Massive Job Loss Sends Unemployment Rate to Highest Since the Great Depression

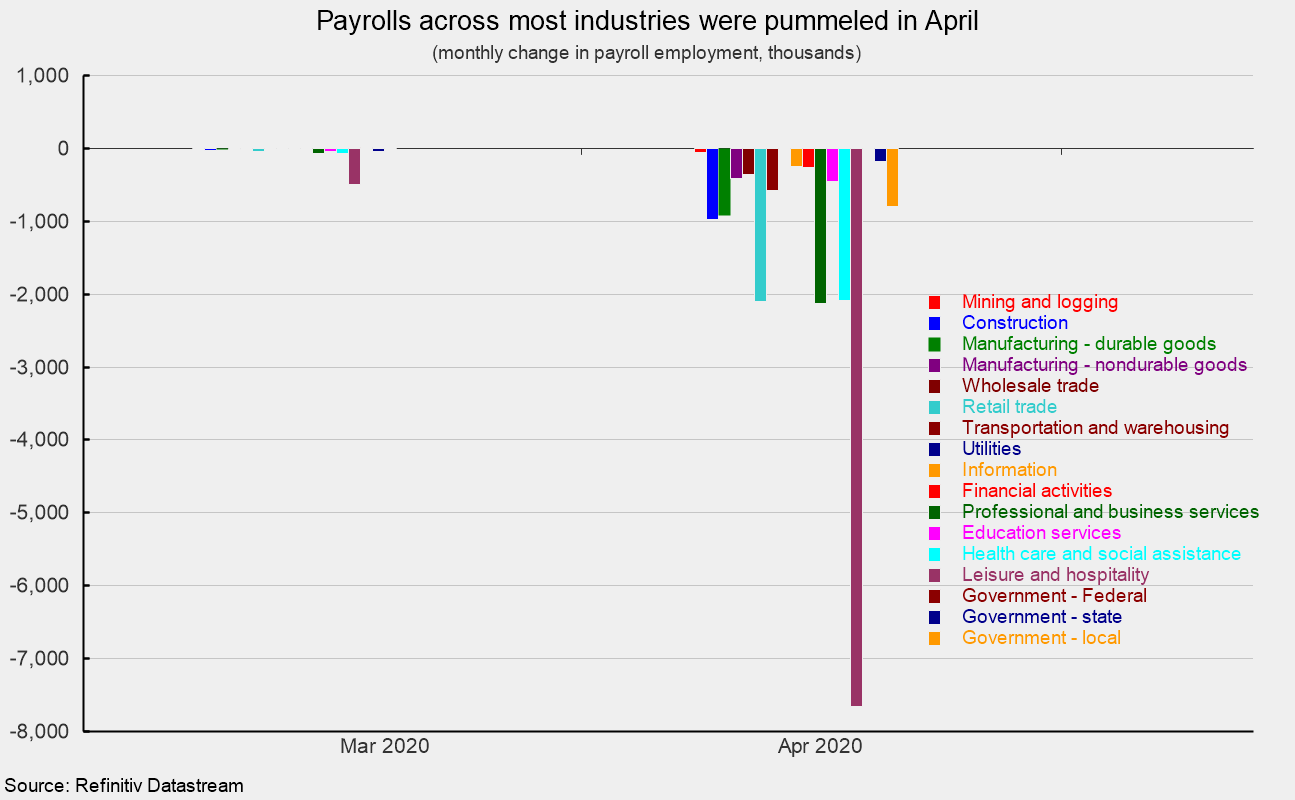

U.S. nonfarm payrolls were slashed by 20.5 million in April, with losses spread across nearly every industry (see first chart). Initial claims for unemployment insurance totaled 33 million over the last seven weeks (some of which are not completely captured in the April employment report) suggesting additional losses in coming months. There were a number of technical issues with the April report including an unusually low response rate from the household survey portion and improper coding of some classifications. While accuracy may be somewhat subpar, the interpretation is the same: the U.S. labor market has been crushed by the pandemic and subsequent policy responses.

Payroll employment is a key coincident indicator for the economy. As such, the second of what is likely to be a number of months of sharp declines in payroll employment suggests that the U.S. economy may have peaked in February and entered a recession in March. Overall, private payrolls lost 19.5 million jobs in April with private services losing 17.2 million and goods-producing industries losing 2.4 million. For private service-producing industries, the declines were led by a 7.7 million decrease in leisure and hospitality. Three other industries lost more than 2 million jobs each: professional and business services declined by 2.128 million with temporary help accounting for 842,000 of that total, retail lost 2.107 million workers, and health care and social-assistance industries fell by 2.087 million. Within the 2.4 million loss in good-producing industries, construction was down 975,000 jobs, durable-goods manufacturing lost 914,000, nondurable-goods manufacturing fell by 416,000, and mining and logging industries lost 50,000 jobs (see first chart).

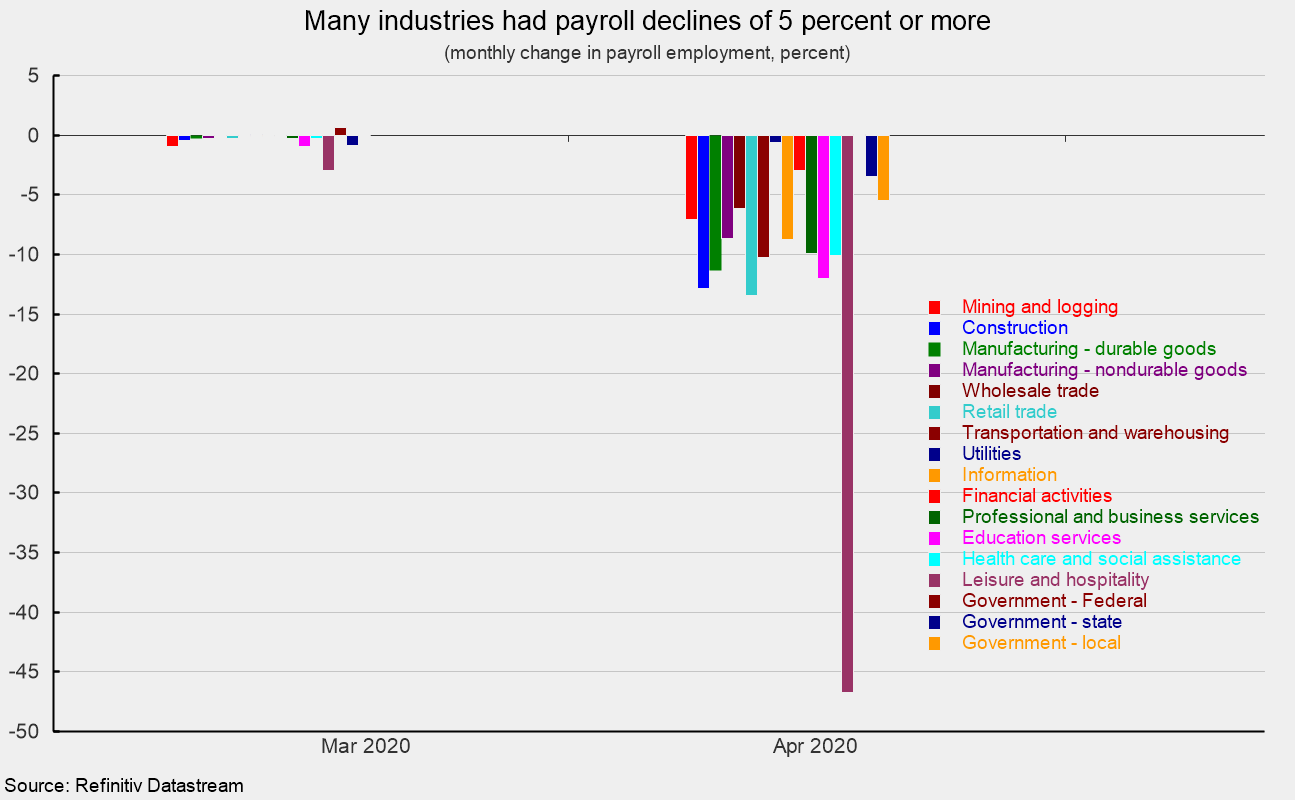

While the magnitudes of the declines are staggering, the breadth is also shocking. Measured on a percentage basis, all of the 14 private-sector industry categories posted declines in April, with 12 of them showing a decline of at least 5 percent. By far, the worst decline was a 46.8 percent drop in leisure and hospitality. (see second chart).

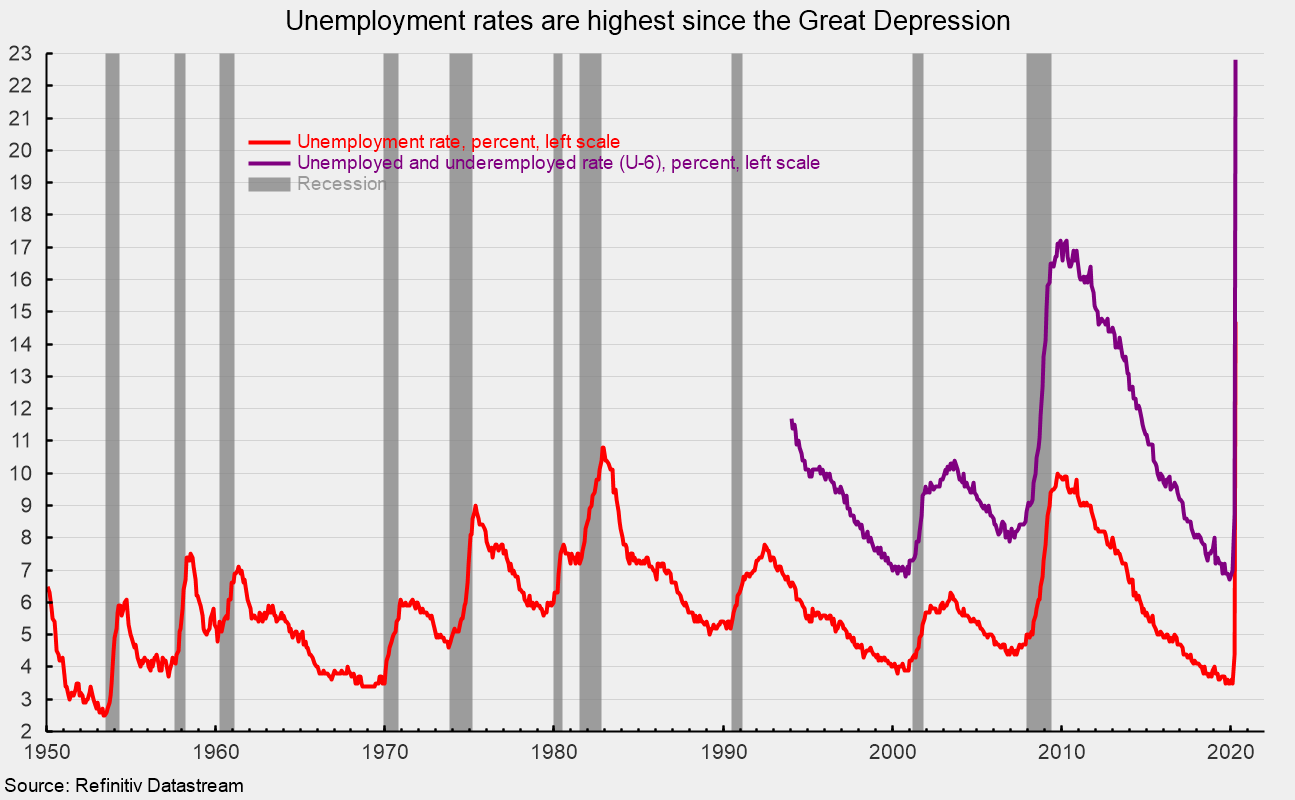

The unemployment rate surged to 14.7 percent while the participation rate sank to 60.2 percent. That officially reported 14.7 percent rate was the highest in modern records back to 1950, with the previous peak being 10.7 percent in November 1982 (see third chart). Though data collection was much less reliable, the unemployment rate following the Great Depression was estimated to have peaked at 25 percent in 1933. The Bureau of Labor Statistics also noted that the technical issues with this report likely underestimated the unemployment rate by about 5 percentage points, meaning the actual rate was nearly 20 percent. The officially reported underemployed and unemployed rate, referred to as the U-6 rate, hit 22.8 percent in April (see third chart).

Average hourly earnings soared but these numbers are distorted due to the skewing of job losses towards lower paid workers. Average hourly earnings rose 4.7 percent for the month putting the yearly gain at 7.9 percent. Combining payrolls with hourly earnings and hours worked, the index of aggregate weekly payrolls fell 10.9 percent in April and is off 8.3 percent from a year ago.

The disastrous jobs report for April combined with the record-shattering initial claims for the final two weeks of April make the probability of a recession a near certainty. Now the focus turns to monitoring the depth and duration of the recession. Much of that will depend on the progression of the COVID-19 outbreak, the ability of the medical and scientific community to find a cure and prevention, and the policies of the government to deal with the outbreak and mitigate the damage to the economy.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.