public debt and facilitate artificially low interest rates.

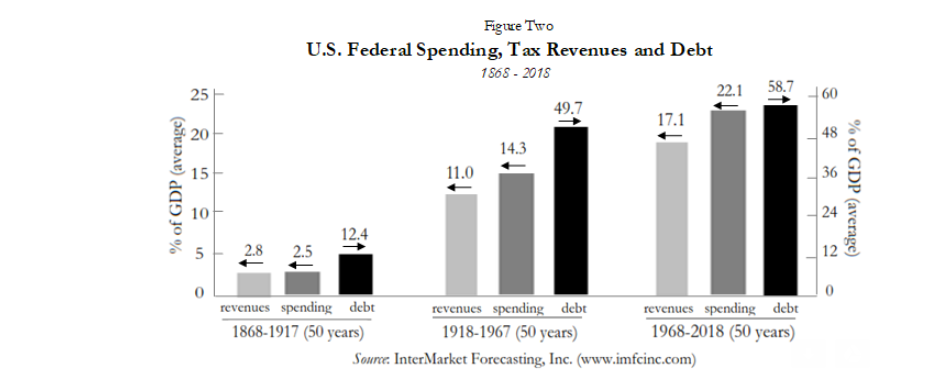

Figure Two illustrates the point. U.S. federal debt, now $22.3 trillion (105% of GDP), has averaged 58.7% of GDP over the past half century (1968-2018), up from just 49.7% of GDP in the intermediate years (1918-1967) and only 12.4% of GDP from 1868 to 1917. When the federal government was smaller it was easier to fully fund its outlays by taxes; indeed, from 1868 to 1917, tax revenues exceeded outlays, on average, even as both were a small share of GDP. In contrast, since 1968, with much larger spending relative to GDP, the average gap between spending and taxing has been 5 % points (22.1% versus 17.1%). U.S. deficit spending has occurred in 90% of the fiscal years since 1968, versus only 26% of the years 1868-1918.

These are non-partisan facts, but I acknowledge that my analysis presumes economic growth is a good thing, a conclusion necessitating a separate, normative argument (which also must be fact-based). I also concede that many people today don’t prioritize prosperity and for various reasons prefer high federal spending, taxing and borrowing relative to national income; if so, my analysis says that they shouldn’t be so surprised when their preference causes less-robust rates of economic growth.

Finally, I admit that still others, who prefer less economic growth, no growth or even “de-growth,” can use this same data to push for an ever-increasing proportion of federal spending and taxing. But those among us who endorse faster economic growth and greater prosperity should, at least, know these important facts.

Richard M. Salsman

AIER Senior Fellow Richard M. Salsman is president of InterMarket Forecasting, Inc. and a visiting assistant professor of political economy at Duke University. Previously he was an economist at Wainwright Economics, Inc. and a banker at the Bank of New York and Citibank. Dr. Salsman has authored the books Gold and Liberty (1995), The Collapse of Deposit Insurance and the Case for Abolition (1993) and Breaking the Banks: Central Banking Problems and Free Banking Solutions (1990), all published by AIER, and The Political Economy of Public Debt: Three Centuries of Theory and Evidence (2017). His fifth book – Where Have all the Capitalists Gone? Essays in Moral Political Economy – was published by AIER in 2021.

Dr. Salsman earned a B.A. in economics from Bowdoin College (1981), an M.A. in economics from New York University (1988), and a Ph.D. in political economy from Duke University (2012). His personal website is https://richardsalsman.com/