A Fate Worse than Hyperinflation

Fiscal restraint is gone. Supported by central bankers who have developed a set of policy tools whose impact is practically imperceptible, year after year the national debt continues to grow.

We no longer live in an era where easy money generates inflation. Such a world might be safer than the one we are in. Instead, easy money generates risk free profits for banks and growing federal deficits. Worst of all, the public is unaware. If we continue on this path, we risk suffering a devil much worse than the double-digit inflation of several decades past.

With the 2008 Crisis, the Federal Reserve adopted a new set of policy tools about which I have been writing over the last year. In response to the 2008 crisis, the Federal Reserve greatly expanded its balance sheet and, in so doing, set a precedent for the central bank to support federal largess. And in response to the current shutdown of the U.S. economy, this year’s federal deficit is expected to be around $3.5 trillion, representing nearly half of this year’s expenditures.

I am not debating whether or not the federal government providing a sort of insurance in the face of the current supply shock is a good or bad idea. The long-run trajectory of federal spending is increasingly unsustainable. The current expansion, even if justified, further entrenches a pattern of negligent behavior practiced by the American legislature.

Growing Fiscal Negligence

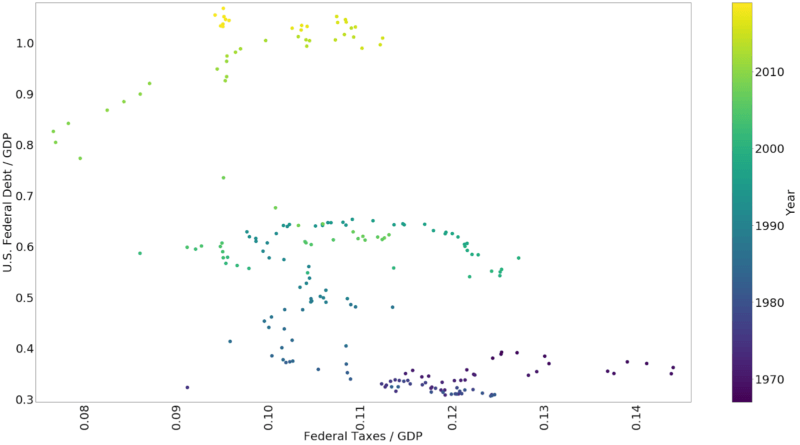

For decades, there was a supposed alliance of ideas consisting of support for lower taxes and lower levels of government spending. The joint influence of these ideas on actual policy has been an article of faith, useful for the campaign trail but not supported by the fiscal data. Lower levels of tax collection have been met with increased indebtedness by the federal government. The current episode will be no exception to this long-run trend.

The political system has developed a formula over the last decade that has only pushed in the direction of further fiscal irresponsibility. Fiscal expansion is not followed by higher taxes or a period of fiscal constraint. It is supported by a central bank that has become increasingly effective at hiding the detrimental effects of this policy. The pain that will accompany a shift toward responsible behavior, whether adopted voluntarily or involuntarily in the case of a day of reckoning, is only increasing.

The central bank is able to support federal spending by money creation without also generating higher prices. To prevent inflation, it pays banks a risk free rate of return not to lend the newly created money. (The Fed also cooperates with the U.S. Treasury to ensure that the quantity of money in circulation remains stable.) Without a signal to the citizen taxpayer in the form of explicitly higher taxes or devaluation of currency, it seems to most observers that we can push happily along, business as usual.

Yesterday was fine, so tomorrow will bring no problems either. Right?

The Road Ahead

There are two possible courses ahead given the nature of monetary policy in the United States. 1) Debt repayment never becomes problematic. This is made possible if the federal government provides incentives in the form of resource transfers to investors. We observe this, for example, with the payment of interest to banks holding excess reserves at the Fed. Or 2) investors lose faith in the ability of the government to repay its debts and, if other incentives cannot sway their concern, these investors will begin demanding compensation for the increased level of risk that they face. This second path would result in higher interest rates that increase the burden of debt repayment by the Federal government.

In the first case, let’s imagine that the central bank is able to support federal borrowing perpetually. As a result, resources are shifted to the federal government and growth in the private sector is limited. The trouble with shifting production to the state is that we cannot expect federal spending to improve the level of welfare generated, in comparison, to improvements that would be achieved by a competitive market. State-supported businesses face looser constraints in terms of profitability.

State support incentivizes continued pursuit of subsidies in lieu of value creation that would otherwise be required for survival in the market. We already see evidence of this effect in the historically low rates of real income growth that have accompanied the new monetary policy regime that provides historically high levels of support for federal spending.

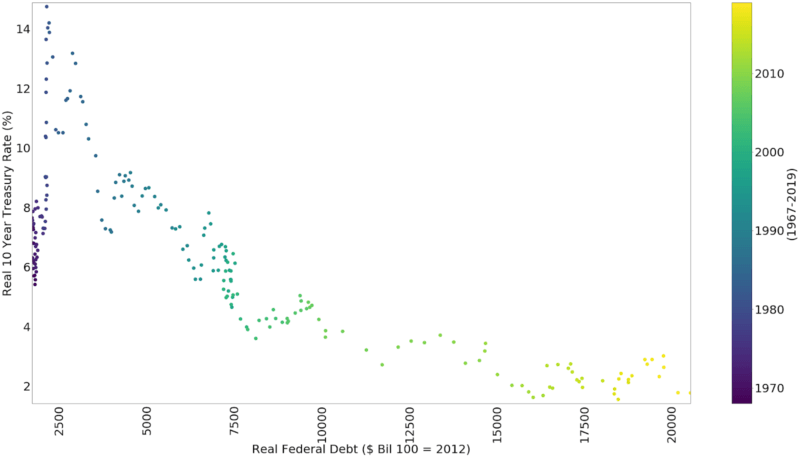

Support for federal borrowing must ultimately translate into lower interest rates. The current level of federal debt has been supported by falling interest rates for the last few decades. If interest rates on U.S. Treasuries begin to increase due to perception of increased risk by investors, the growing burden of repayment will demand that the government cover costs by lowering the level of expenditures or increasing taxes. An increase in rates of a few percent, without an accompanying increase in the tax base, would make containment of the deficit especially difficult to maintain.

There is a third, and unpleasant, alternative: devaluation. The federal government could ease the burden of debt by generating inflation. If the dollar is worth half as much, then the value of the federal debt not protected from inflation would also be cut in half. This would not be without consequence.

The geopolitical implications of fiscal irresponsibility are frightening, to say the least. If investors lose faith in the ability of the federal government to repay its debts, this will lead to lower valuations of the dollar. In the worst case, investors may search for a new currency to mediate international trade. In this case we would likely see a shift in trade blocs and political alliances (though one might hope that in the best case money becomes denationalized).

As federal spending has evidenced little to no restraint over the last decade, and as political rhetoric expressed during the recent primary season has shown little concern for the fiscal situation, to expect a change in posture from the current regime or any soon to follow seems no more than a fanciful imagining.

But we don’t live in a dream. This is real life. The game played by federal actors and financial markets is for keeps. A lack of awareness of the dangers faced in this game by both the public and by politicians leaves the audience of public opinion in a collective yawn in response to discussion of fiscal responsibility. As we await a proactive change in behavior or a day of reckoning, we will have to live with increasing levels of federal control over private activity and lower rates of economic expansion.

James L. Caton

James L. Caton is an Assistant Professor in the Department of Agribusiness and Applied Economics and a Fellow at the Center for the Study of Public Choice and Private Enterprise at North Dakota State University. His research interests include agent-based simulation and monetary theories of macroeconomic fluctuation. He has published articles in scholarly journals, including The Southern Economic Journal, the Journal of Entrepreneurship and Public Policy, and the Journal of Artificial Societies and Social Simulation. He is also the co-editor of Macroeconomics, a two-volume set of essays and primary sources in classical and modern macroeconomic thought. Caton earned his Ph.D. in Economics from George Mason University, his M.A. in Economics from San Jose State University, and his B.A. in History from Humboldt State University.